Demographic shifts

Supporting the intergenerational wealth transfer

In recent years, there has (quite rightly) been a big focus on the growing pool of older individuals with large DC pots that they must rely on in the absence of a DB pension.

Supporting this demographic will be vital, but we cannot lose sight of who’ll be receiving this accumulated wealth. The challenge here is that younger clients remain something of a mystery to lots of wealth managers, and it’s estimated that around 90% of heirs change their adviser.

Who is transferring wealth?

Who is inheriting wealth?

Silent Generation (born 1928-1945)

Generation X (1965-1980)

Baby Boomers (born 1946-1964)

Millennials (1981-1996)

Generation Z (1997-2012)

To tackle this, we first need to be clear on the ‘known unknowns’. For example:

We know that £5.5tn is set to be passed down by 2050 – the largest generational wealth transfer in history. [source]

We know that the beneficiaries will include millennials, Gen Z and a significant proportion of women. [source]

There is a clear advice gap among this cohort, stemming from both a lack of consumer confidence and the challenge of squaring the commercial circle when these younger individuals don’t, currently, have sufficient assets to take on the risk of advising them.

Our experience is that most wealth professionals know the intergenerational wealth transfer is coming and, in many cases, what needs to be done. However, the pressures of current client needs and near-term EBITDA result in the inevitable “not yet” on building the proposition.

Our hope is that the regulator’s targeted support consultation will provide advice and guidance which will bring us a step closer to closing the gap mentioned above. But running alongside the advice and education problem is a business-risk consideration of what happens if things go wrong.

To support this part of the debate, we’ve analysed how ‘wrong’ you can be if the foundations of a well governed, simple and low-cost investment proposition are in place.

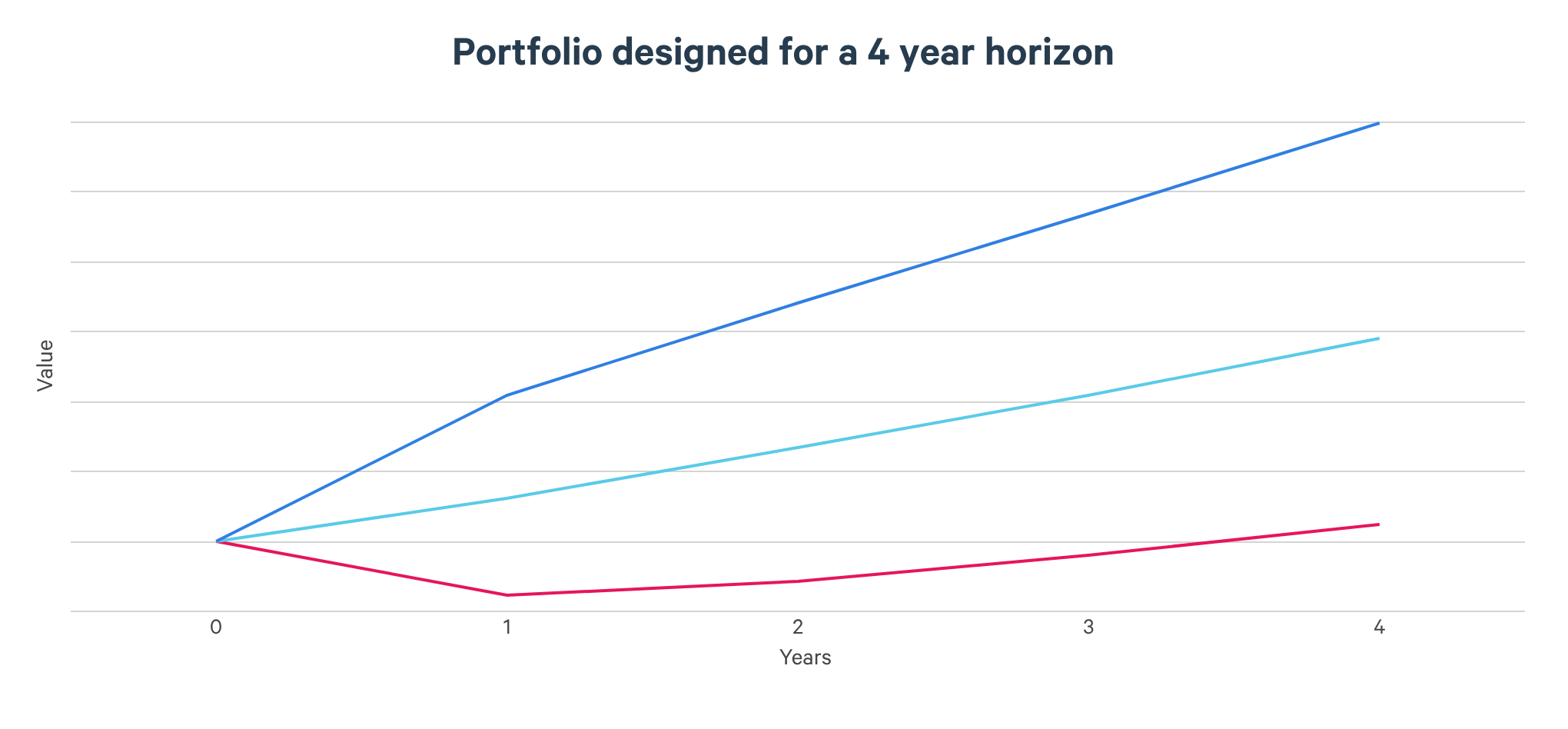

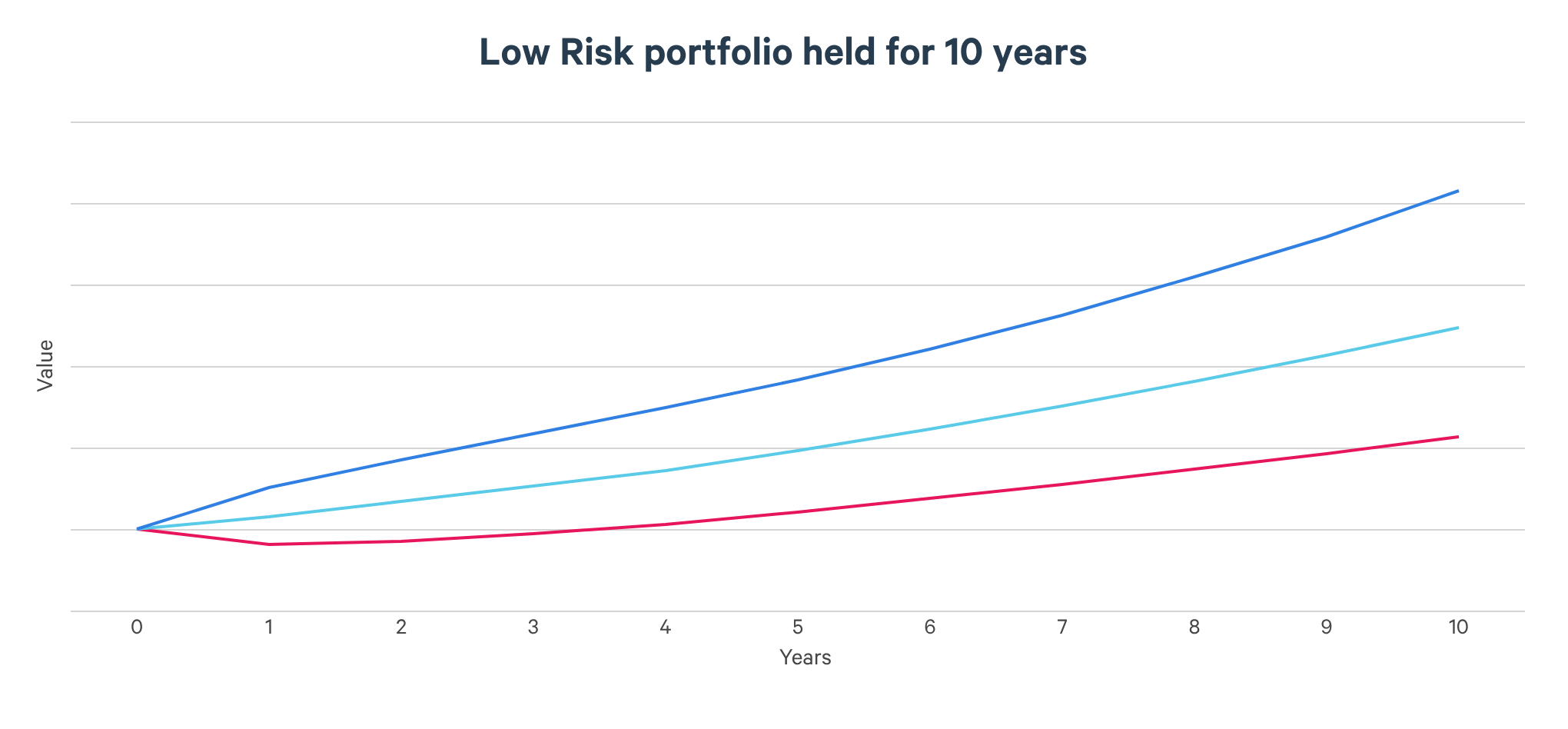

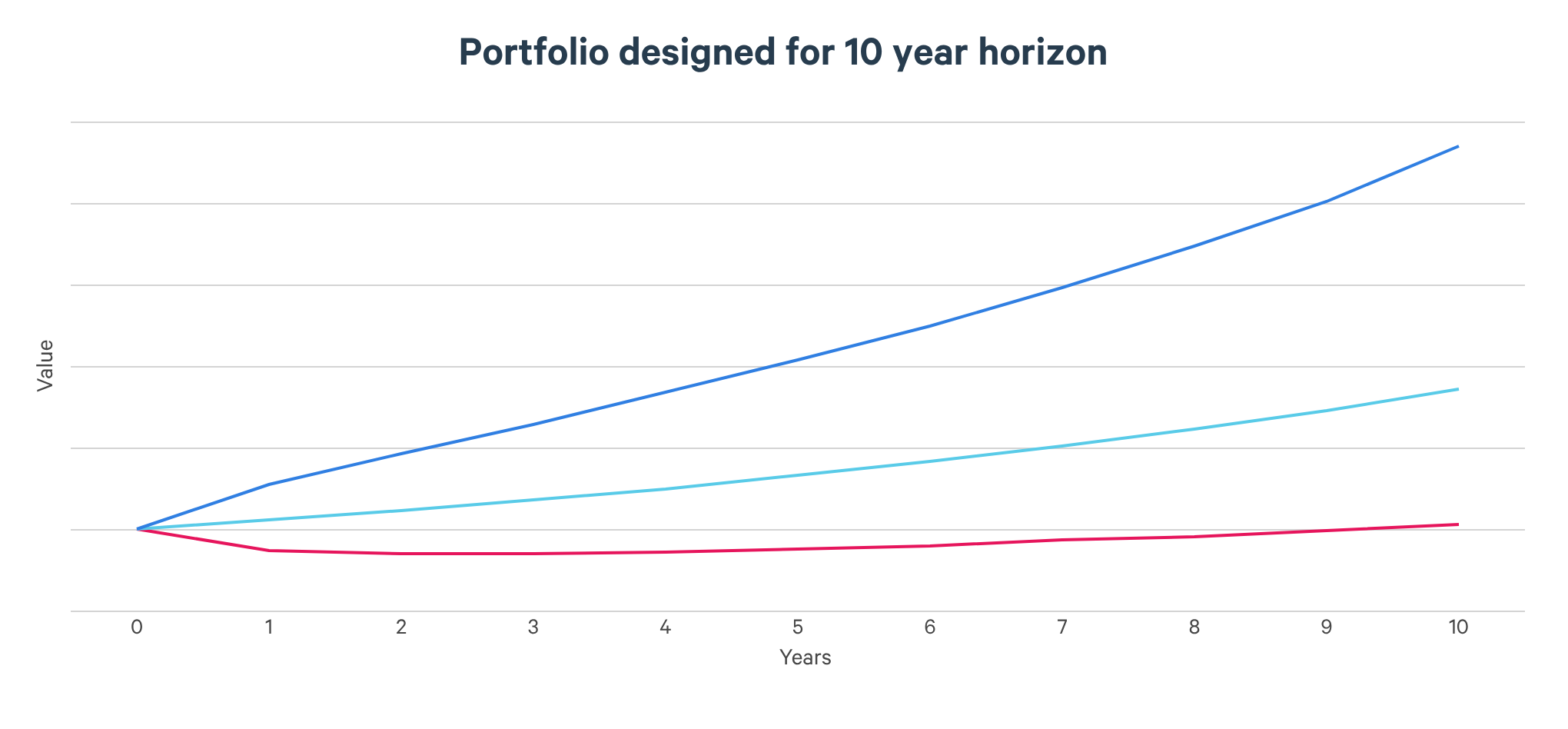

So, how wrong can you be? Take this simple core portfolio range.

CLIENT 1This client presents as high capacity for risk with a 10+ year horizon. Then they decide they want to sell their assets after four years with no notice. The issue here is that after four years, in a bad market environment (red line), the portfolio could have lost more than it would have done in a portfolio designed for a four-year horizon. The central case and upside, on the other hand, would have delivered a better outcome though.

CLIENT 2This client presents as low capacity for risk with a four-year horizon. Then they leave the money with you for 10 years. The issue here is that the client has missed out on the potential for substantial upside. Albeit, in a bad scenario, they would still be better off in the lower risk portfolio.

The importance of developing a well governed investment proposition cannot be understated. Delivering appropriate advice to clients to match their investment time horizon is of the utmost importance to ensure good client outcomes.

Almost quarter of Gen Z go to advisers for investment advice - FTAdviser