Changes and challenges

Emma MartinSenior CounselSackers

Find me on LinkedIn

Drop me an email

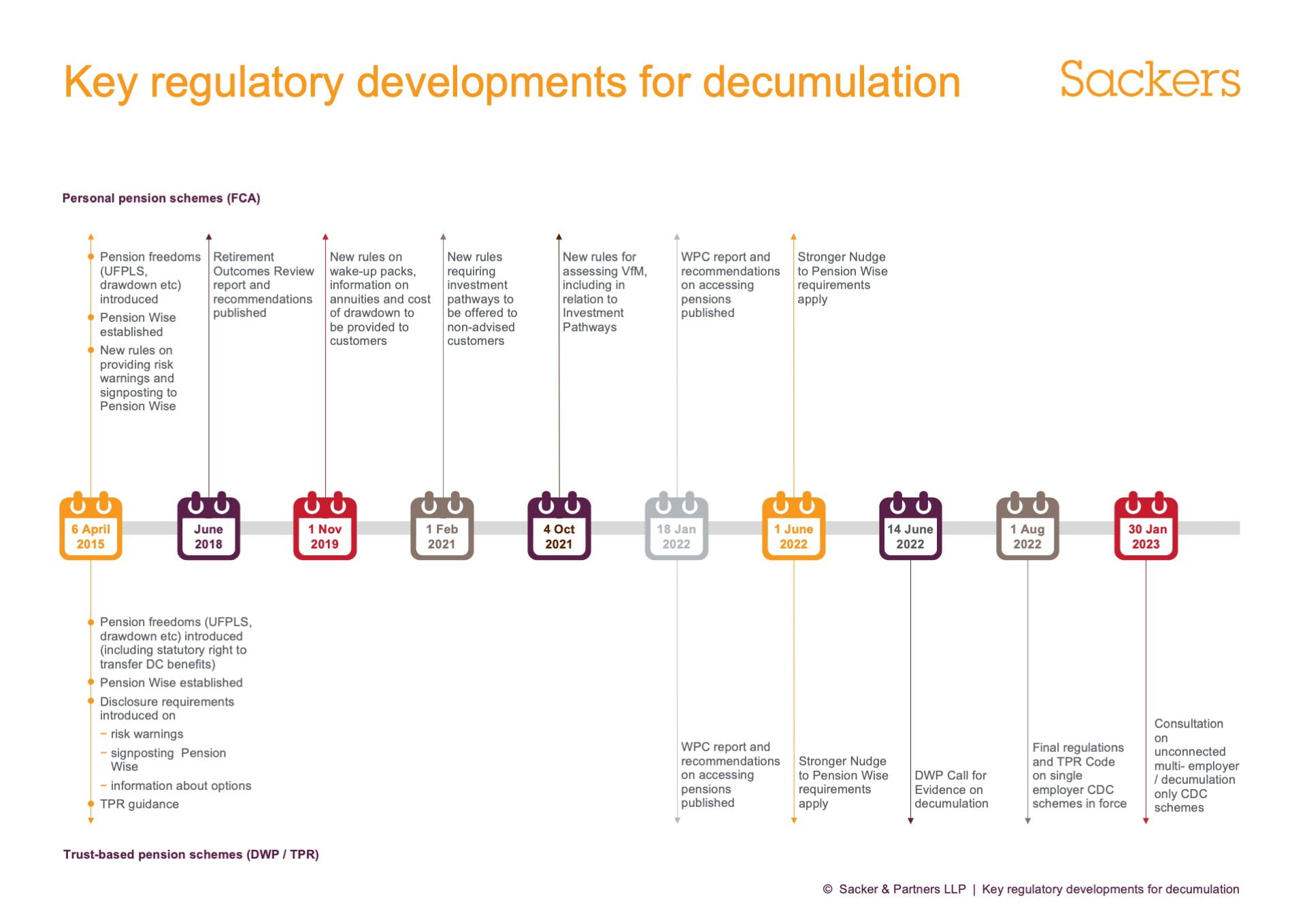

The introduction of pension freedoms on 6 April 2015 launched a new regulatory regime for DC retirement across trust schemes and personal pension schemes. Although the basic freedoms are the same, there are currently different rules about how trustees (for trust schemes) and FCA-regulated providers (for personal pension schemes) should manage the retirement or “decumulation” process, as illustrated in the timeline on the next page.

Divergence in regulatory approach Until now, the Department of Work and Pensions (DWP) and The Pensions Regulator (TPR) have focused on how members join trust schemes, and the rules surrounding how members contribute to and invest in them. They haven’t had much to say about how members choose to retire and take their benefits. This is understandable given the relatively young DC population in trust schemes and the small number of trust schemes that offer drawdown or multiple cash sums.

In contrast, for personal pension schemes, the FCA has introduced various measures to support consumer decision-making at retirement. This is largely in response to the findings of its Retirement Outcomes Review published in 2018. These include new requirements for retirement “wake-up” packs and the introduction of clearer charges information. There’s also a requirement for providers to offer investment pathways for non-advised consumers accessing their pension savings, which independent governance committees must assess for their value for money.

This has created some disparity between trust schemes and personal pension schemes; for example:

There’s currently no requirement to offer investment pathways in trust schemes.

Trustees are only required to provide members with retirement wake-up packs four months before their retirement date, whereas FCA-regulated providers are required to send retirement wake-up packs earlier (from age 50) and more frequently.

Once a person has accessed their DC pension pot, pension providers are required to send annual information on the costs and charges paid, but there are no equivalent ongoing communication requirements in decumulation for trustees.

Move to a more joined-up approach?Against this backdrop, the Work & Pensions Committee published a report [1] in January 2022 calling on the Government and regulators to play a more active role in supporting savers to help them make better decisions when accessing their savings and to develop a more coordinated approach.

In response, the DWP published a call for evidence on 14 June 2022 regarding aligning the two regulatory regimes with the aim of improving member outcomes. In particular, the DWP wishes to explore if there should be new duties for trustees in decumulation, including whether to implement investment pathways. However, fundamental differences between trust schemes and personal pension schemes would need to be reflected in policy development.

For example:

Trustees have a fiduciary duty to act in the interests of members as a whole, whereas FCA-regulated providers have a direct relationship with each consumer.

Members with DC pots in trust schemes often have DB scheme benefits that sit alongside them and aren’t usually wholly reliant on their DC pension savings.

Despite these differences, recent regulatory developments show the start of a more coordinated approach between the DWP/TPR and FCA following the launch of TPR/FCA’s joint regulatory strategy in 2018.

We’ve seen a good example of this coordination in relation to the “Stronger Nudge” requirements effective from 1 June 2022. Under this initiative, trustees and pension providers have been required to deliver a Stronger Nudge to Pension Wise guidance for DC transfers and retirements. Although some operational differences between the DWP and FCA requirements exist, there’s a broad consistency in approach and the fundamental principles are the same.

What does the future hold?One of the key recommendations from the WPC report related to collective defined contribution (or CDC) schemes. These schemes provide retirement incomes from a collective fund, so members don’t have to make complex financial decisions at retirement and don’t need to purchase an external annuity. The Government is currently consulting on whether CDC could help it achieve its goals for better member outcomes by extending CDC in the trust-based space to unconnected multi-employer schemes (including master trusts) and decumulation-only arrangements. There are a number of challenges to overcome, but this could be an exciting development for the industry.

There are also voices calling for more wide-ranging regulatory change. For example, the Pensions and Lifetime Savings Association (PLSA) has proposed the establishment of a new regulatory framework, including a legal obligation for schemes to signpost members to a preferred product or solution at retirement. The framework would also deliver a set of minimum standards for the member journey as well as retirement product design and governance.

Wide-ranging changes to regulation on decumulation are needed to clarify and coordinate the obligations on trustees and pension providers. As pension lawyers, we’re very much looking forward to seeing how this area develops in the future.