An asset manager's perspective

Philip MayDirector of Retirement IncomeCapital Group

Find me on LinkedIn

Drop me an email

Pensions Freedoms were introduced in 2015 to give UK retirees a wider choice in post-retirement investing and better outcomes. Unfortunately, this revolution still has some way to go in achieving this.

Saving versus spending challengesAlthough retirees no longer need to purchase an annuity, there’s little consensus about what post-retirement investment should look like. That’s perhaps not surprising, as the ‘spending’ phase of retirement planning is very different from the well-established ‘saving’ phase.

The saving years are primarily about maximising the pot size at retirement, with little consideration of volatility – as monthly contributions buy more when markets are depressed (via pound-cost averaging).

The spending years, however, present different challenges, principally dealing with uncertainty. Key considerations include:

How long a pension needs to last;

What might happen with inflation over time; and

How to deal with market volatility when drawing money down.

Moreover, while the investment objectives of retirement savers are typically similar, those of retirement spenders are more diverse, reflecting their different wealth levels and sources of income.

Innovation in asset managementThe increasing importance of investing in retirement, as opposed to for retirement, is demanding innovative thinking from the asset management industry. In the US, where DC has been the mainstay of retirement investment over many years, members typically use a Target Date Fund (TDF) structure, which is less well-known in the UK.

In a TDF, investors select a fund, usually the one nearest their anticipated retirement date (a 2040 Fund, for example). Over time, that fund's mix of stocks and bonds will gradually shift towards more conservative investments, known as a ‘glide path’. A TDF continues post-retirement, enabling the retiree to use a single fund for decades, with a strong focus on maintaining appropriate investments as they get older.

Within TDFs, there’s growing attention on the ‘in-retirement’ investment strategy, which is vital given increasing life expectancies. Retirees living into their mid-80s and beyond likely require a broad mix of assets, including equities, to keep pace with inflation. Investments that are low risk in nominal terms are unlikely to be adequate.

But remaining invested in relatively volatile assets during the drawdown phase can lead to the faster degradation of pension pots and ultimately running out of money if withdrawing during market downturns. One possible solution is to use equity strategies with some natural downside protection, typically in the form of dividend yield.

But what about non-TDF retirees, are any new ideas emerging?While advisers typically have a range of diversified multi-asset portfolios available across a selection of risk profiles, these don’t often include a post-retirement range, which could be beneficial. As investors move through retirement, they would benefit from the risk profile of their portfolio altering age-appropriately – this is particularly important for those retiring early.

Consider, theoretically, a man in the UK taking early retirement at 57, having started work at age 22. He has a life expectancy of 84 [1], which would mean a retirement of 27 years. He also has a one in four chance of living to 92, meaning his period in retirement (35 years) would be as long as his working life. This would demand a more nuanced approach to investing in retirement, with different phases requiring different types and combinations of assets, just as in the saving phase.

Blockers and solutionsWhat’s standing in the way of this happening? It isn’t clear that the right balance between product design and simplicity has been reached. Products need to do the job, but if they’re too complex, advisers, who need to explain them to clients, won’t buy into them.

The asset management community has to play its part by building straightforward, robust solutions that are flexible enough to capture individual needs but also provide good value for money.

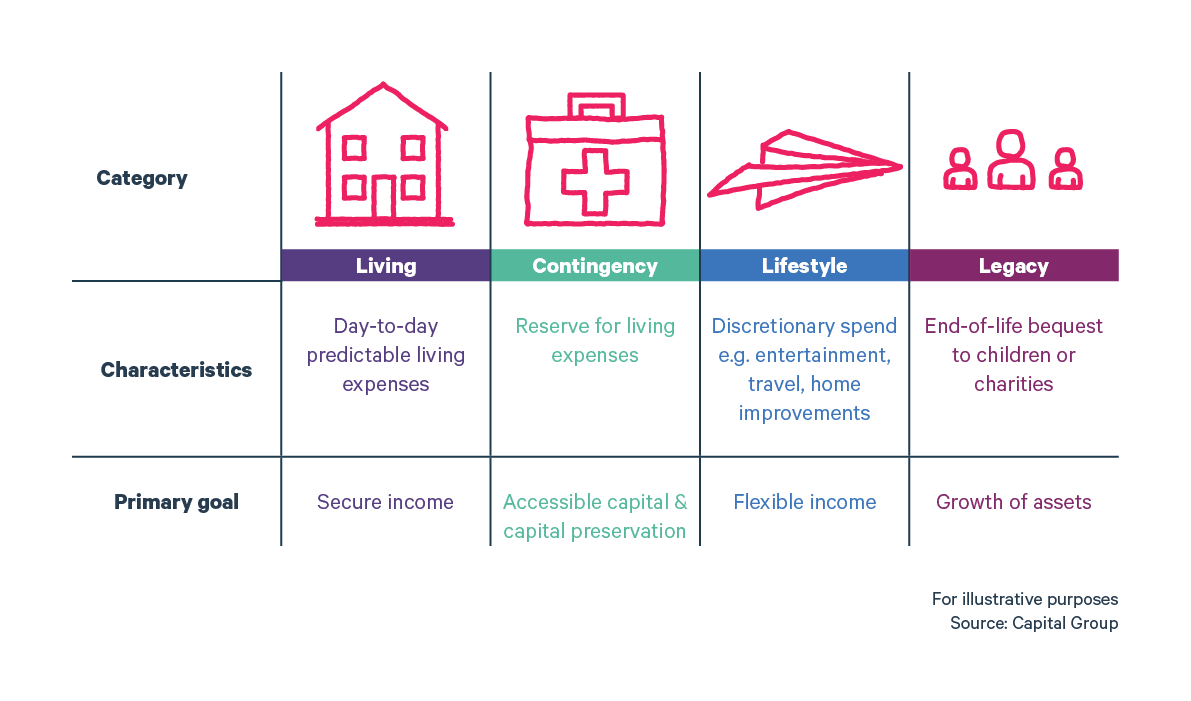

One approach is to show how retirement needs are supported by specific financial assets. The diagram on the right shows a framework for thinking about needs in retirement; it includes:

Essential living expenses, traditionally food, housing and energy costs, but this category is increasingly likely to include perceived essentials such as holidays, too;

Contingency reserves, representing ‘rainy day’ money, although this shouldn’t be excessive to reduce drag on returns;

Lifestyle expenses, consisting of entertainment, longer holidays and projects (such as home improvements); and

Legacy assets, which are typically seen as an important element in the US, but less so in the UK and, in any event, usually consist of property.

The retiree could support each of these needs with a dedicated portfolio. For example, the portfolio for living expenses could well be a lower-risk bond/cash mix, but it might also incorporate an element of annuity. Whereas the portfolio for lifestyle expenses would probably need to be one with a higher proportion of equities, with the potential to grow income over the course of retirement.

As retirement progresses, needs will change, perhaps with less required for holidays and more for essentials in the home. To adjust for this, the amounts allocated to each category could be altered or the risk profile varied. We envisage asset managers and advisers developing tools to increase the degree of personal customisation available.

Looking forward, we’d like to see more emphasis on the changing needs of the spending phase of retirement investing. It’s vital we recognise the importance of growing income over this period, and retirees should be supported through greater customisation and flexibility. There will also be a real need for straightforward communications to clearly demonstrate the benefits and arm members with the information needed to understand post-retirement investing. With many now living for several decades in retirement, this is an innovation challenge the UK asset management industry needs to embrace.