The Future of Retirement Income

Welcome to our new interactive content platform, Turtl. It's designed to give you the best possible online reading experience, and it’s configured to map perfectly to your device, whether that's a desktop, laptop or mobile.

Enjoy the read!

VIDEOSGrab some popcorn and enjoy the show!

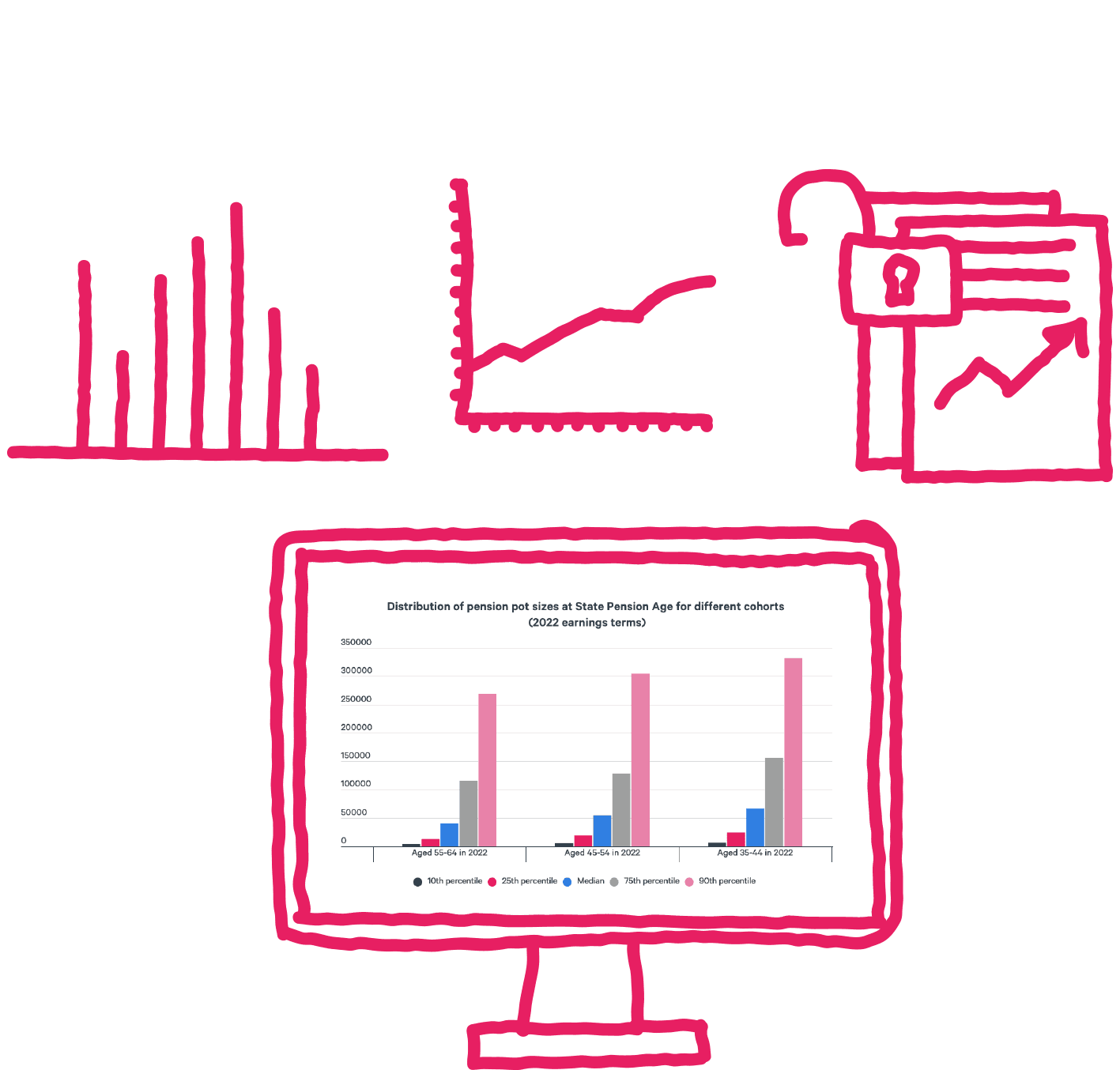

CHARTSOur charts are interactive: click on them to zoom in and explore.

POLLSWe're keen to hear your thoughts: choose, click, send – it's that simple!

PREFER A PDF? You can download our publication here or you can find a download option in the contents menu (top left).

Jonathan ParkerHead of Defined Contribution& Financial Wellbeing

Find me on LinkedIn

Drop me an email

David Lloyd George, then Chancellor of the Exchequer, introduced the Old Age Pensions Bill in May 1908 to widespread support in the chamber of the House of Commons. The Bill received Royal Assent on 1 August the same year and heralded the first broad-based, state-funded pension system in the UK, paid for out of central taxation (National Insurance was not introduced until 1925). The pension was five shillings a week (around £25 in today’s money) and eligibility was tightly controlled to those aged 70 and over. It also disqualified individuals who failed certain behavioural conditions, including those who had made themselves poor in order to qualify, had been imprisoned or convicted under the Inebriates Act.

The Times reported on 31 December 1908, the day before the first payments were expected to be made, that well over 600,000 people were expected to be eligible. The cost was estimated to be £7.5million, about £750million in today’s terms. State pension costs in 2021 were over £100bn annually……gulp!

Although private sector pensions were actually established, albeit on a limited basis, by certain employers or sectors earlier than the state pension – including Reuters (1882), WH Smith (1894) and Colman’s (1899) – coverage of any form of retirement income was extremely limited until well after the Second World War.

Importantly, the primary objective stated for these early pensions was to act as a replacement for income that had been lost by giving up work. This focus on income is critical, which is why the reformed basic state pension in the UK today remains the core foundation of any retirement provision.

Fast forward to 2023 and the world is a very different place. The concept of longevity escape-velocity (LEV) [1] is gaining traction, and apparently we are only a few years away from advances in science being able to extend our life expectancy for more than a year for every year we are alive. If these predictions by certain futurists are proved correct, how does a pot of lifetime savings last if you’re potentially going to live forever?

Over the last 20 years or so, defined contribution (DC) pensions have become the main way most people in the UK (and elsewhere around the world) save for later life. Although it may not yet be the main source of income in retirement, what is very clear is that there has been a steady shift in responsibility for saving, and bearing the risk for income in retirement, from the state and employers, to the individual.

The real-world implications of the ‘pension freedoms’ reforms are now starting to be felt. There's a real need for the pensions industry to work together to support DC members in making a number of very complicated decisions and collaborating on the best ways to provide sustainable income in later life. This comes at a time when the traditional concept of retirement as envisaged through the Old Age Pension Act is itself changing.

In this first for the pensions industry, Redington has brought together leading voices in a collaborative publication aimed at kick-starting the debate on the future of retirement income.

I would like to thank our external experts who contributed articles:

Philip May (Capital Group)Sarah Hawke (Quietroom)Mark Ormston (Retirement Line)Emma Martin (Sackers)Tom McPhail (The Lang Cat)Vaughan Jenkins (Moneyhub)

And a long list of colleagues at Redington (including Anran Chen, Arash Nasri, Sanam Mehta, Iona Young and Nkolika Ezepue) who have written articles and made this initiative possible. In particular, Russ Wright who has led the project from start to finish.

We’d love it if you joined the conversation through engagement with this publication, joining our roundtables or talking to the team.

Contact us dcteam@redington.co.uk

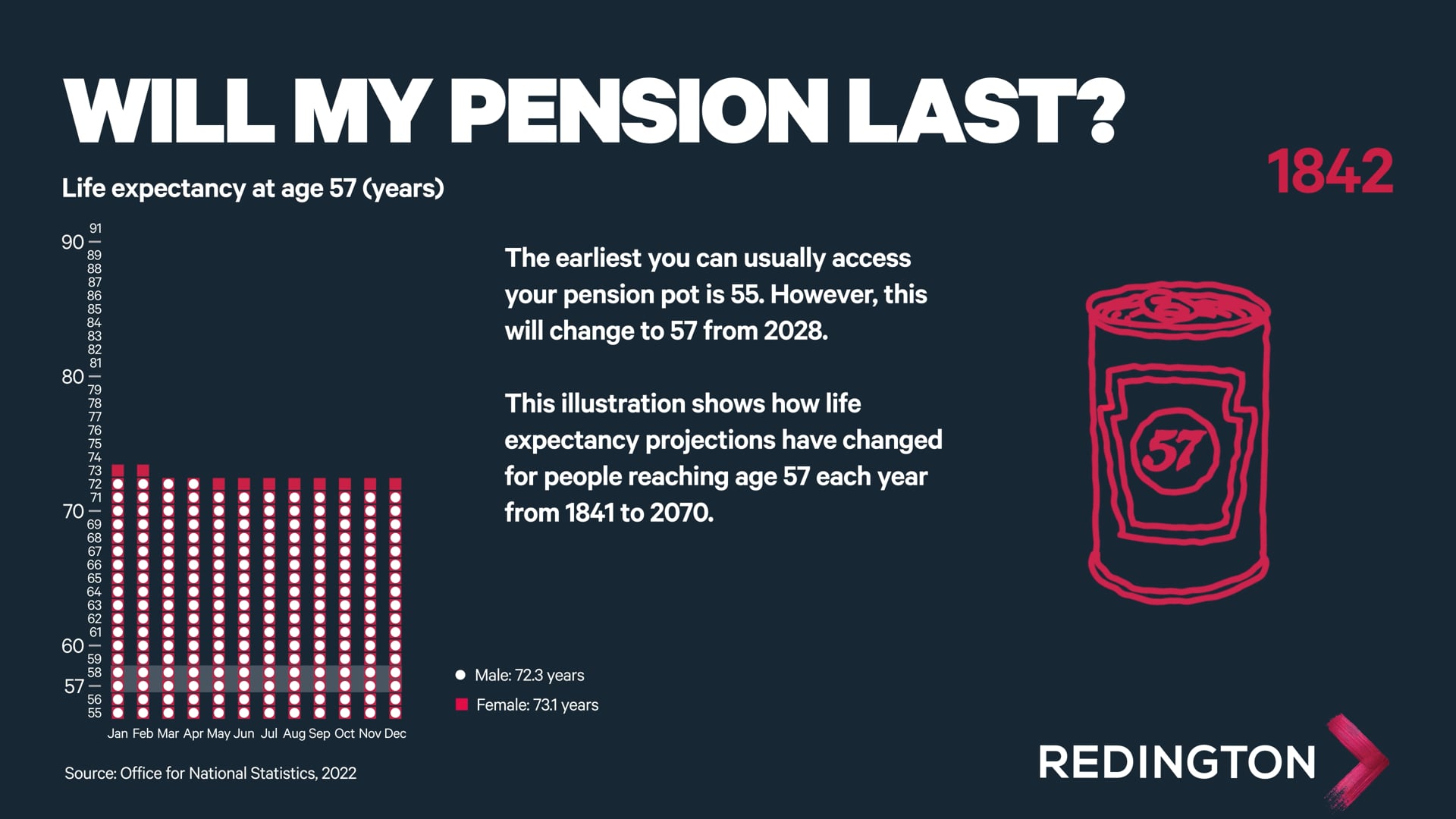

With the normal minimum pension age increasing from 55 to 57 in 2028, our focus is on age 57 and beyond. In particular, how can people in the UK avoid the proverbial “beans-on-toast retirement” that could occur without innovation. We tackle this important subject from a number of angles including member support, product development, income sustainability & technological innovation.

This publication will be complemented by a series of roundtable discussions dedicated to these areas - we’d be delighted if you would like to participate.

July 2023 edit: We’re delighted to share that The Future of Retirement Income has been awarded Content Campaign of the Year, by Investment Week’s Investment Marketing & Innovation Awards 2023.