Enhancing your pension’s pot(ential)

Alex WhiteManaging Director and Co-head of ALM

Find me on LinkedIn

Within the world of pensions, much investment focus to date has been placed on DC savers – encouraging members to increase their contributions and accumulate wealth. These efforts have been important and successful, with the PPI projecting the median total DC pension assets in the UK to grow from around £545 billion today to over £1 trillion by 2042.1

However, with a growing number of DC members entering the decumulation phase – many of whom are at risk of running out of money prematurely – we need to devote attention to pension spenders too.

Enhancing your pension's pot(ential)

So, what options exist to help members with decumulation?Since the pension freedoms were announced in 2014, DC members have tended to shun the security of annuities in favour of the flexibility of drawdown. This brings with it a range of risks that most people will struggle to manage. And of course, those needing their pension to provide them with a lifetime income will want to ensure they’re managing their investments and income effectively to maximise their chances of success.

As with most investment conundrums, there’s no one-size-fits-all solution. That said, investors typically have only two options to choose from when it comes to decumulating wealth more effectively:

Option 1: Change how much they drawdown; or Option 2: Change their investment strategy.

Unfortunately, most people will retire with just a modest-sized pension pot and fixed income needs (research shows that most people see holidays as essential, for example). So, there’s likely to be little scope to reduce the amount withdrawn – or to fluctuate it based on investment performance. Therefore, the impact Option 1 can have on one's overall retirement outcome is likely to be marginal in many cases.

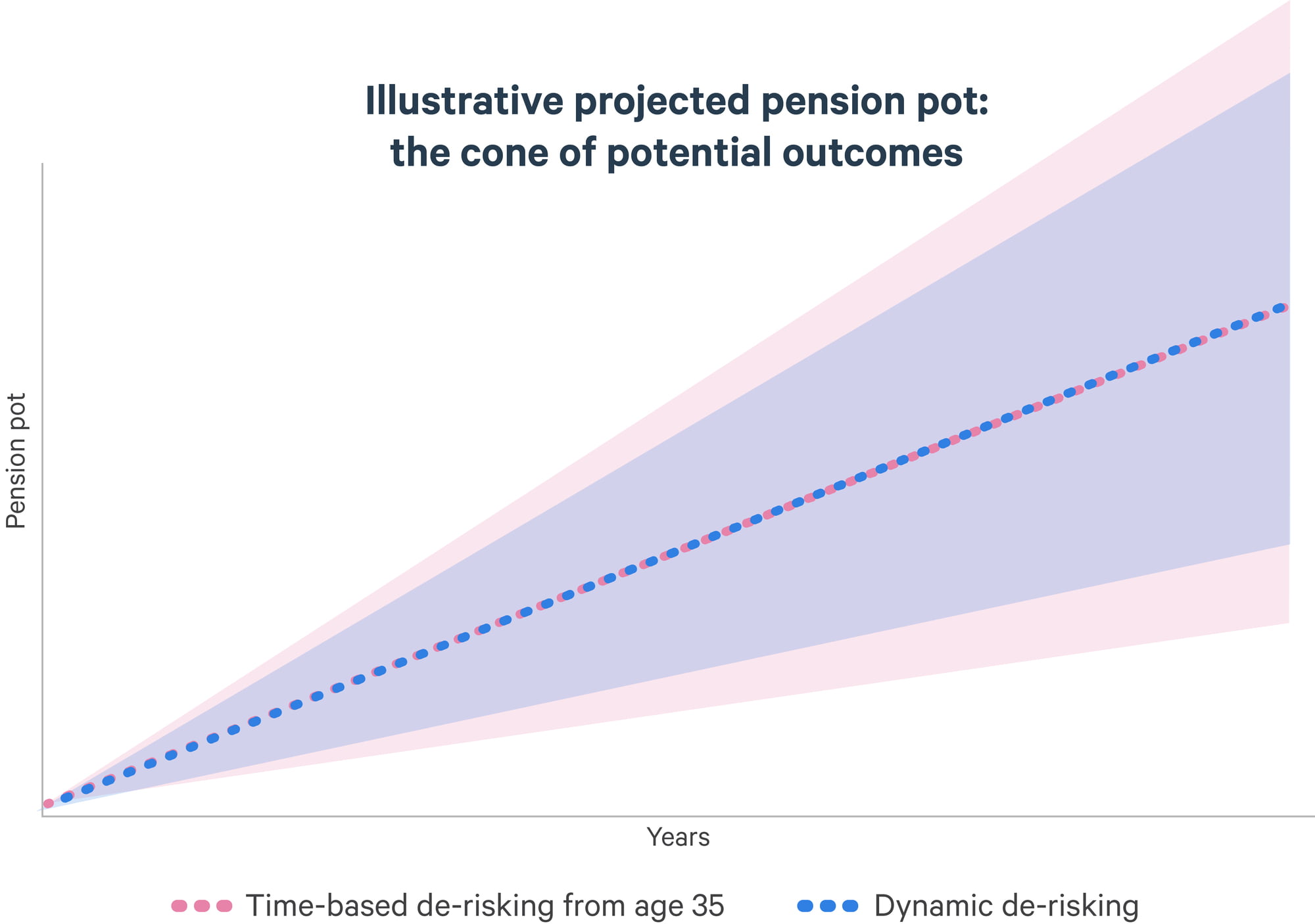

Option 2, however, could have a much more meaningful impact. Typically, DC investment strategies tend to employ time-based de-risking. For example, the portfolio will start to gradually de-risk from 100% equities when a member reaches age 35 to mostly cash and fixed income when they reach age 65 (or their selected retirement age). The aim of which is to narrow the cone of potential outcomes.

Although this strategy helps provide more certainty over the projected pension pot, it’s not necessarily the most efficient option. Introducing some form of dynamism into the investment strategy could help maximise the pot’s potential.

What could a dynamic decumulation strategy look like?Rather than adopting a time-based approach to de-risking, suppose the pot was de-risked based on investment performance. For instance, when the portfolio has performed well, it's shifted to a less-risky strategy to effectively bank some of the gains made. Then, during periods when the portfolio hasn’t performed so well, the strategy is re-risked with the aim of improving returns.

Applying this dynamism, we’d expect to trim some of the extremes – both on the upside and downside – hence further narrowing the cone of potential outcomes while improving the projected central case, as can be seen from the chart to the right.

While making minor refinements to a base strategy avoids having binary, time-based cut-offs that can negatively impact the long-term performance of pension assets, this approach is no magic bullet, and it can mean going against market momentum.

But aren’t members still at risk of running out of money?All this is assuming the member takes a steady income from the point of retiring until the end of their life. However, there are two potential issues with this line of thinking:

1. Due to lifestyle changes, it’s unlikely that pensioners will require the same level of income when they’re say, 95, as when they were 65. Drawdowns could arguably be more aggressive when the member is younger, reducing over time. But this brings with it an increased risk of running out of money if withdrawals exceed investment growth; and

2. At an individual level, longevity risk is high, so there’s a risk of depleting the pot prematurely.

One potential solution to this is CDC – where investment and longevity risk would be pooled. We shared our thoughts on this in the last edition of The Defined Contrarian.

Alternatively, members could consider a hybrid solution comprising an annuity covering the minimum required retirement income while maintaining – rather than exhausting – a pot of assets to draw additional income from. Given the stability provided by the annuity, the additional pot of money warrants greater exposure to growth assets than would otherwise be possible, allowing the pension assets more potential for growth over the long term.

Ultimately, while dynamic spending (including CDC and hybrid income options) may be more effective than dynamic risk adjustments, another lever that may need to be pulled is delaying retirement.

Pension providers must embrace some of the creativity they’ve applied to pension savers to improve the outcomes for those members in the spending phase. Moving away from binary de-risking and educating members about the benefits of hybrid income options are two potential solutions. But far more needs to be done to provide a sustainable retirement income for the masses. You can read some of our – and the wider pensions industry’s – thoughts in our award-winning publication, The Future of Retirement Income.