DIVERSITY, EQUITY & INCLUSION

A long road still to travel

of managers have DEI policies in place. While still a high proportion, this is a slight decrease year-on-year.

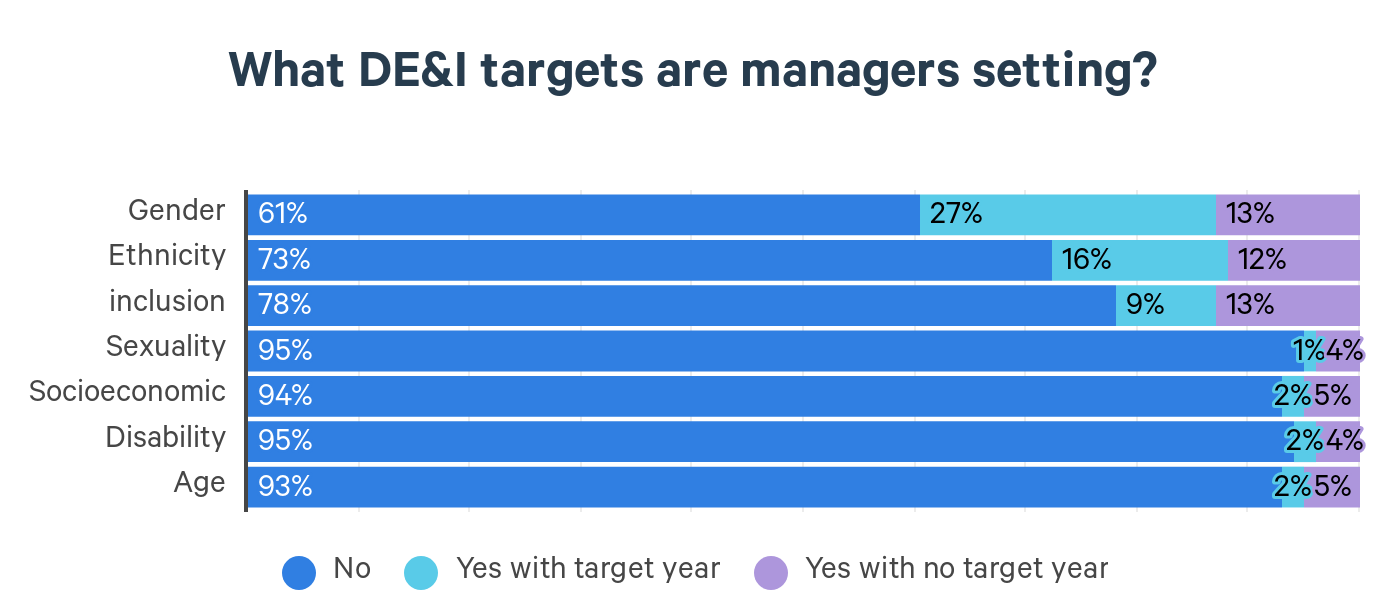

“Gender remains the most common target set by managers (40%), followed by ethnicity (28%) and inclusion (22%).”

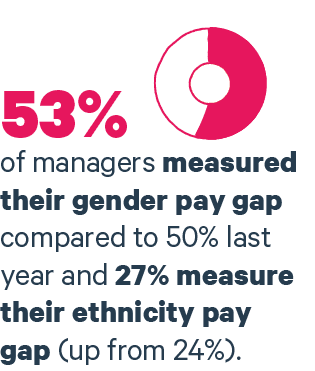

of managers measured their gender pay gap compared to 50% last year

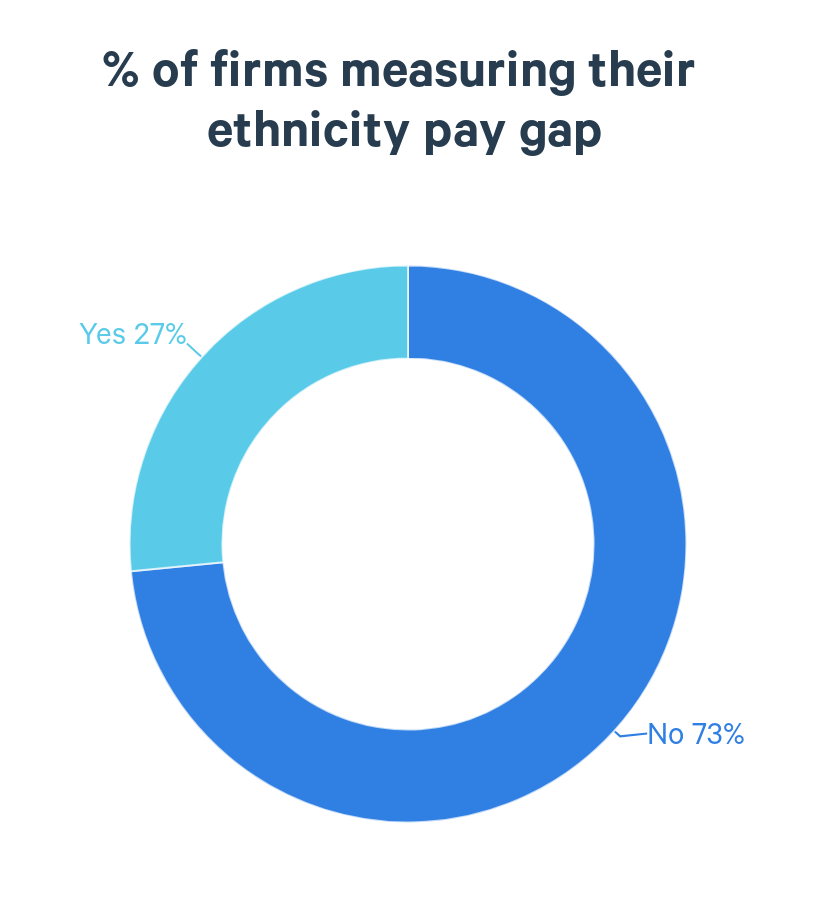

measure their ethnicity pay gap (up from 24%)

Yes

No

Not sure

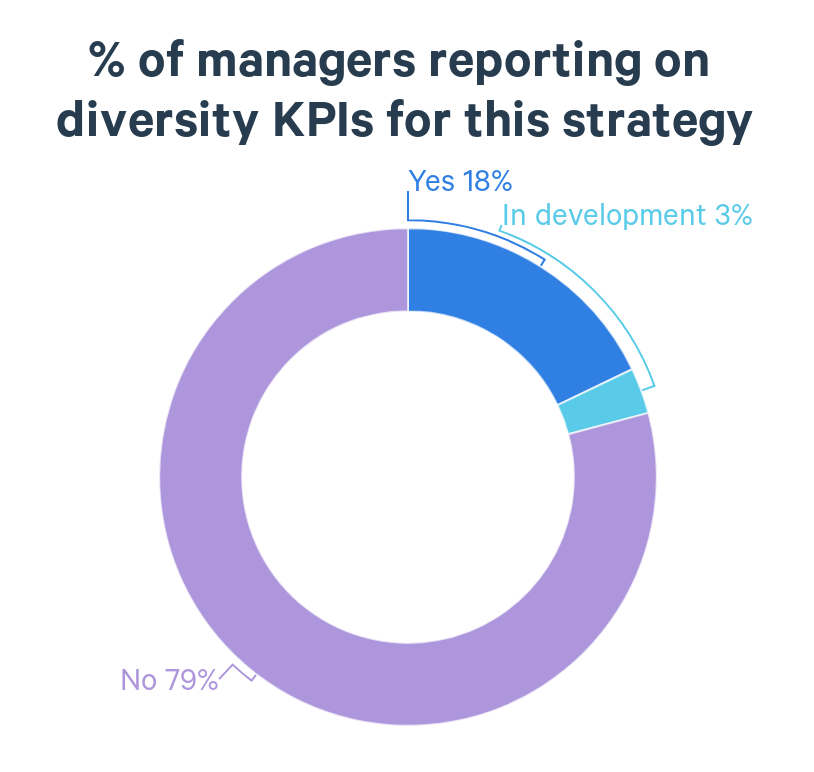

of managers don’t track and measure promotion levels and time to promotion across different groups

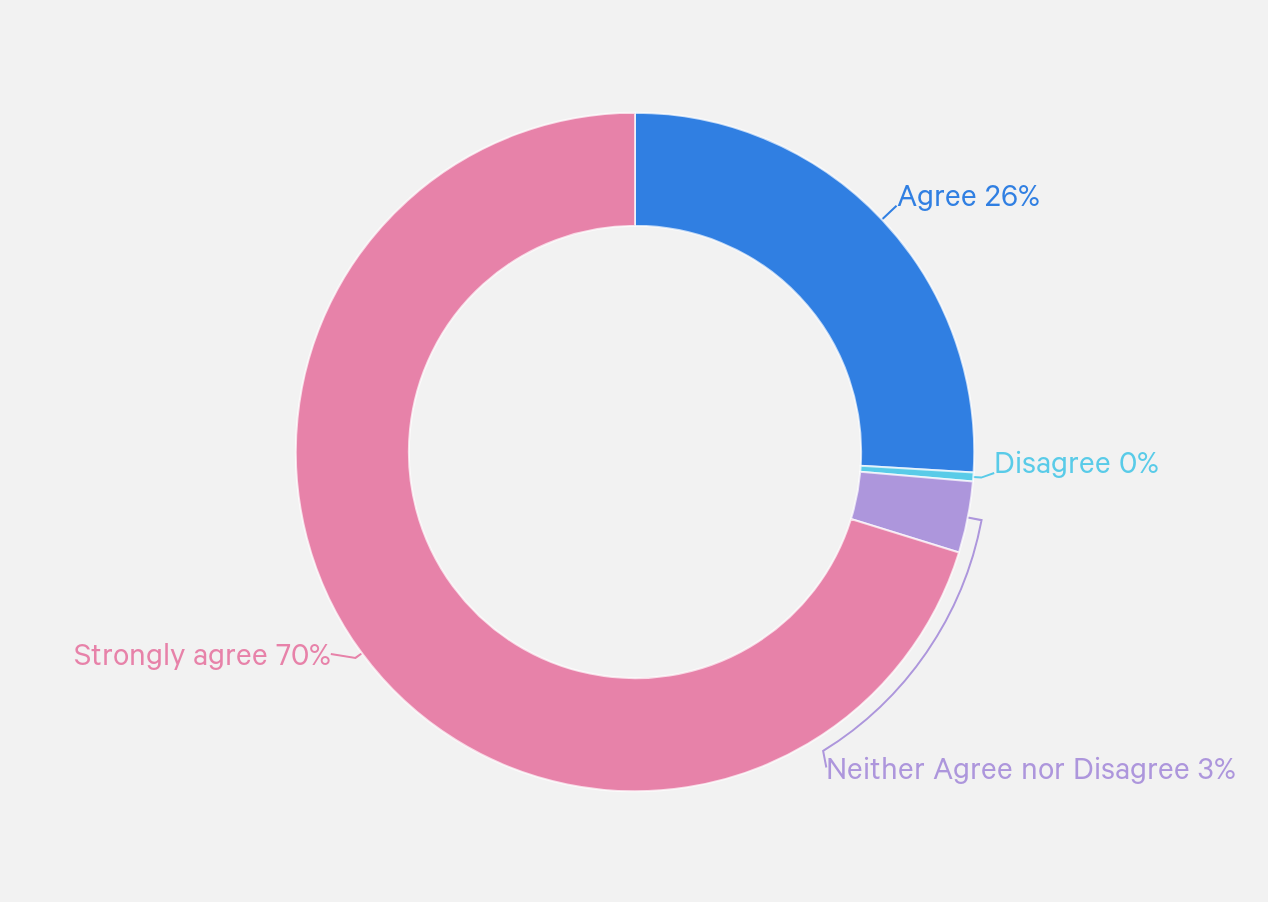

96% of managers agree or strongly agree that diverse teams create a culture of success and improve their ability to deliver a more effective investment strategy.

At face value sentiment appears to be shifting compared with last year (in 2023 80% strongly agreed and only 16% agreed), but what’s driving this?

92% managers we engaged with have DEI policies in place. While still a high proportion, this is a slight decrease year-on-year.

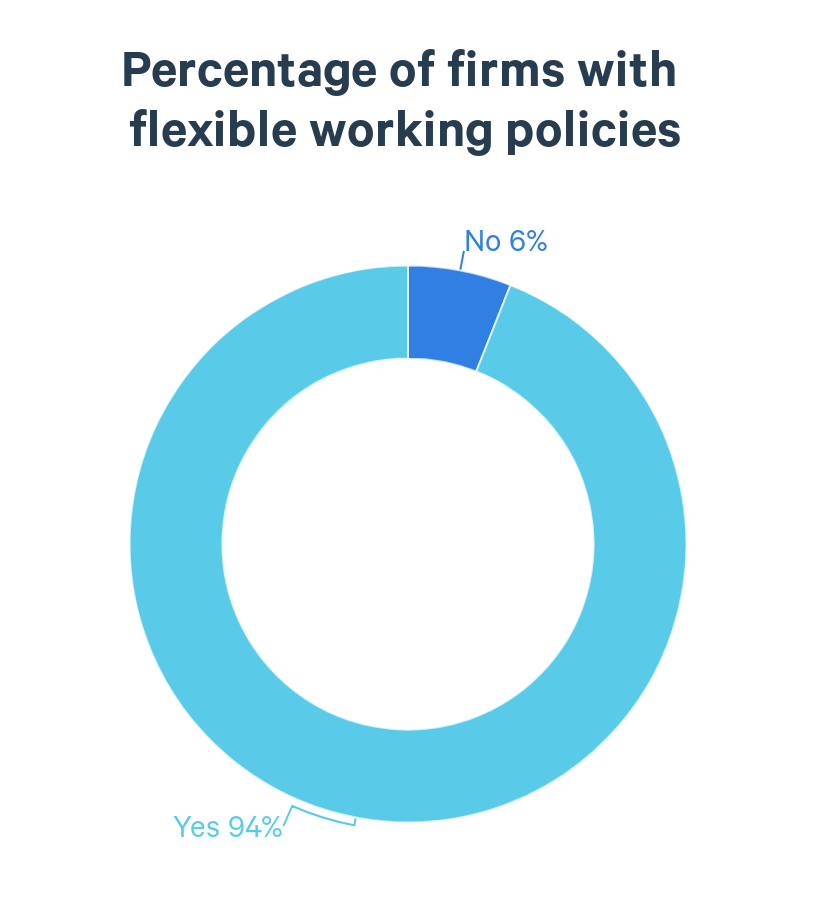

Encouragingly, 94% of firms have flexible working policies, up from 91% in the 2023 survey.

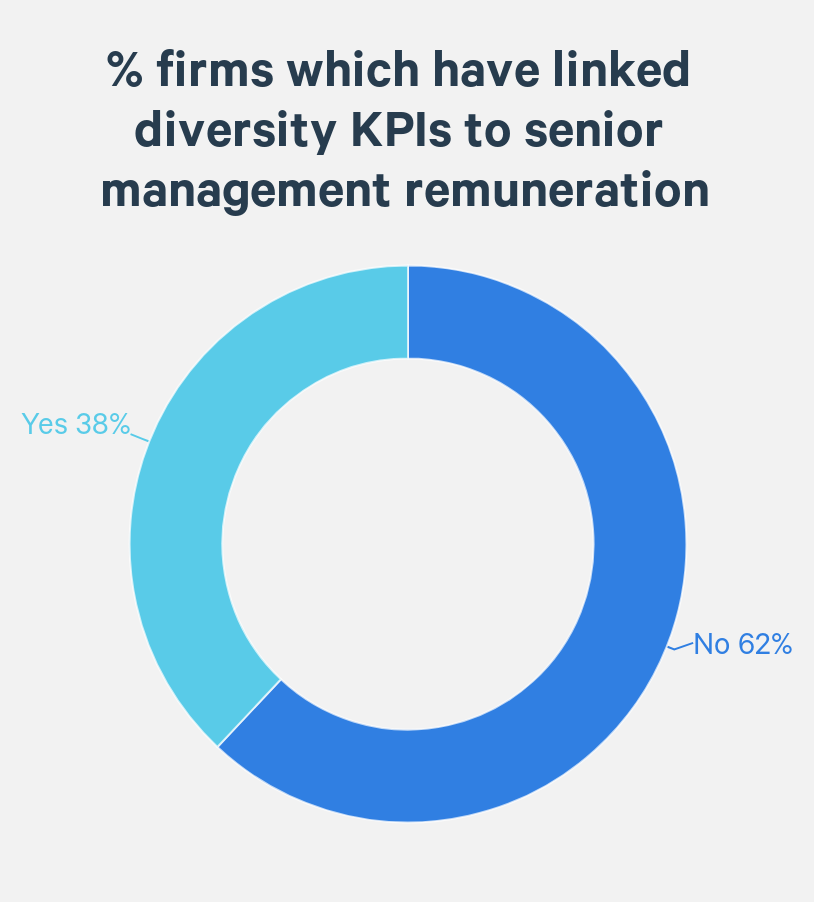

Material progress is still lacking regarding incentivisation to meet diversity targets. 38% of managers have linked their senior management remuneration to diversity KPIs, in line with 2023. Until senior leaders within firms are held accountable for making tangible progress on DEI targets, driving meaningful change will continue to be difficult.

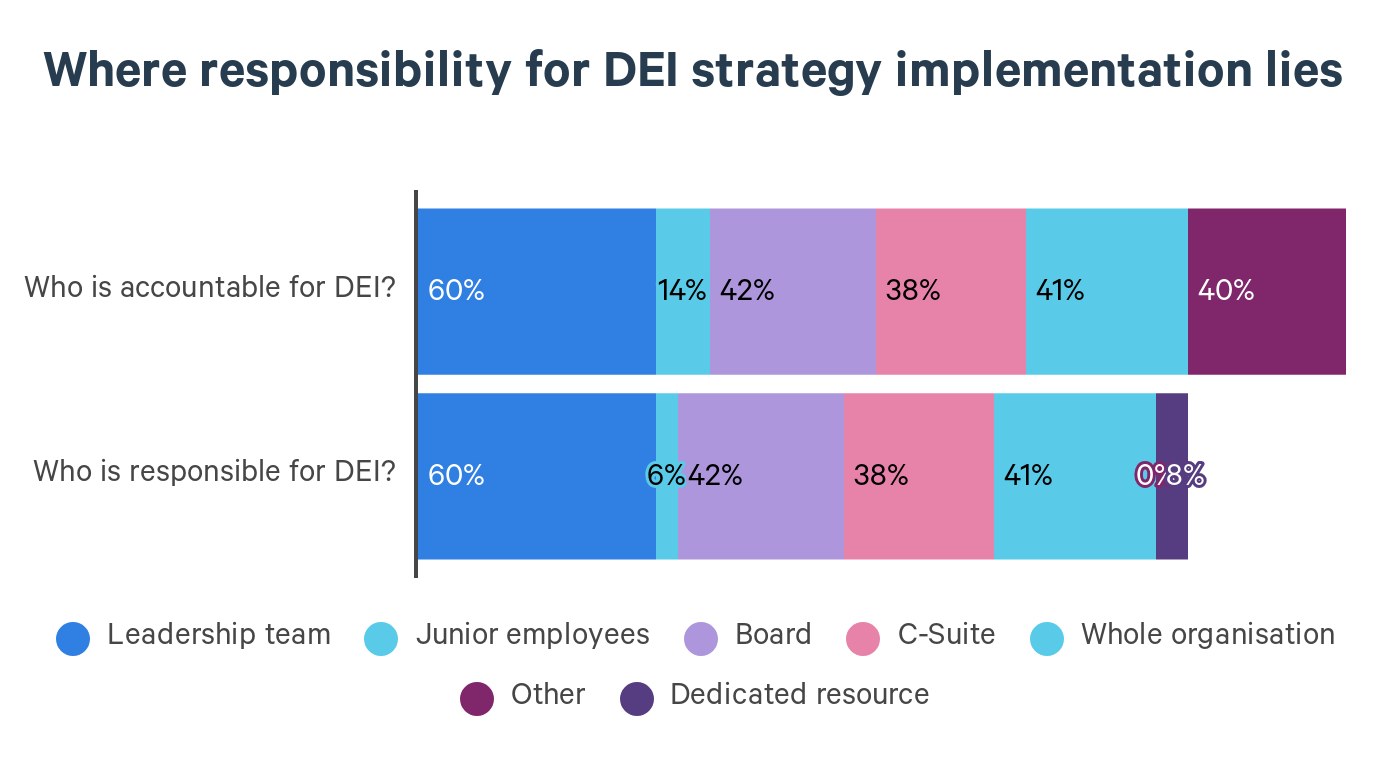

Looking at where responsibility and accountability for implementing DEI strategies lie, the data indicates that Leadership, C-Suite and the Board continue to hold responsibility for implementation, whilst junior accountability remains lower. Only 8% of firms have dedicated resource for implementation and 41% report that the entire organisation implements strategies.

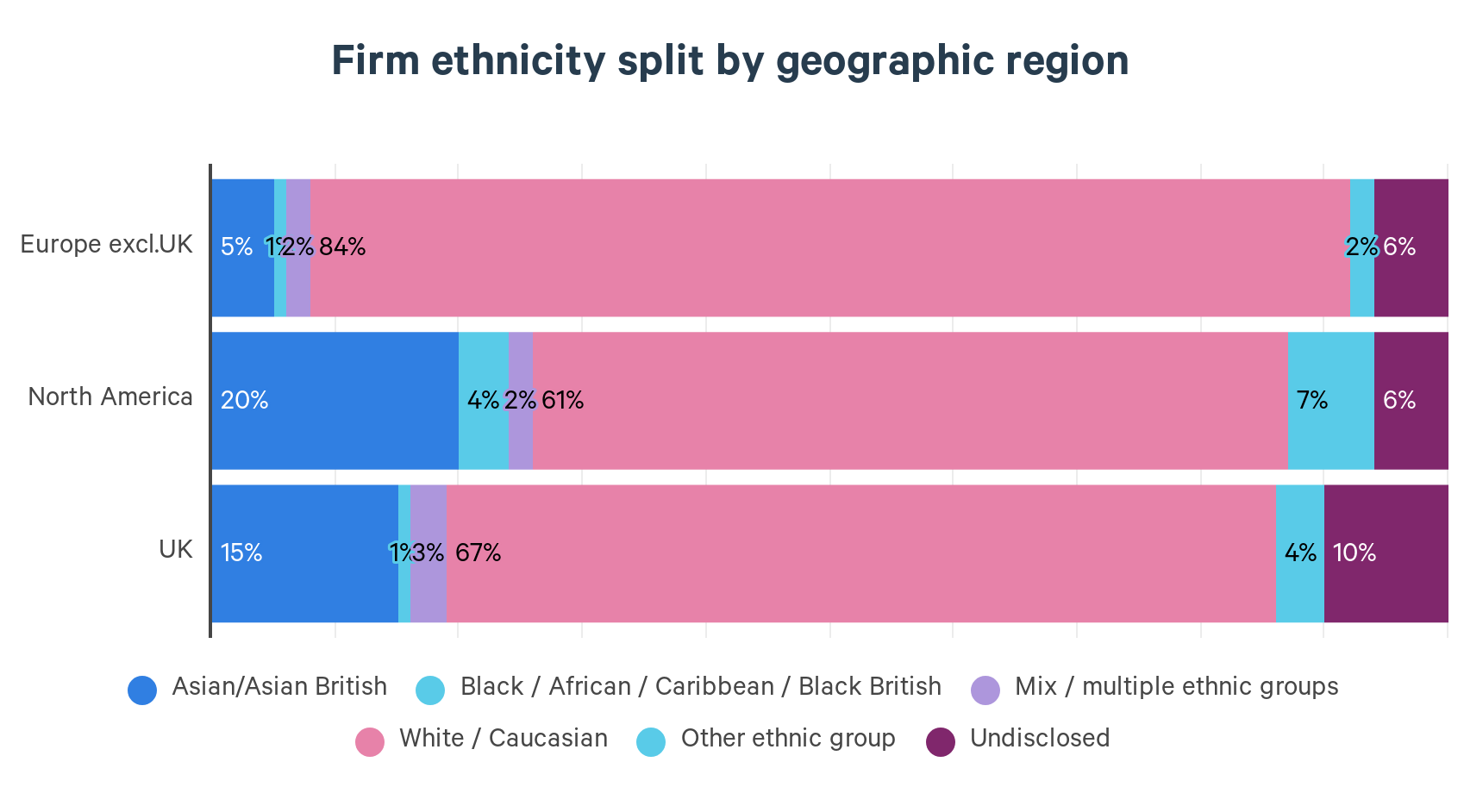

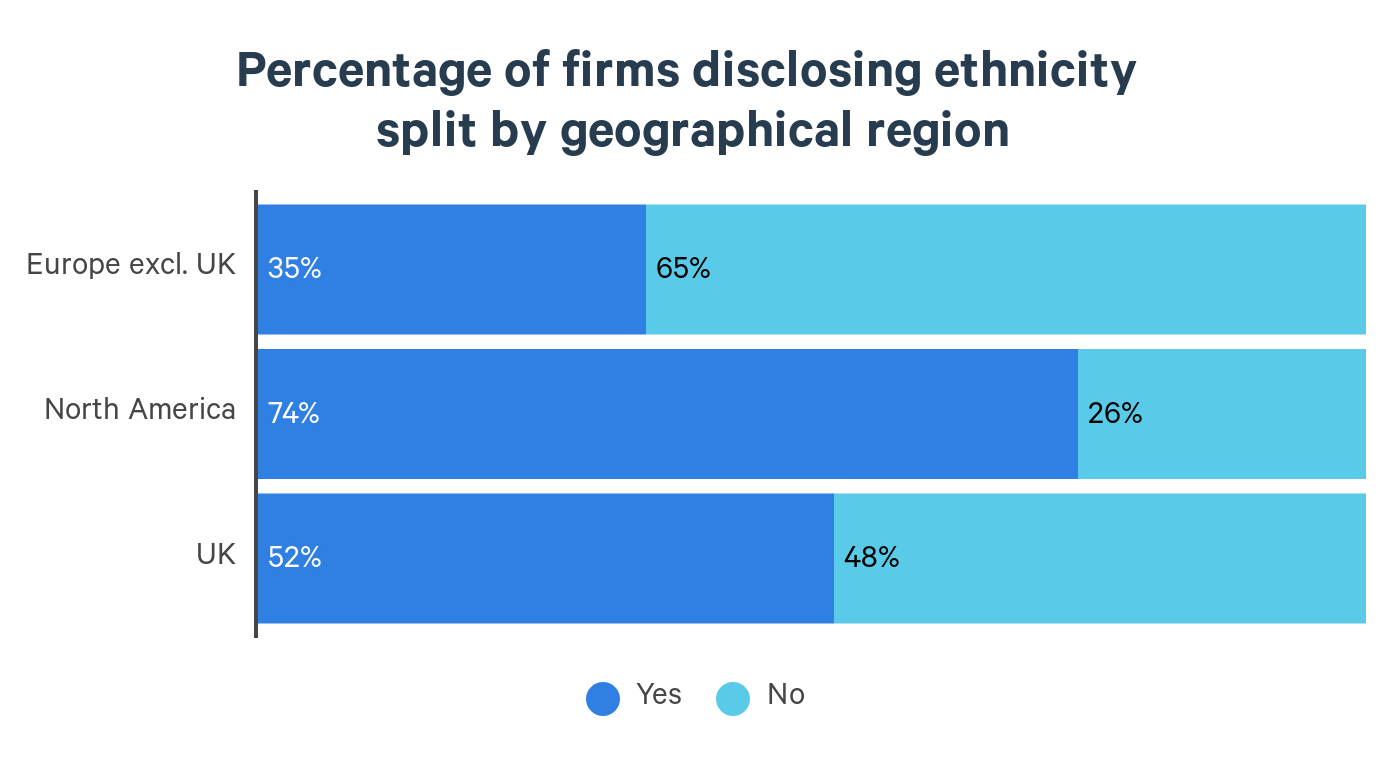

Ethnicity disclosure appears to be weaker in Europe from our survey. This is also a trend indicated within wider research. One of the reasons cited for this is legal and privacy concerns in Europe relating to ethnicity disclosure. European data protection laws, such as the General Data Protection Regulation (GDPR) enforce stringent rules on how personal data, including ethnicity data, can be collected and processed.

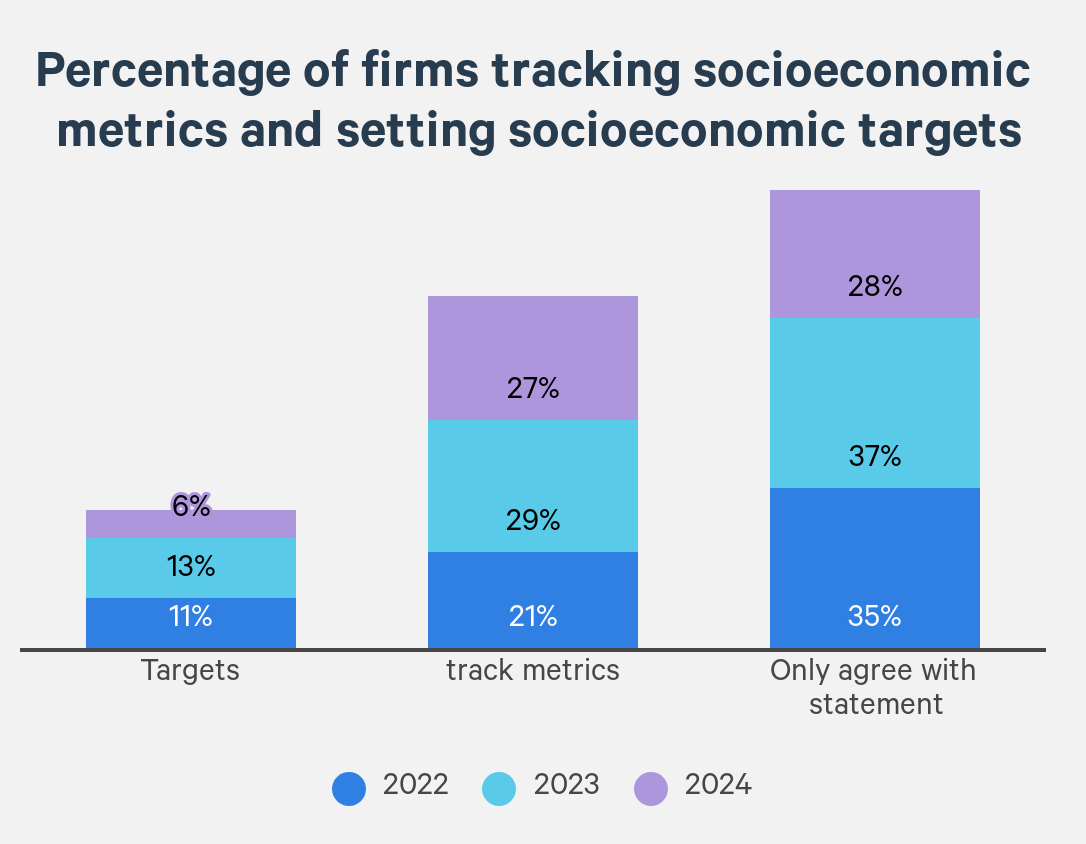

We have seen a worrying negative trajectory regarding socioeconomic metrics. The percentage of managers with socioeconomic targets has been decreasing since 2022, with this more than halving in the last year (13% in 2023 vs. 6% in 2024). However, with the onset of new social mobility guidance from industry bodies such as The Diversity Project, the pressure is only set to heighten in this area.

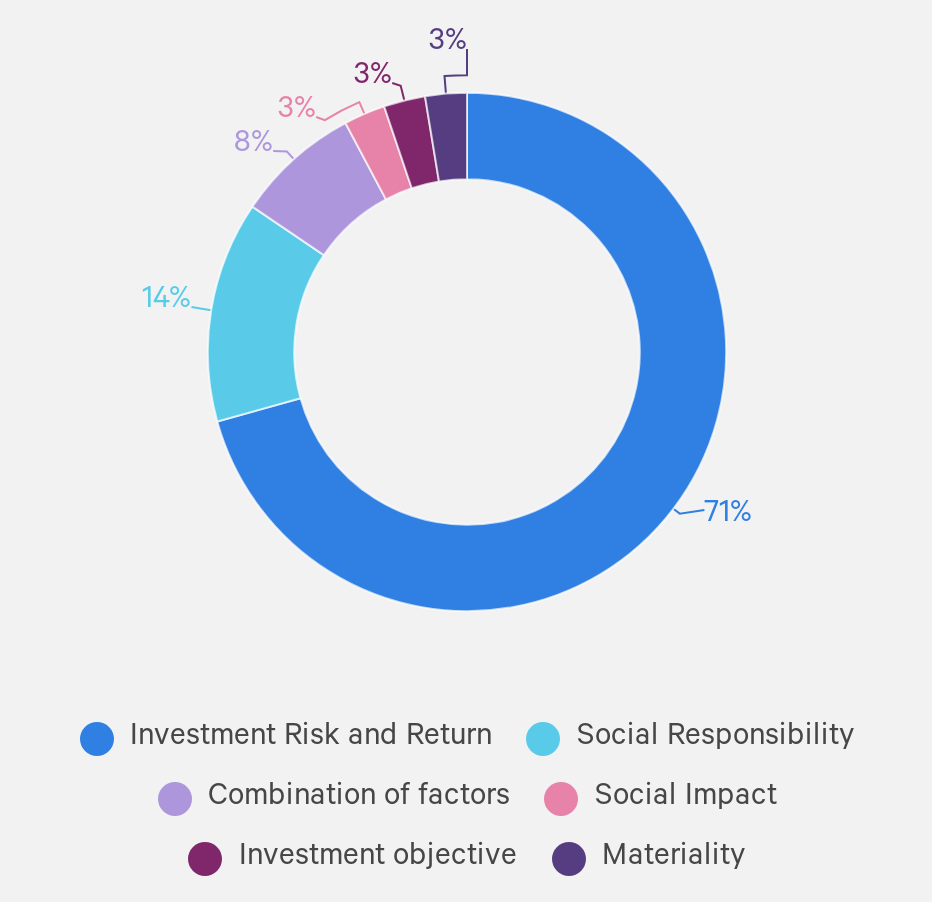

Where DEI is considered, it’s being driven almost three quarters of the time by investment risk or return considerations.

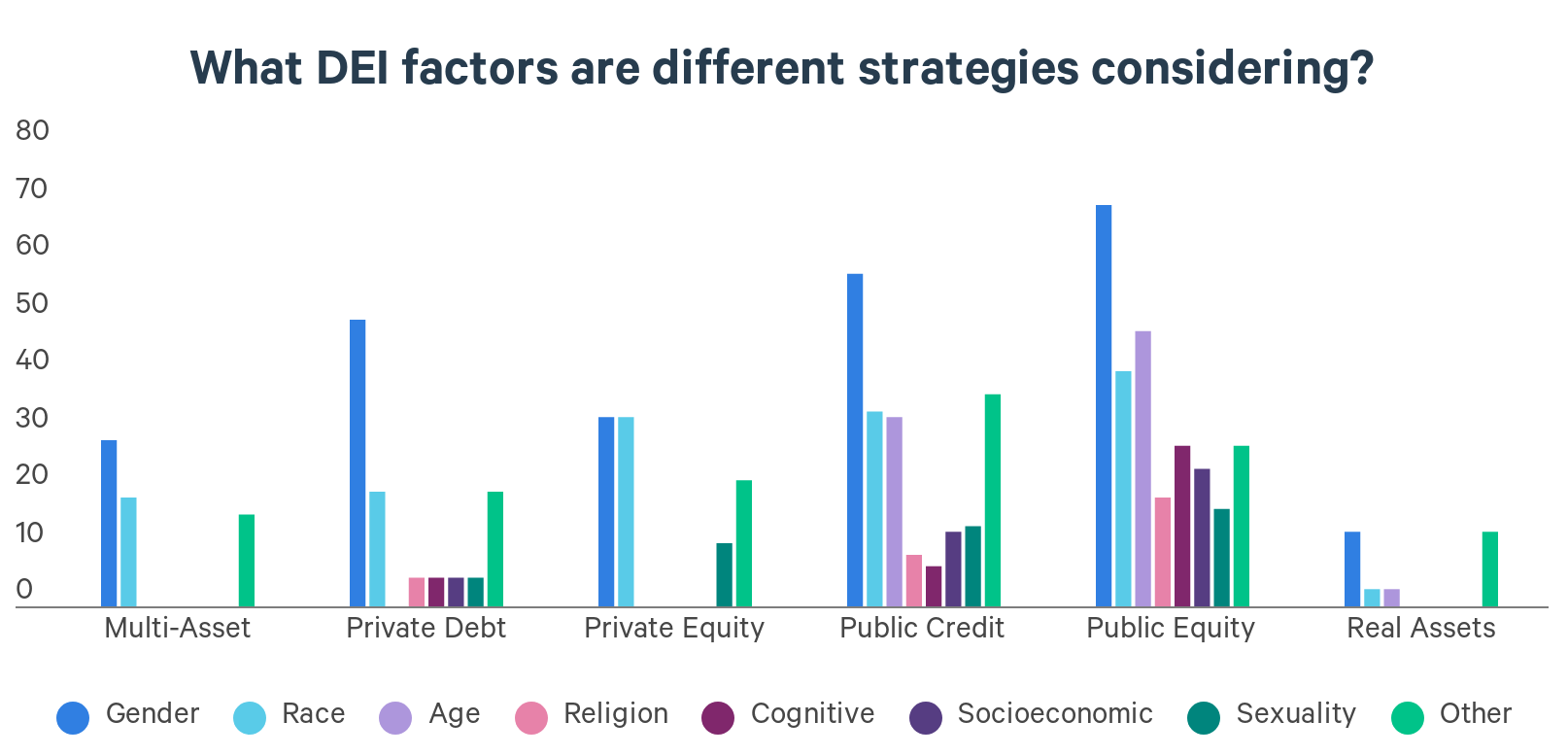

We also found that the biggest focus on DEI within the investment process was post-investment engagement with portfolio companies.

Where DEI factors are considered, it’s focused around gender and race and primarily in public equity.

Within the investment industry gender has arguably been the most talked about, targeted and reported diversity metric over the last few years. So why are we still struggling with significant underrepresentation and pay gaps when it comes to women?

Representation remains stagnant with on average 1 woman for every three men in investment teams.Additionally, only 3% of firms disclosed percentages for genders other than male or female.

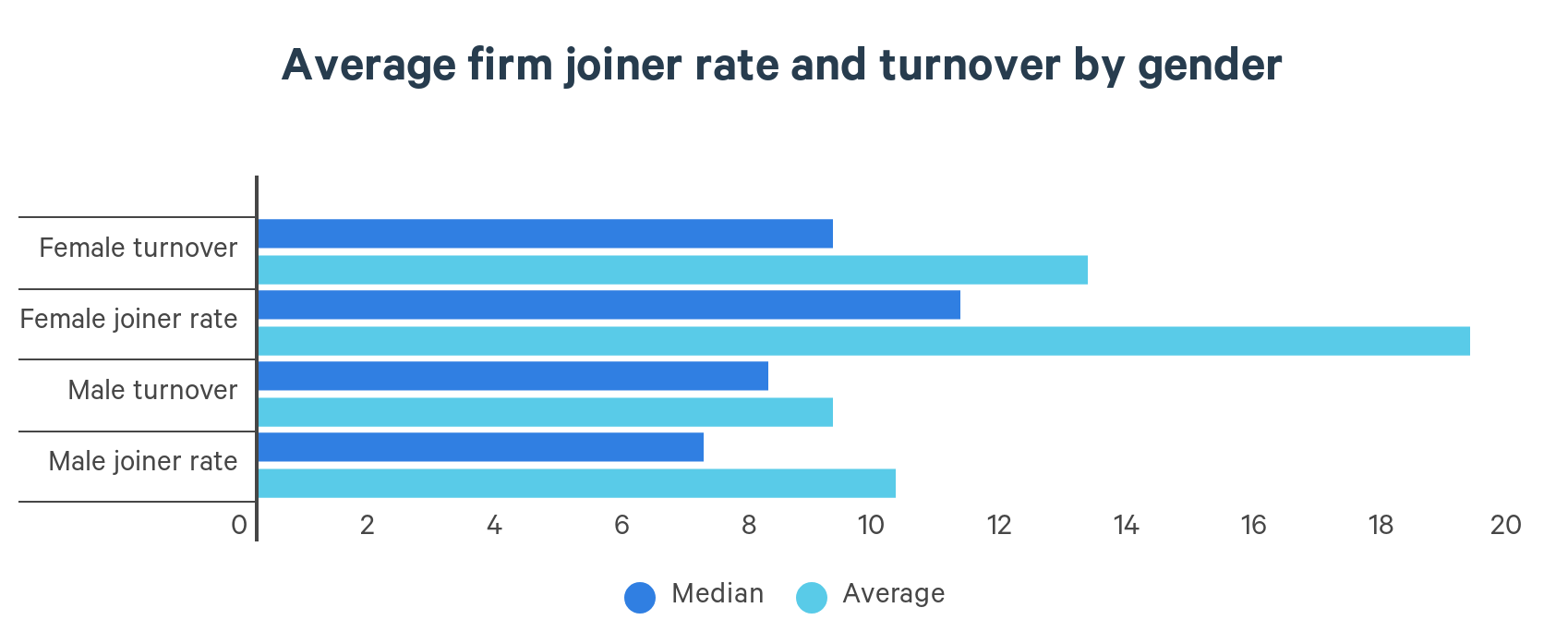

Across the survey we continue to notice a positive sentiment regarding recruitment numbers, with a higher average joiner rate for investment teams for women than men. However, the average turnover rate for women is comparatively higher than for men – 13% on average compared to 9% for men.

This is a trend identified in wider industry research; the average turnover rate for female fund managers was 42% in 2023, compared to 28% for male managers.1

It’s worth noting that turnover varies geographically and by size of firm, with smaller firms showing higher female turnover on average and also Europe showing higher turnover than the UK and North America.

Gender remains the most common target set by firms (40%), followed by ethnicity (28%) and inclusion (22%). However, the proportion of managers with gender targets has decreased slightly since last year, and just 27% are targeting a specific timeframe.

Targets are vital to ensure that inclusion and diversity goals are not just aspirational, enabling managers to track and measure progress over time and demonstrate their commitments in practice.

The fact that the majority have not set a specific timeframe is concerning. Concrete timings make the targets meaningful, and encourage continued momentum for reaching objectives as well as giving firms the opportunity to consider at specific intervals whether progress is sufficient and, if not, how initiatives should be changed.

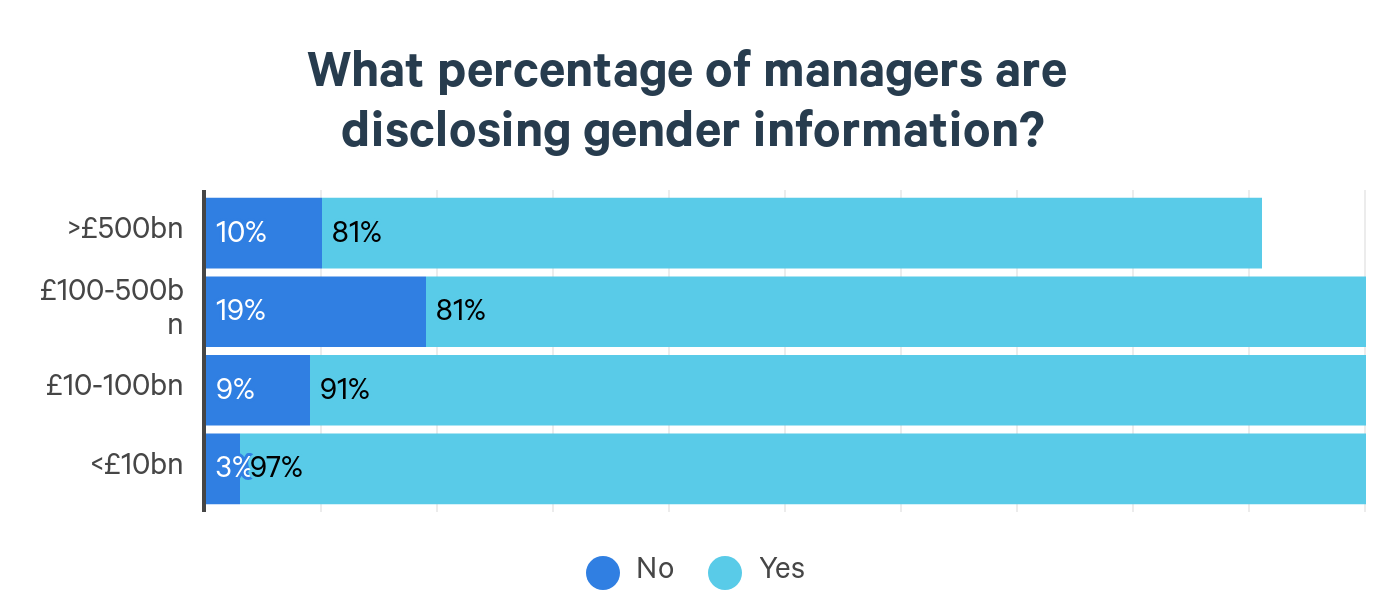

Gender disclosure, although high, largely seems to be driven by the size of the company. Firms under £10bn in size are more likely to disclose gender information, with the percentage of firms claiming to disclose gender decreasing as AUM increases. This is interesting, given that evidence suggests that smaller firms are more likely to lack the resources to collect and report gender data.2

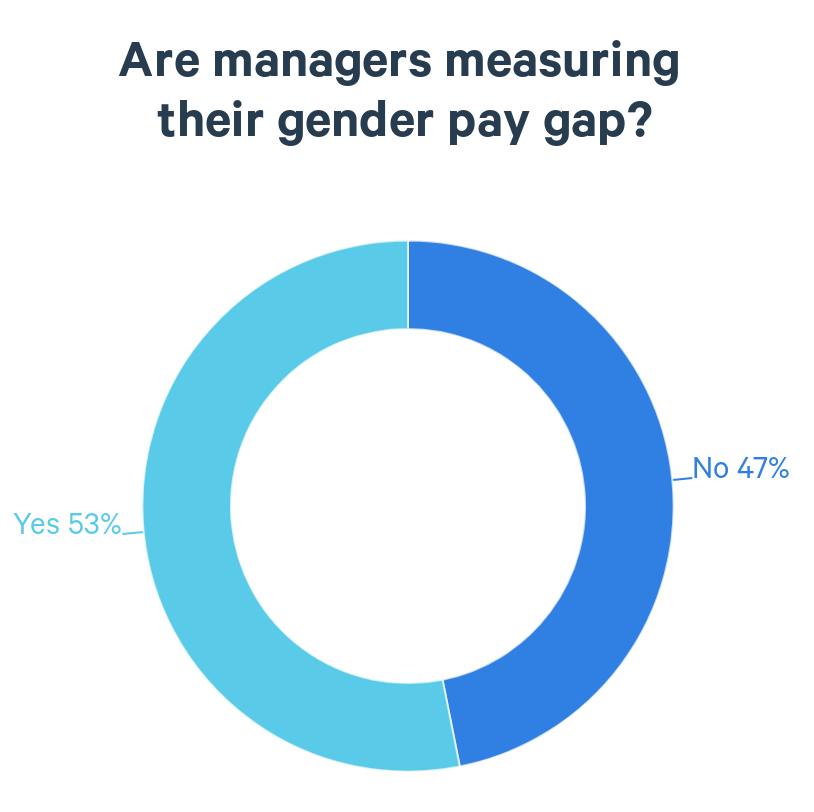

The proportion of managers measuring both gender (and ethnicity) pay gaps for each reporting period have increased since last year. This year 53% of managers measured their gender pay gap compared to 50% last year and 27% measured their ethnicity pay gap (up from 24%). Whilst there is still significant progress to be made, this is a clear step in the right direction.

When comparing sectors, the financial sector gender pay gap in 2023 was the highest out of any sector, and by a significant amount3. This may be indicative of fewer senior women being in post – and therefore women either leaving before they are promoted, or not being promoted at all.

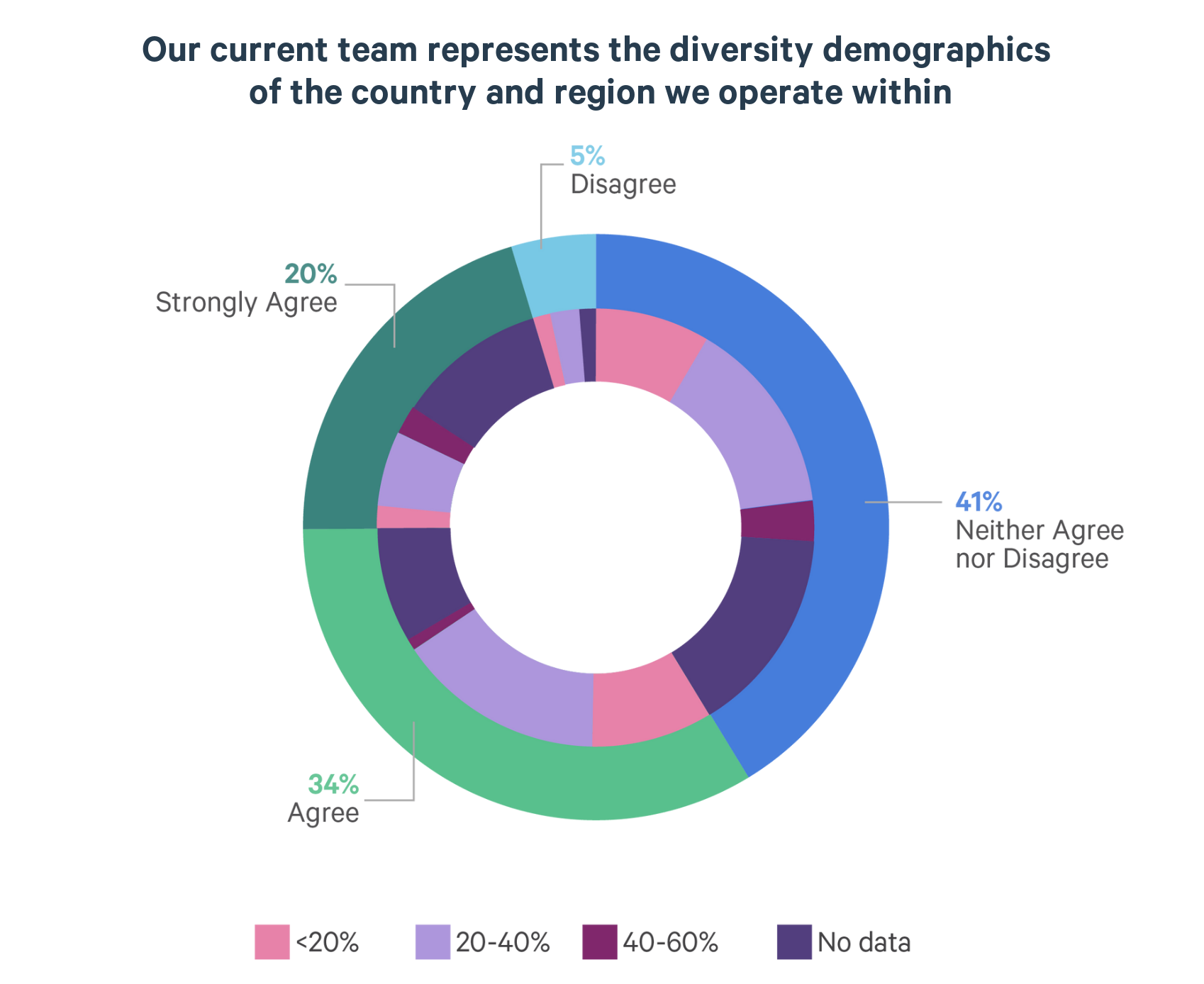

There continues to be a mismatch between female representation within a firm and female representation across the broader working population. Whilst most firms agree that their investment teams are representative of the region they operate in, only 6% of that group had teams of 40%-60% of women disclosed. None had greater than 60%.

Our data has shown that firms with any of the four initiatives below on average show greater representation of women in investment teams:

Staff engagement survey undertaken in the last 12 months

Flexible working policy

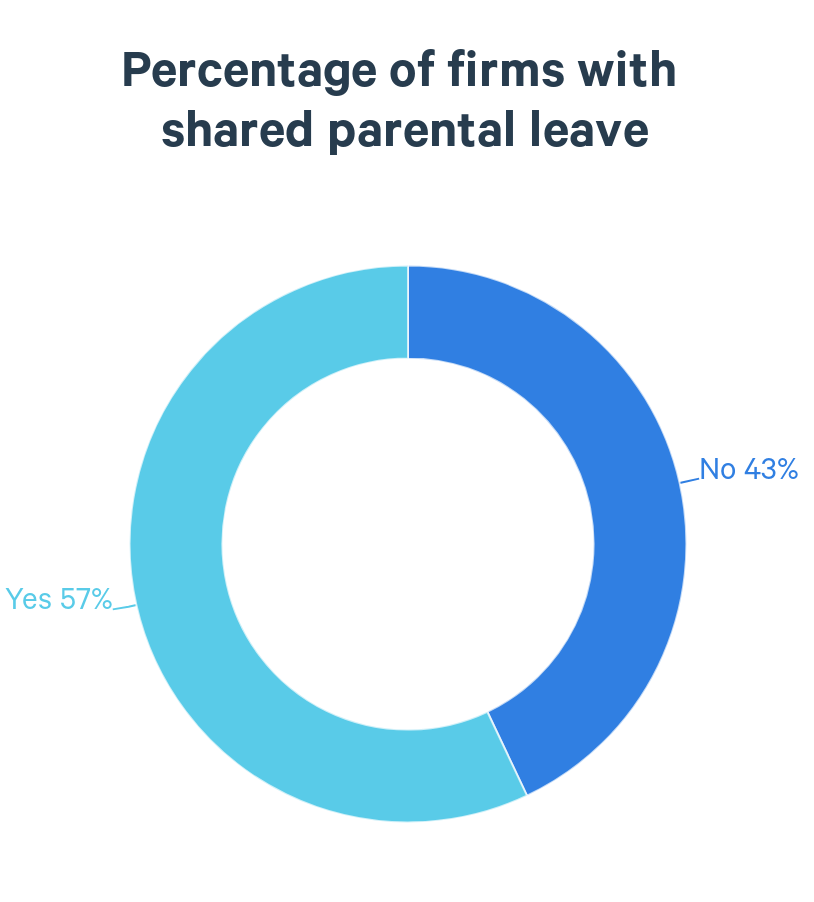

Shared parental leave policy

Diversity KPI’s linked to senior management remuneration

However, it’s important to remember that the above may not be the case for all investment firms, as many have particular nuances regarding their workforce.

We continue to think about what we as a firm can do to move the dial and make improvements.

We held our second roundtable this year with clients, prospects and investment managers to discuss how we can address the barriers to female progression in the investment industry. From the discussion, we highlighted five proactive steps companies could implement to help prevent women leaving:

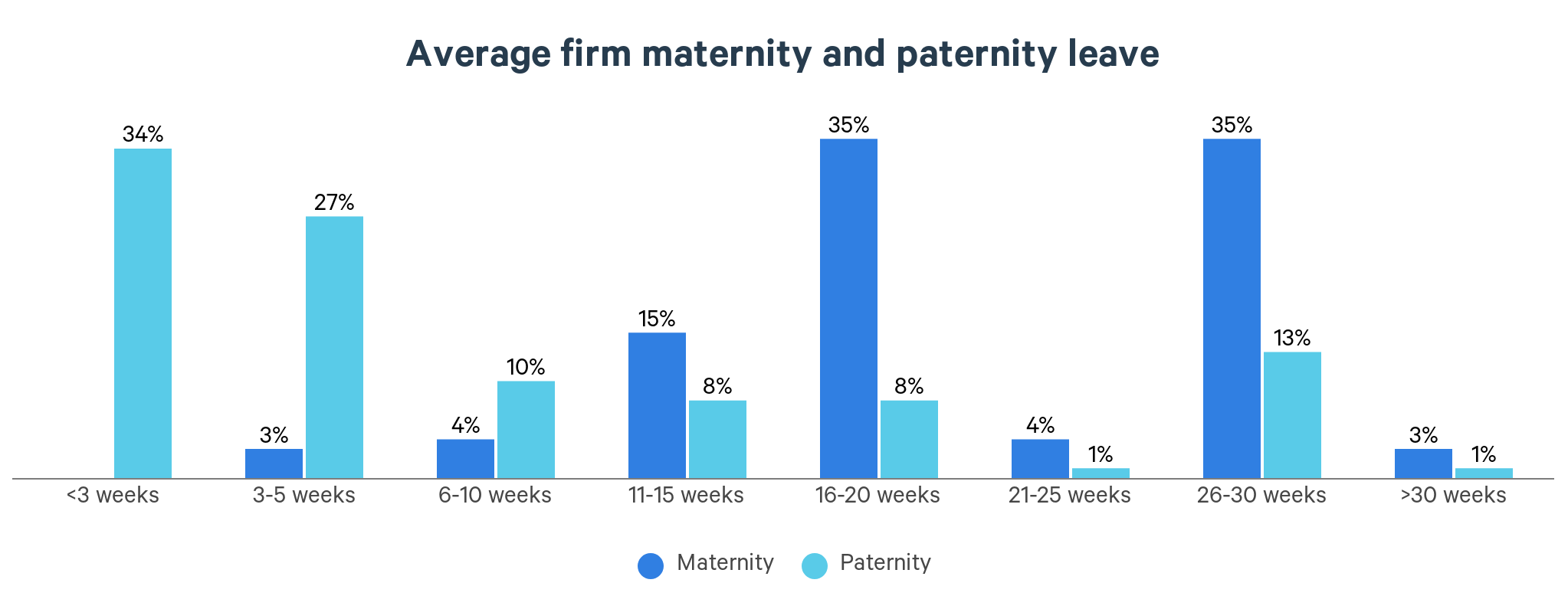

Look to enhance parental leave packages wherever possible. The average number of weeks of full pay offered in a maternity leave policy sits at 16-20 weeks, whilst for paternity leave this is 3-5 weeks.

Replace ‘years experience’ with the actual skills required in job specs and promotion processes.

Remove, limit or change meetings away from core childcare hours (e.g., around school pick up and drop off).

Advocate and sponsor women in businesses – promote women when they are not in the room and to people that do not have exposure to them.

Review and create menopause-related policies and coverage in private health insurance.

We also engage with managers on DEI topics. We regularly collect both gender and turnover data from managers as part of our due diligence and continuously challenge on female representation.

Reducing female turnover and increasing retention is crucial for overall representation and will most likely reduce business costs associated with rehiring. When women stay longer within their roles, they have more opportunities to progress and grow their careers, enabling them to shape and influence the industry. For example, women in senior roles can advocate for policies which support gender diversity such as parental leave.

This helps to attract more women to the industry and gradually shift the gender balance.