IMPACT & EMERGING THEMES

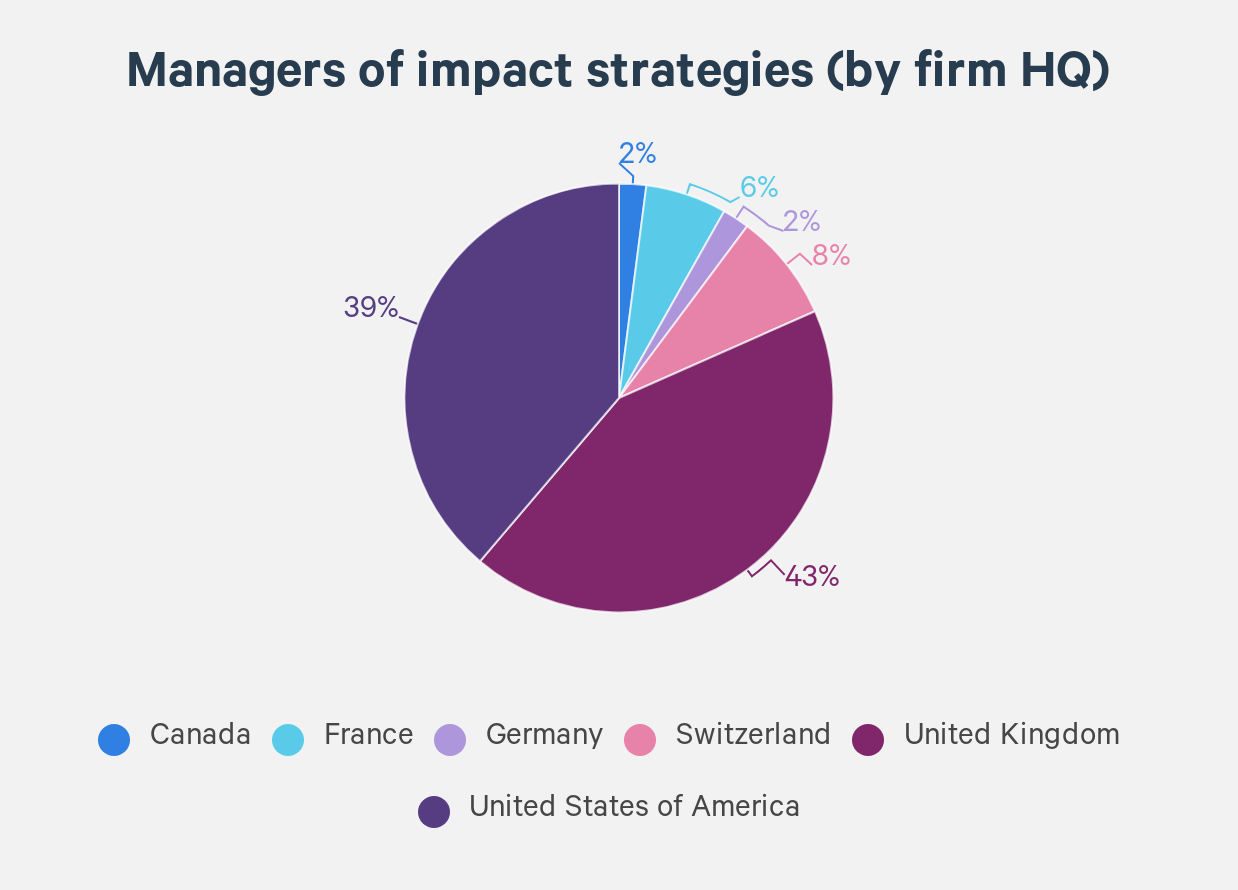

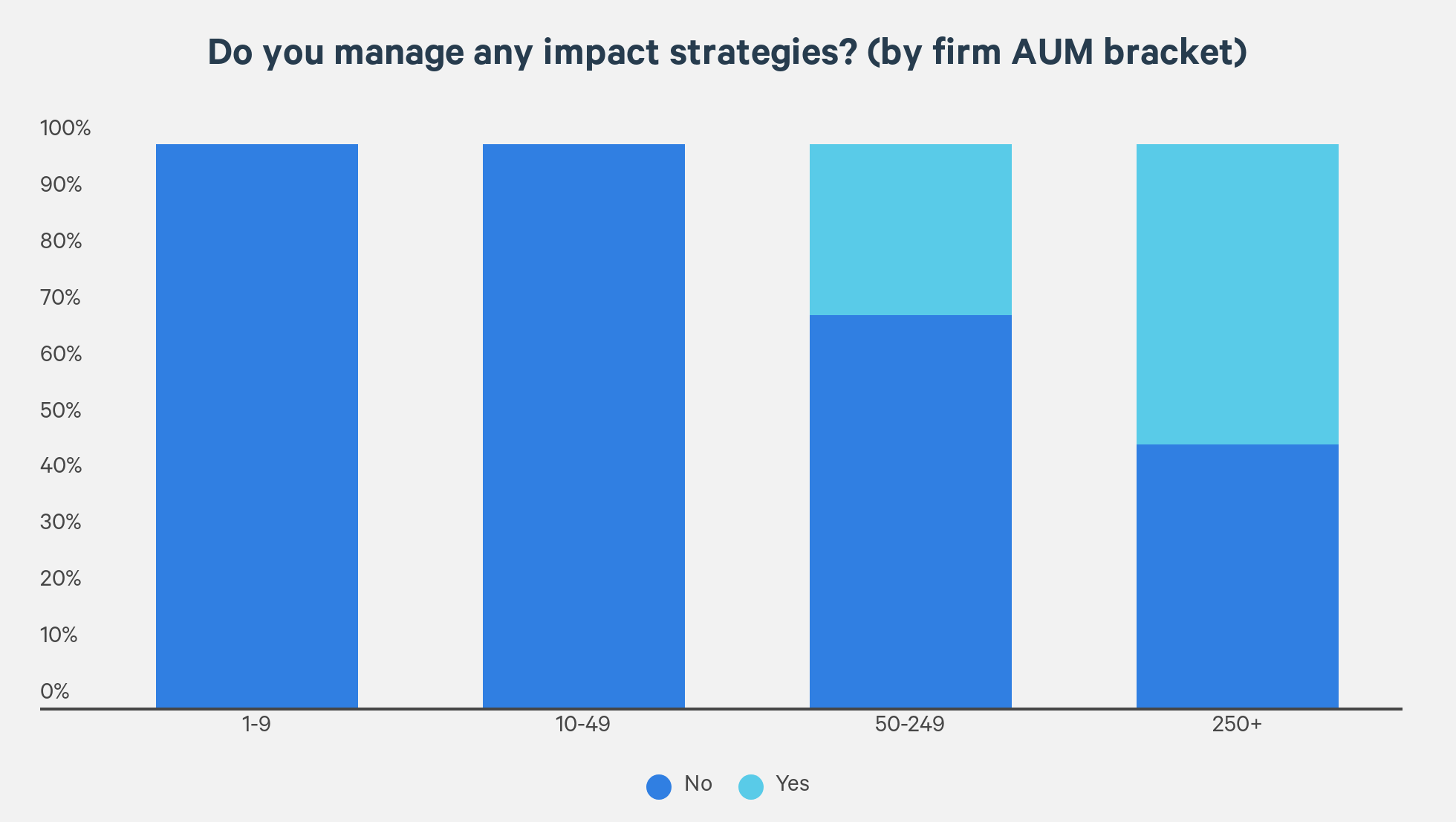

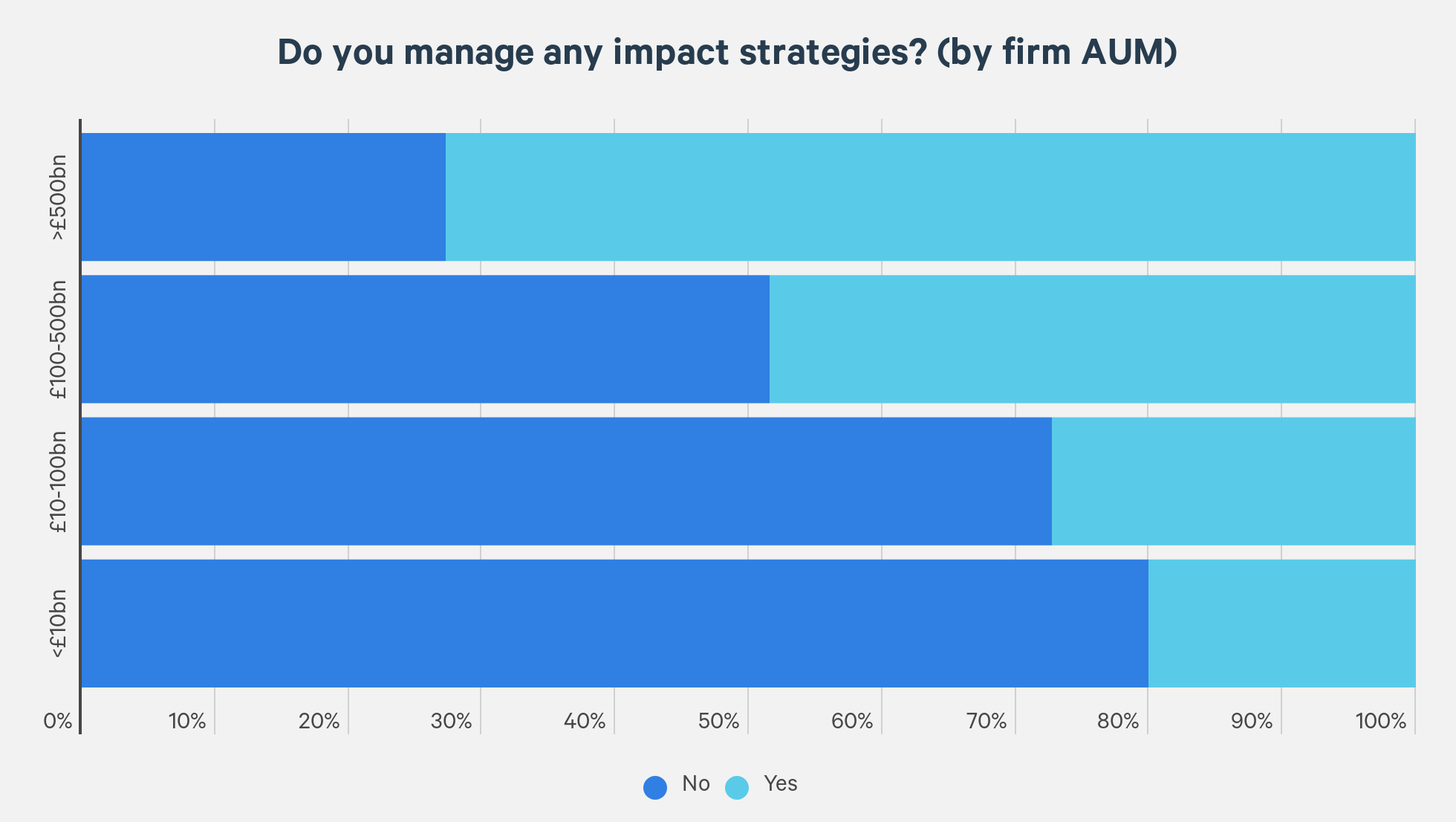

Larger firms continue to lead the impact charge

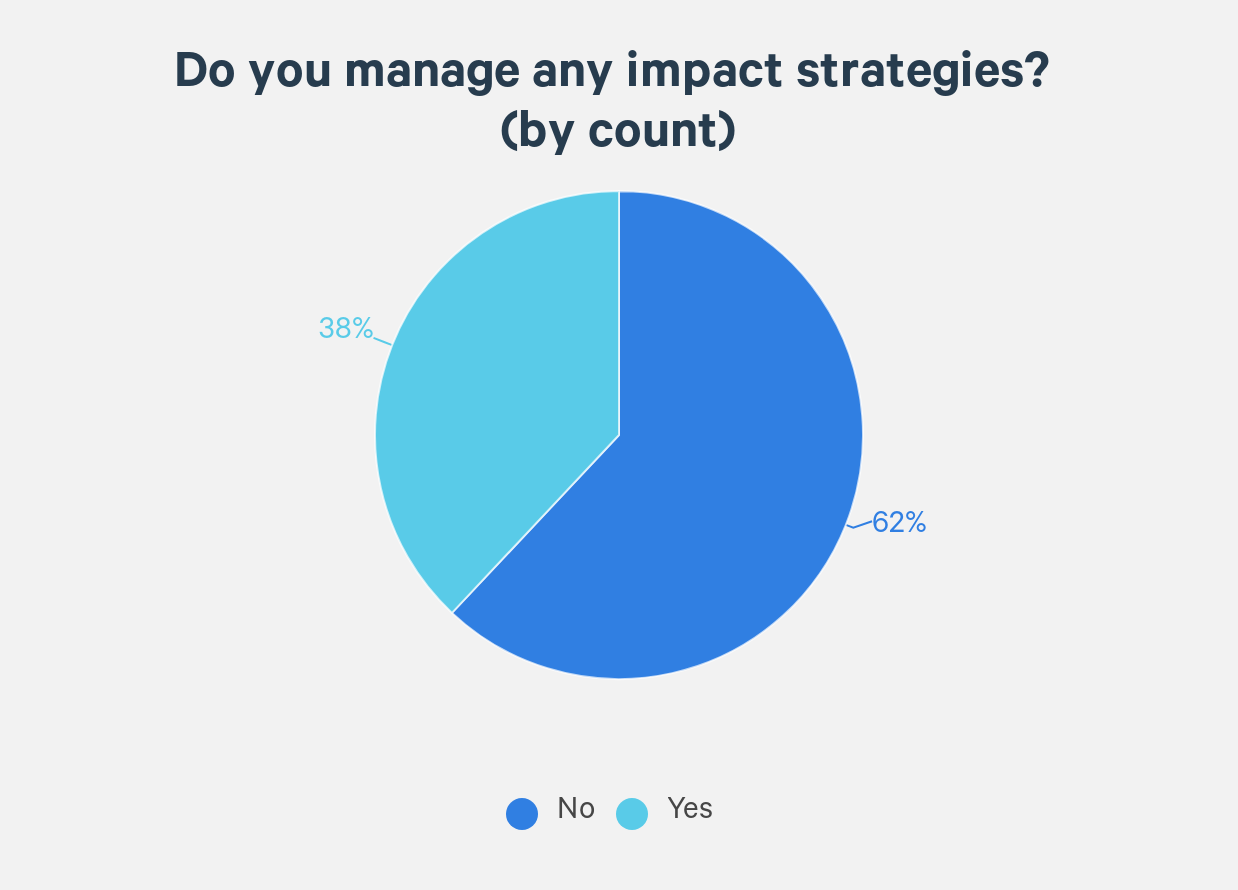

of managers in our universe reported managing at least one impact fund, with total impact AUM amounting to over £220bn

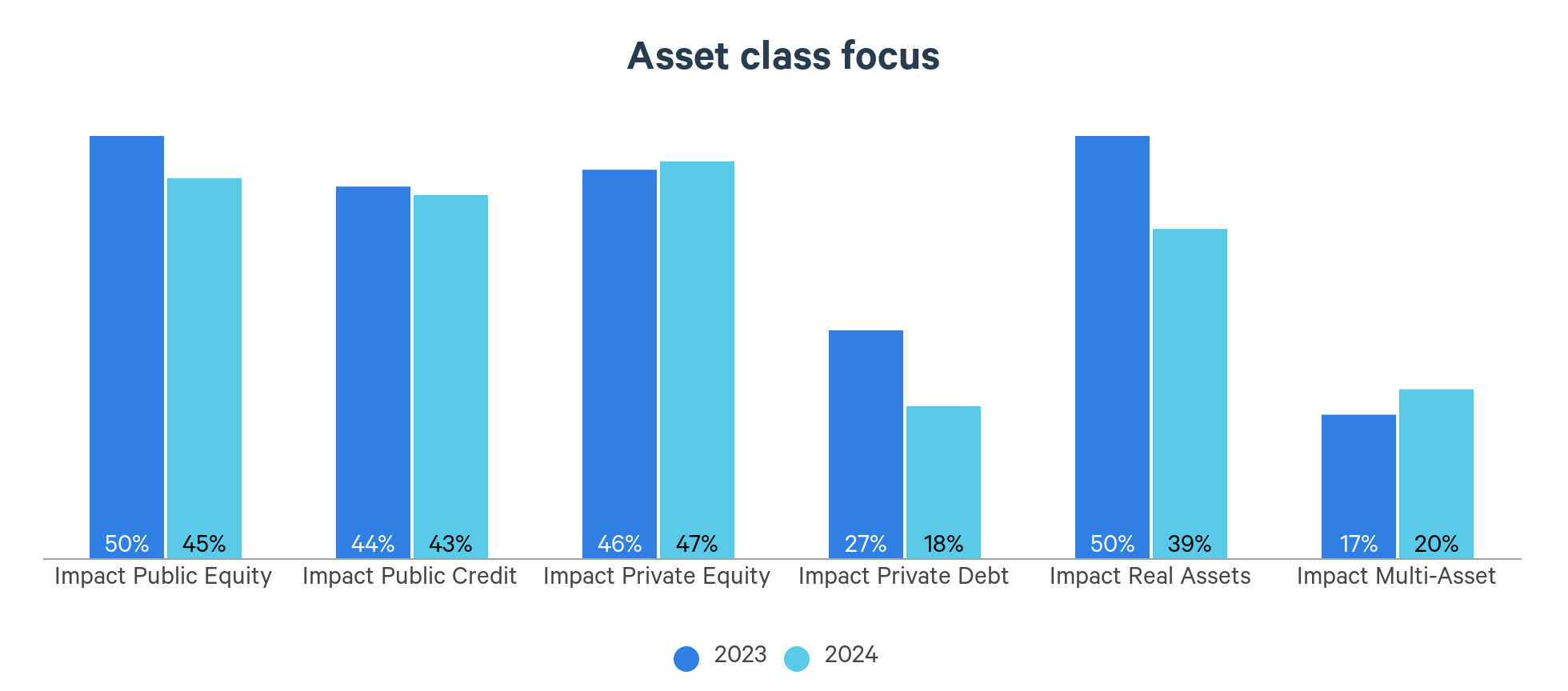

There were notable decreases in private debt (27% in 2023 vs. 18% in 2024) and real assets space (50% vs. 39%).

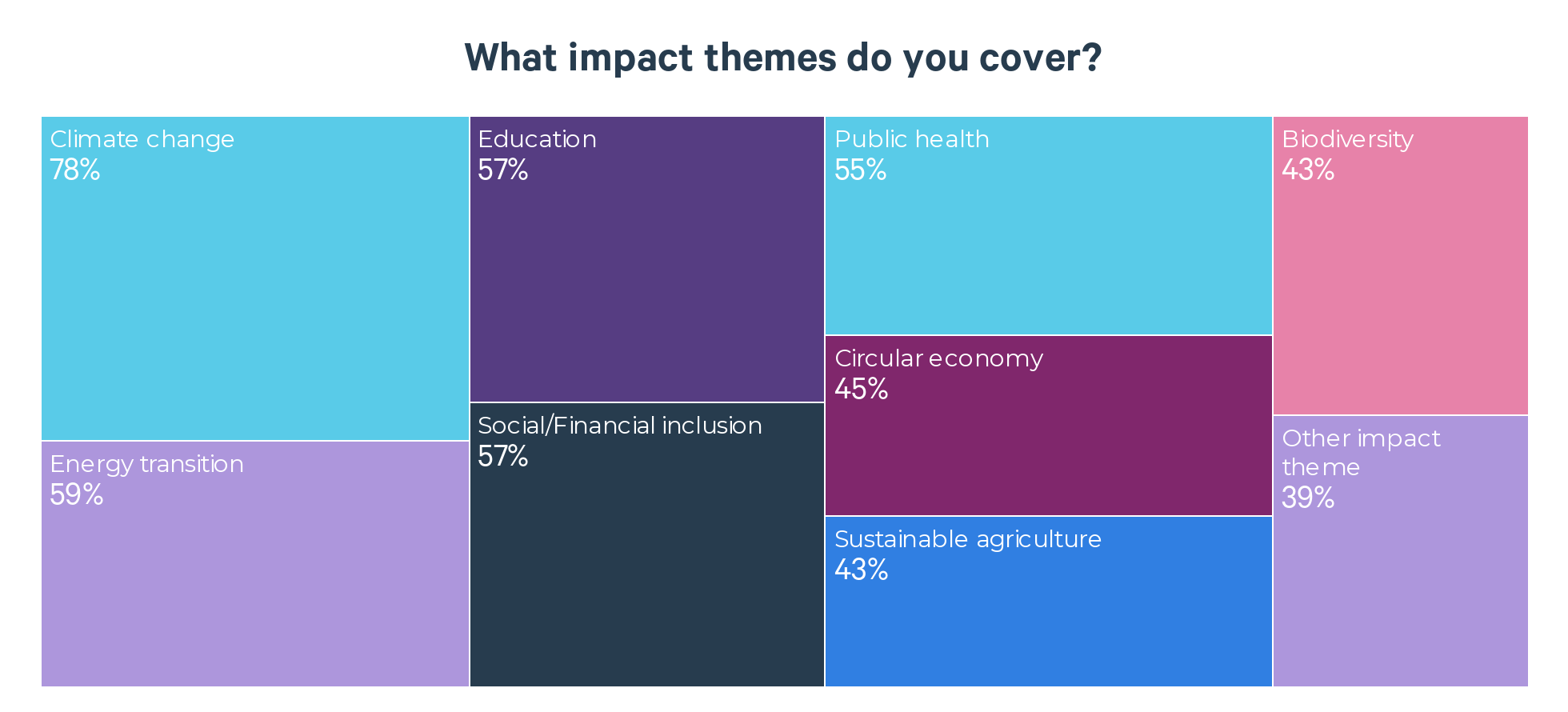

In terms of impact themes covered

of managers cover the climate change

cover the energy transition

“The decrease in managers claiming to offer impact solutions in private debt and real assets is interesting as 2024 has seen us research, rate, and allocate client capital to impact managers across both asset classes.”

From an asset class perspective, the proportion of managers claiming to run impact strategies across various asset classes has dropped.

Climate change

Energy transition

Social and financial inclusion

Education

Public health

Circular economy

Biodiversity

Sustainable agriculture

Other

Modern portfolio theory aims to optimise expected returns for a given level of risk – a balance that traditional investors have been attempting to manage for decades. Yet, as systemic risks like climate change and social inequity materialise, we see a third element grow of notable importance on the investor agenda: impact.

According to research by the Global Impact Investing Network, impact capital is increasingly flowing from asset allocators to asset managers, with pension funds accounting for the largest proportion of impact manager capital at 20%1. If we look at Redington allocations, we have about £7bn of client capital invested in sustainable and/or impact-listed equity strategies and billions more across private markets.

Through this survey, we continue to engage with managers on approaches to impact investing to better understand the impact status quo. About 39% of managers in our universe reported managing at least one impact fund, with total impact AUM amounting to over £220bn (or 0.5% of total assets under management). The story relative to last year remains the same: larger and better resourced firms tend to be more likely to run an impact fund. This makes sense as impact investments typically necessitate additional technical expertise and further due diligence, monitoring, and reporting to meet both financial and impact objectives.

Whilst the ‘who’ in impact investing seems to be much of the same compared to last year, there has been a shift in the ‘how’ and ‘what’. For example, from an asset class perspective, the proportion of managers claiming to run impact strategies across various asset classes has dropped, with notable decreases in private debt (27% in 2023 vs. 18% in 2024) and real assets space (50% vs. 39%).

There has been a ‘crack-down’ on impact-washing in recent years, with increased scrutiny being placed on managers by regulators and fines being issued for those overstating capabilities and/or sustainability results.

As a result, there has been increased reticence or conservatism from managers when making impact or sustainability labelling claims (e.g. the EU’s SFDR or UK’s SDR). Anecdotally, we hear that compliance teams increasingly encourage managers to err on the side of caution when including references to sustainability in investor material given uncertainty around what constitutes non-compliance. Whilst we do not place emphasis on the labels managers assign to their products when we conduct our due diligence and assign ratings, we are supportive of efforts to increase standardisation and transparency with regards to impact objectives, processes, and outcomes.

The decrease in managers claiming to offer impact solutions in private debt and real assets is interesting as 2024 has seen us research, rate, and allocate client capital to impact managers across both asset classes. From an environment-focused private credit manager and a real estate manager providing housing for those with high social need, to a firm focused on sustainable land management, we have been exploring impactful solutions that provide investors with risk-adjusted financial returns alongside positive real-world outcomes and have found particularly attractive opportunities here. It is worth mentioning that, whilst the impact investing universe may be broadly categorised as emergent relative to traditional investments, our ratings and allocations to impact funds this year have spanned from established teams/funds with multi-year track records to first-time funds innovating in a particular space.

From a thematic perspective, managers remain focused on climate change and the energy transition. However, as investors get more sophisticated and start to look at sustainable investing more holistically, increasing attention is being paid to social issues such as financial inclusion, education, and public health. In the past year, we have had a number of clients – particularly in the charities and LGPS space – who are seeking to broaden their investment remit to specifically target the ‘S’ in ESG. We are continually working to upskill ourselves and our clients, and continue to assess interesting investment opportunities in the social realm.

Health as a theme is an area that we are currently researching across asset classes to identify areas that may be attractive for clients. Earlier in the year, we specifically queried managers on health investing to help inform our next steps.