CLIMATE CHANGE AND NATURE

How are managers addressing the biodiversity crisis?

Very important

Somewhat important

Somewhat unimportant

Very unimportant

Not sure

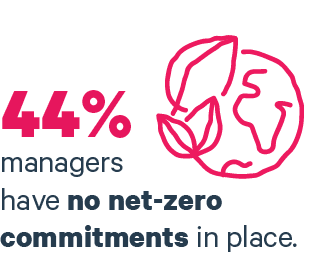

of managers have no net-zero commitments in place, up from 43% in 2023.

of managers said they consider biodiversity and nature-related criteria when making investment decisions.

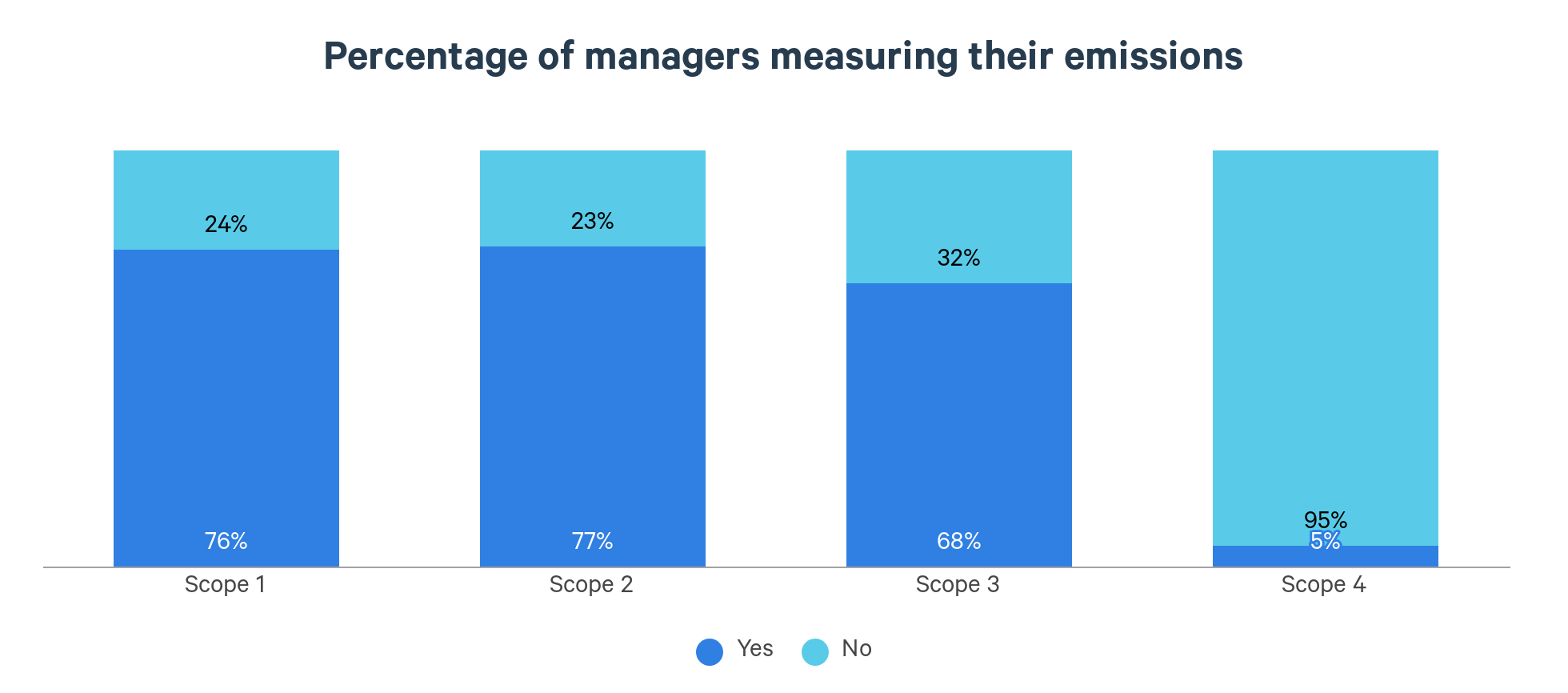

For 2024, there was a higher percentage of managers reporting that they don’t measure emissions (21% compared with 19%)

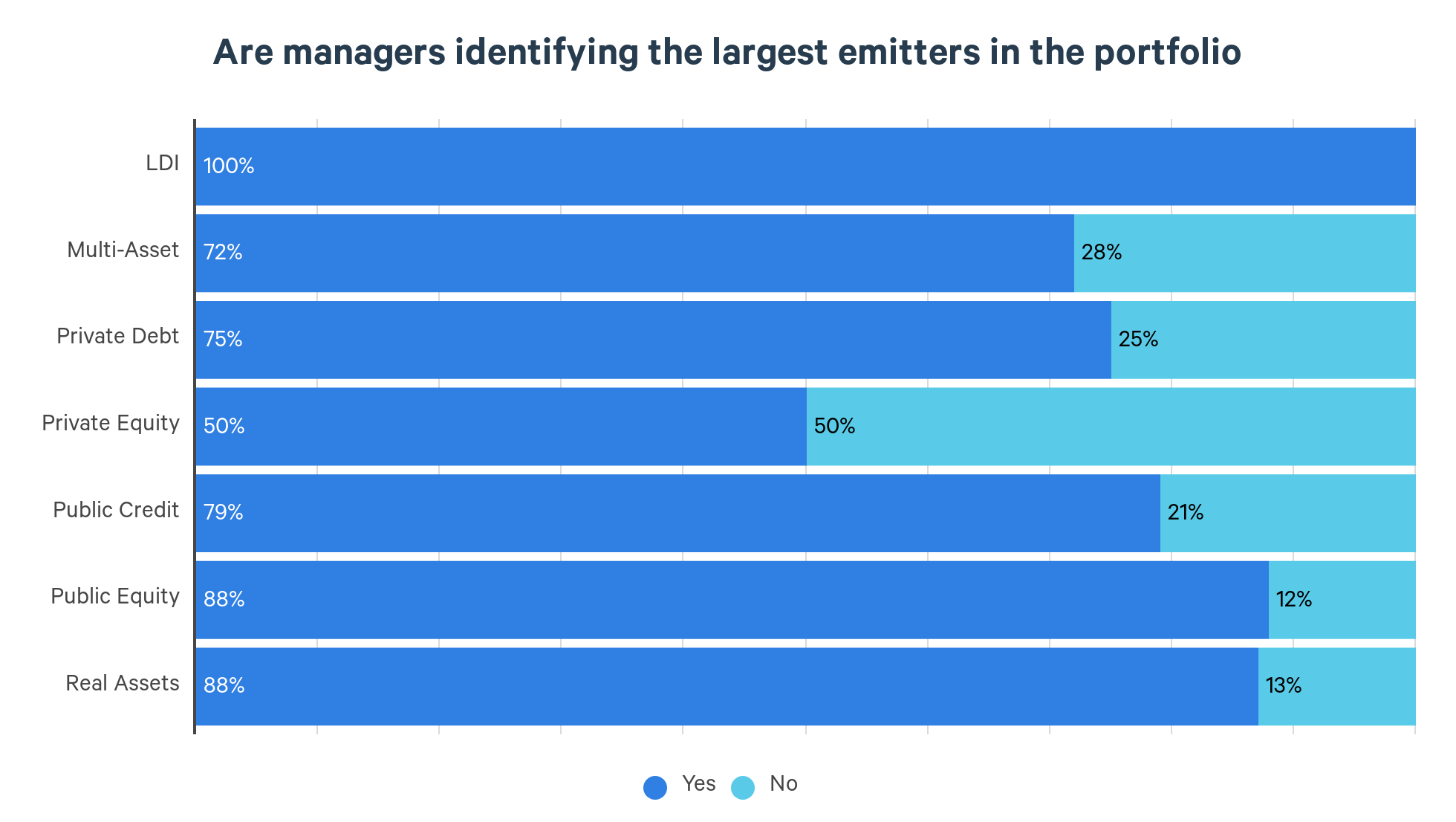

71% of managers identify the largest emitters in the portfolio, a crucial step in investors’ climate journey.

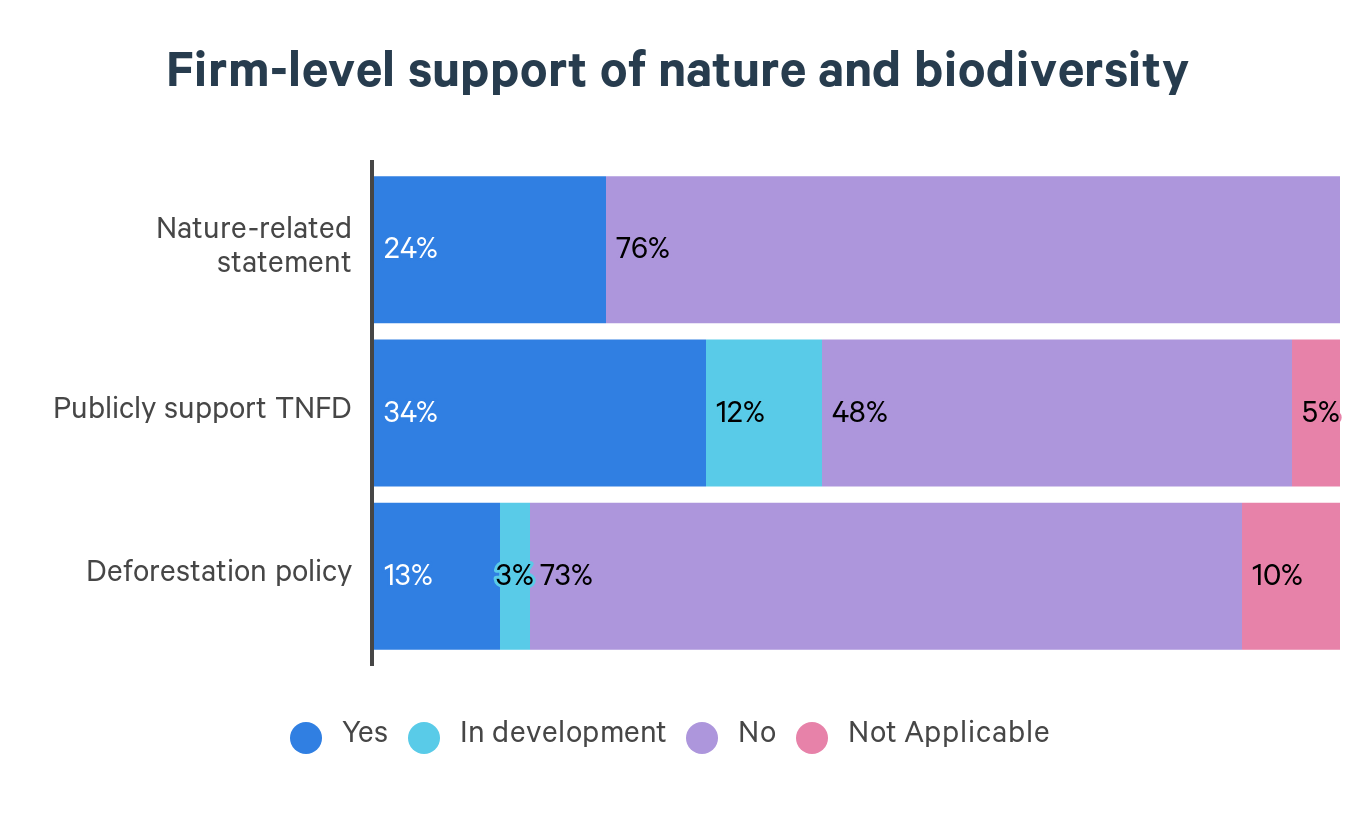

Nature is an issue rising rapidly up the agenda for many asset owners. The increasing biodiversity crisis, combined with the advent of the reporting standard from the Taskforce on Nature-related Financial Disclosures (TNFD), is leading to increased attention.

This isn’t yet fully reflected among the investment management community. The majority of managers without a nature-related statement say biodiversity and nature-related risks and opportunities are integrated into the investment process where these efforts can contribute to value creation.

Some managers acknowledge they are at an early stage with biodiversity and nature-related research, with a lack of data making it harder to make a clear materiality case for integrating nature.

Others say their approach to nature is primarily engagement-based, where negative impacts to business activities are apparent. Some respondents referenced performing a bottom-up analysis which breaks down nature issues into tangible factors – such as pollution, supply chains and plastic packaging – which feed into biodiversity outcomes and are more in the control of management than broad measures of natural capital.

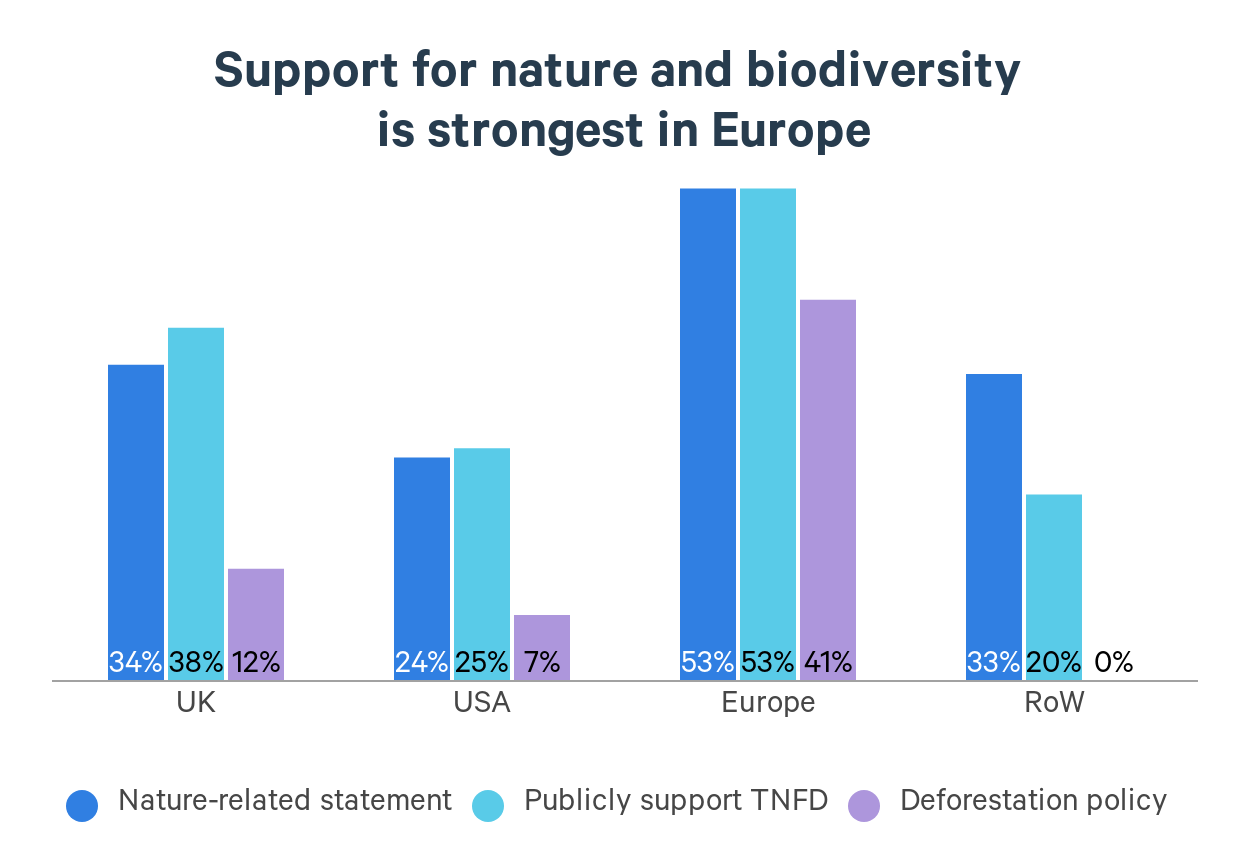

The EU’s strong regulatory framework regarding sustainability and biodiversity reporting is likely driving this divergence in the approach to nature.

As shown below, the EU’s support for TNFD is significantly higher than other regions. According to the TNFD, 43% of new adopters in 2024 were based in Europe, in comparison to just 6% from North America and Latin America and 3% from Africa and the Middle East. Data also indicates that Asia and the Pacific are also increasingly showing commitment to TNFD, comprising 42% of early adopters.1

Given that the TNFD recommendations are well aligned with other EU biodiversity standards, such as the European Sustainability Reporting Standard (ESRS), the comparability of data between disclosures is driving higher support.2

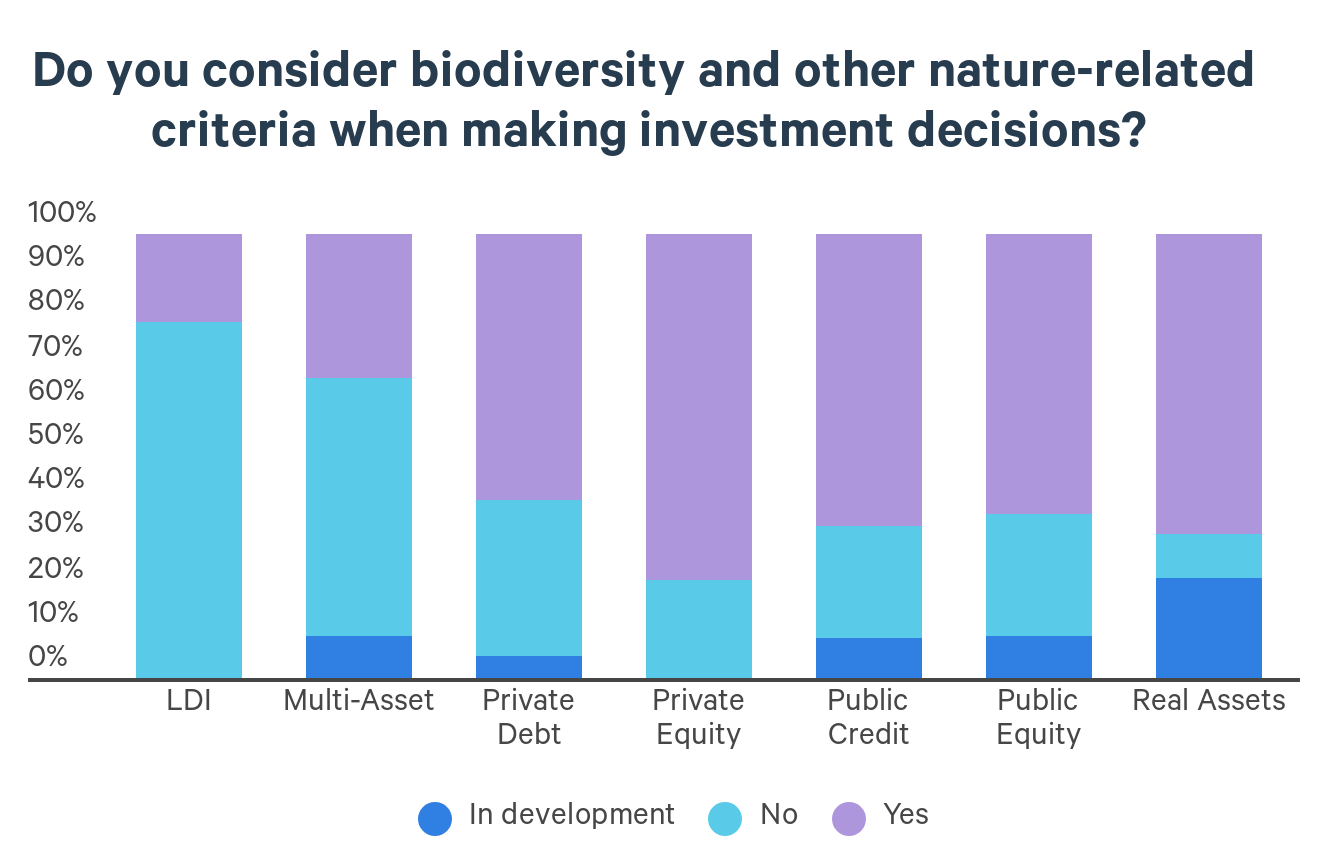

In total, 60% of managers said they consider biodiversity and nature-related criteria when making investment decisions. From an asset class perspective this figure sat at over 50% across PE, real assets, public credit, public equity and private credit.

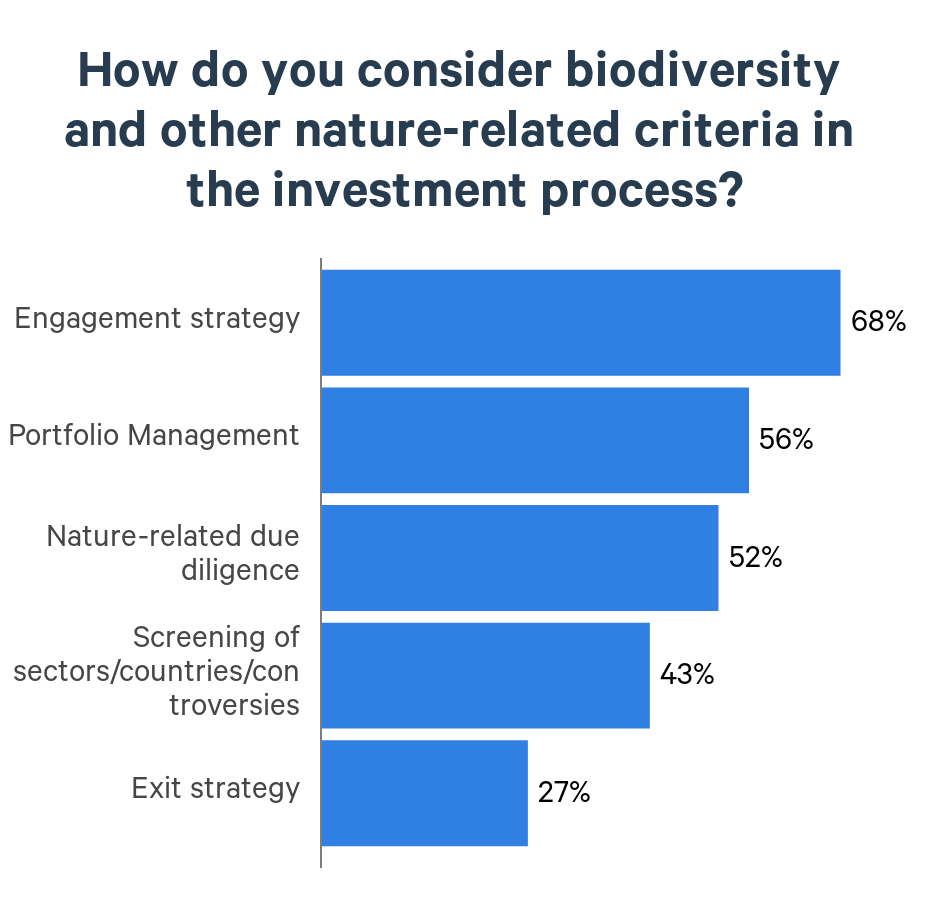

Managers claim the main challenges for incorporating nature considerations into investment process are insufficient access to high quality, reliable, standardised data and tools to measure performance. A lack of disclosure at the company level and difficulty in measuring risks due to the complexity of supply chains were also apparent.

An issue that was raised several times by managers was a lack of awareness on the importance of incorporating biodiversity into investment decisions and the need for further education on this topic.

Some (44%) managers have no net-zero commitments in place, up from 43% in 2023.

Of those firms with a commitment in place, the proportion working towards 2030 and 2045 targets has decreased slightly, with 2050 becoming proportionally more favoured.

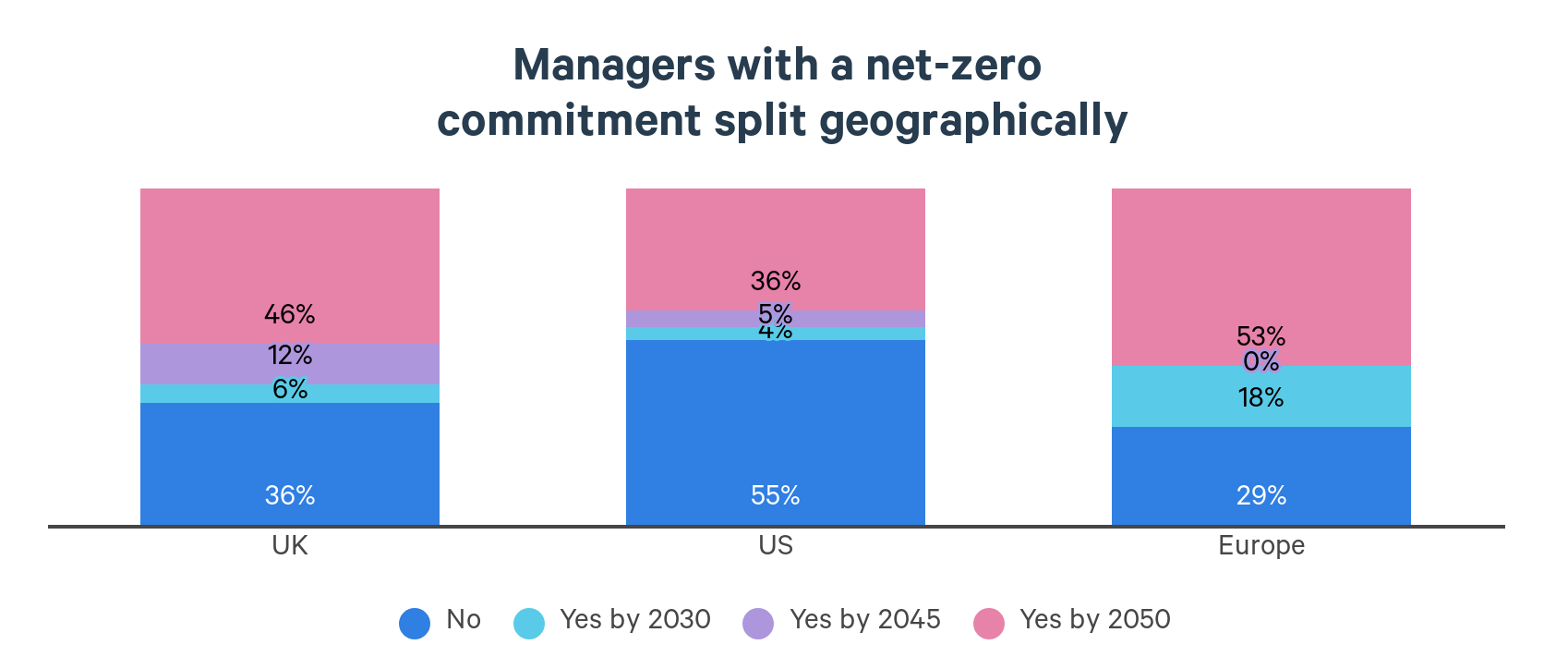

Looking at the geographical split of net-zero commitments, the US still lags considerably behind the UK and even further still behind Europe. This increasing divergence is perhaps unsurprising given the significant pushback on ESG commitments in the US and subsequent retreat from climate pledges and policies.

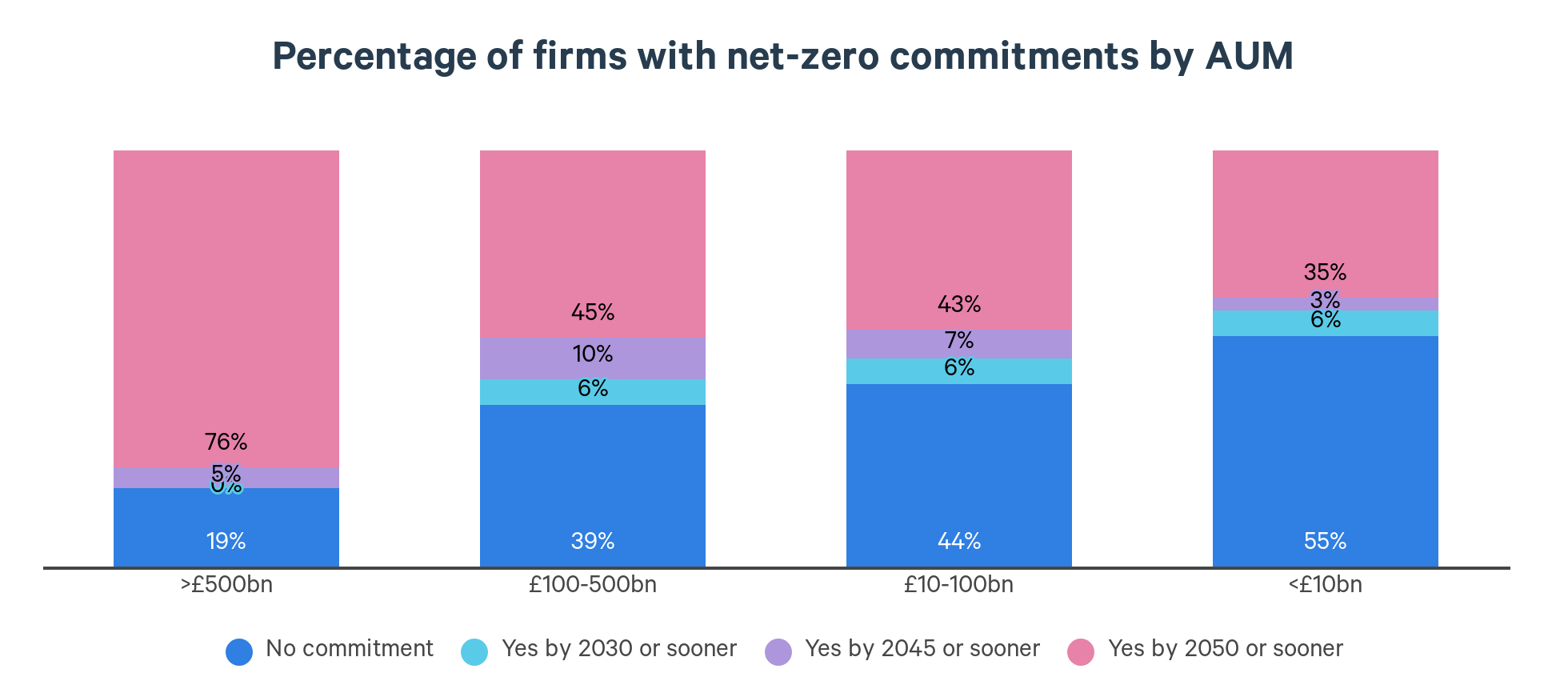

Firms with larger AUM are more likely to have set a commitment than those with fewer assets. 55% of firms under £10bn are yet to set commitments, in comparison to 19% of those over £500bn.

For 2024, there was a higher percentage of managers reporting that they don’t measure emissions (21% compared with 19%).

55% of firms under £10bn are yet to set commitments, in comparison to 19% of those over £500bn."

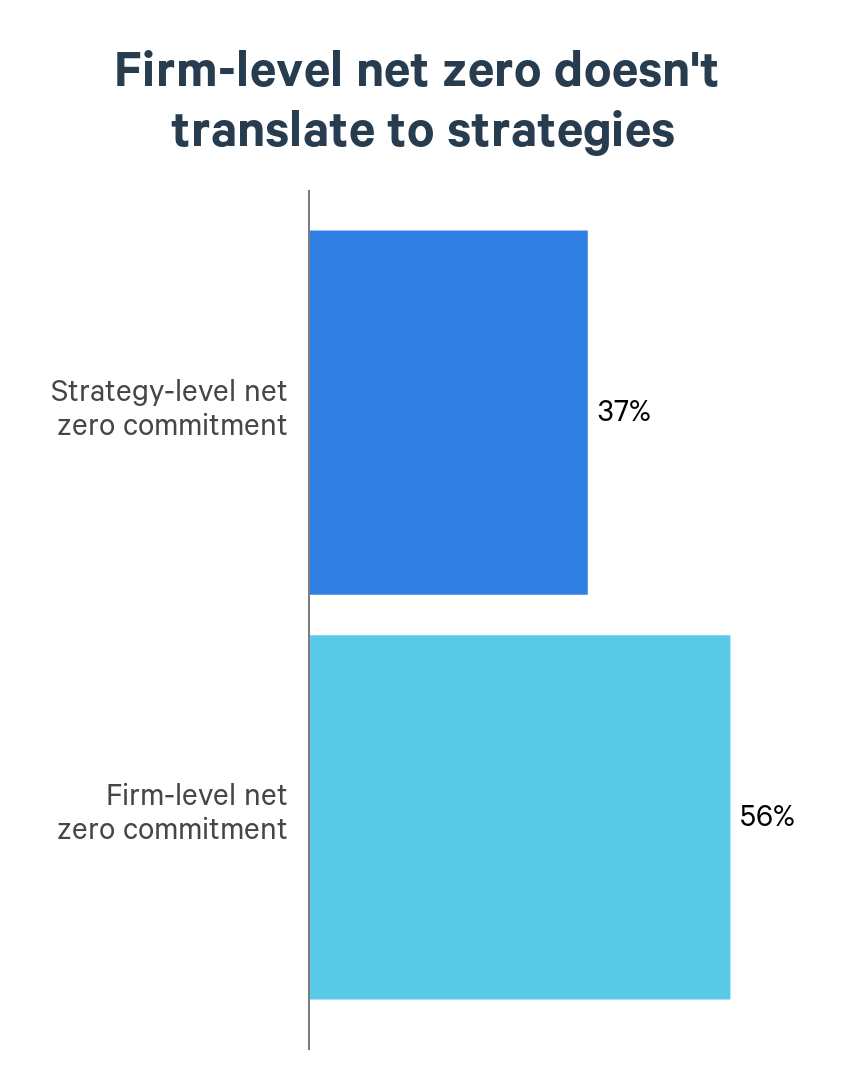

In addition, firm-level net-zero commitments aren’t translating to strategy level as we would expect.

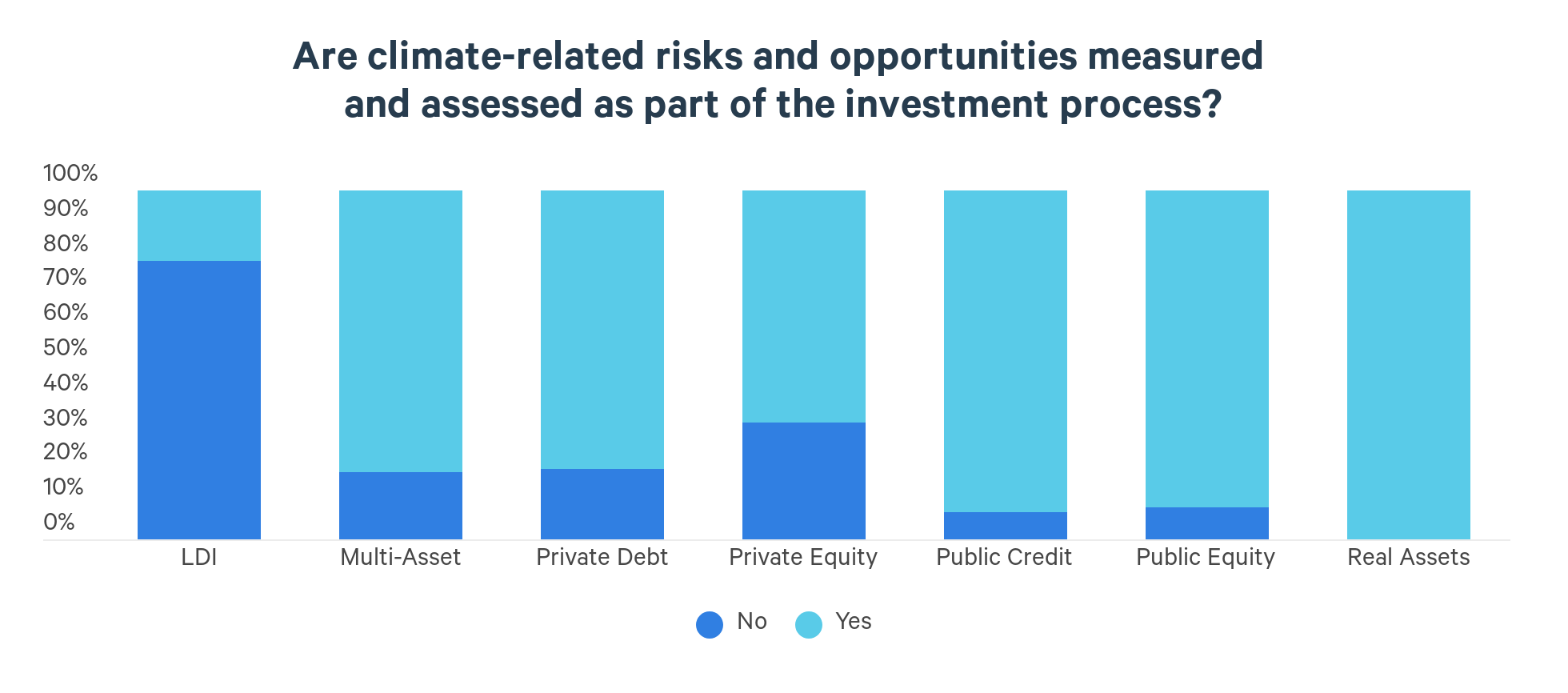

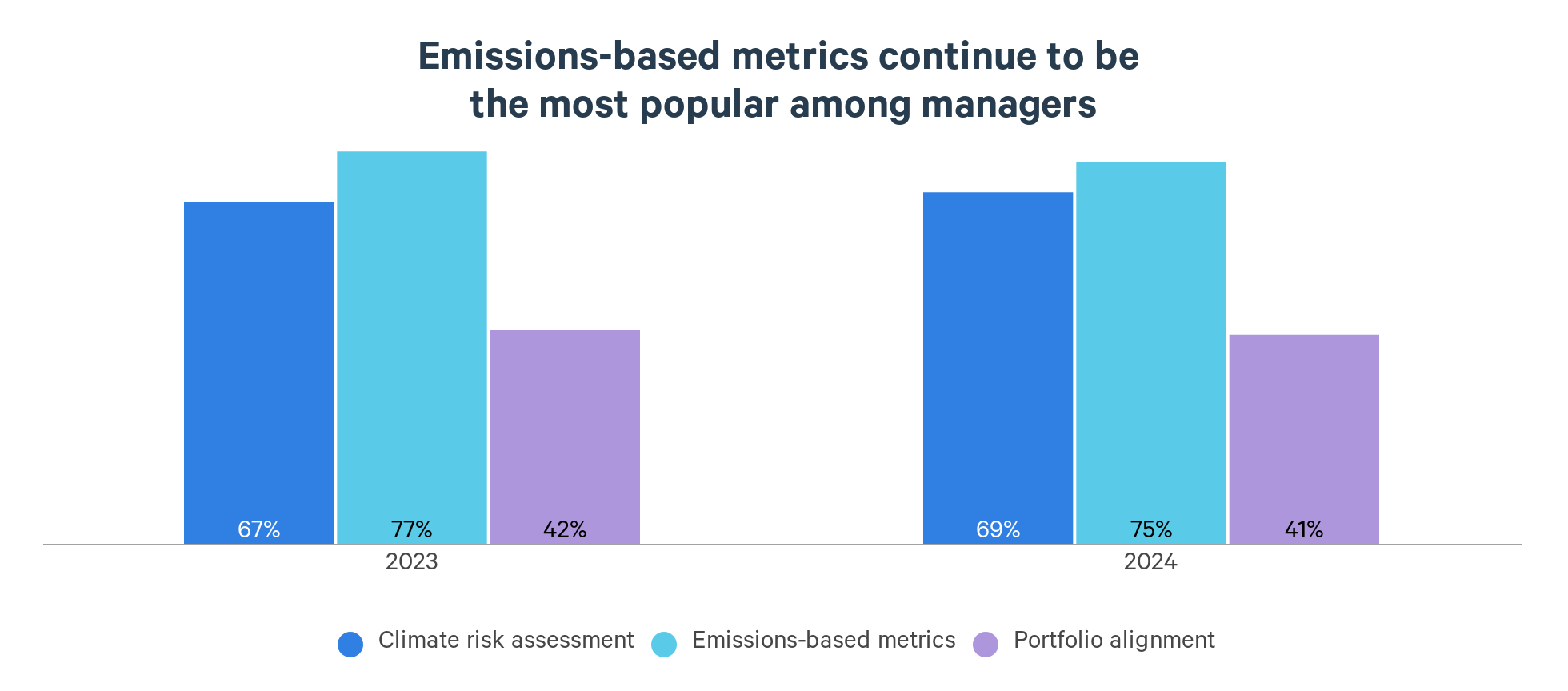

Overall, 88% of managers measure and assess climate-related issues in the investment processes, vs. 85% last year. While this is a slight improvement across the board, at a strategy level LDI continues to lag behind.

88% of managers measure and assess climate-related issues in the investment processes, vs. 85% last year."

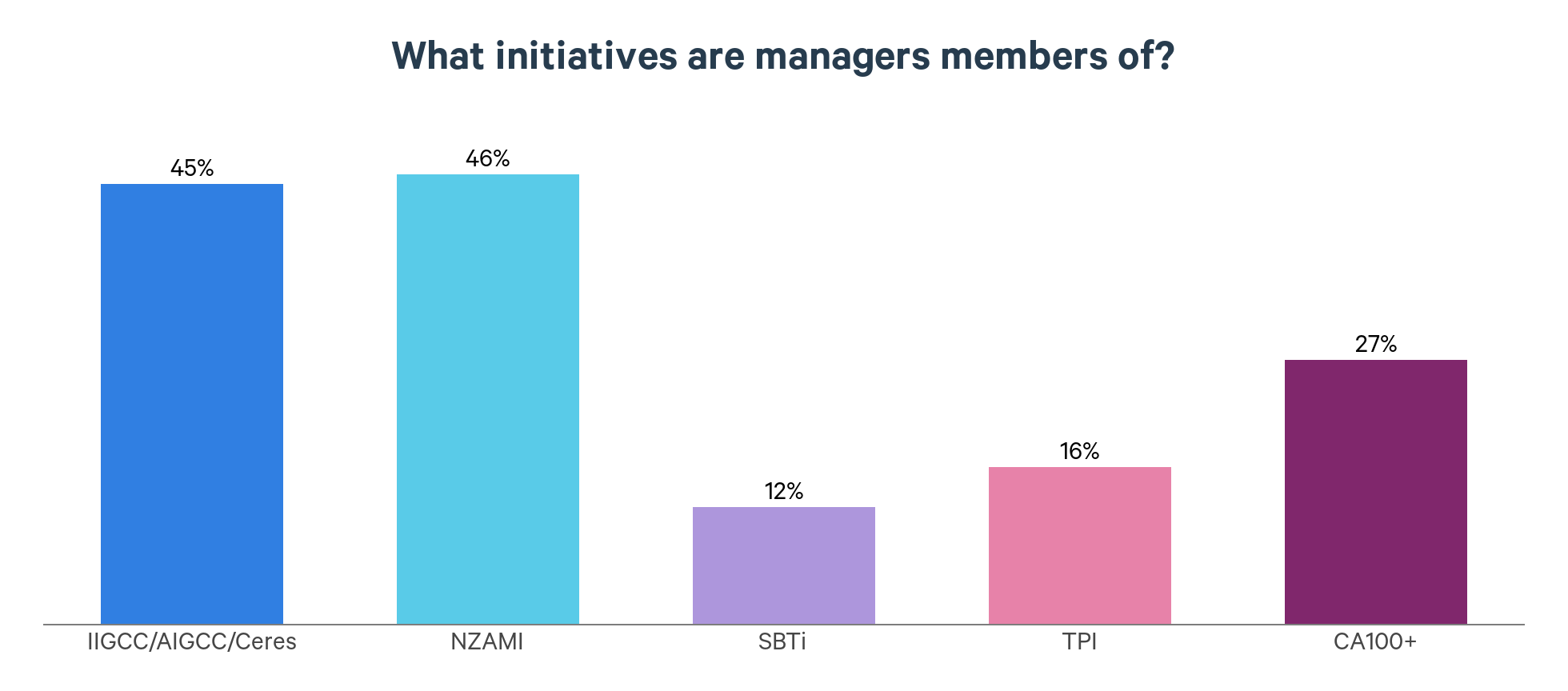

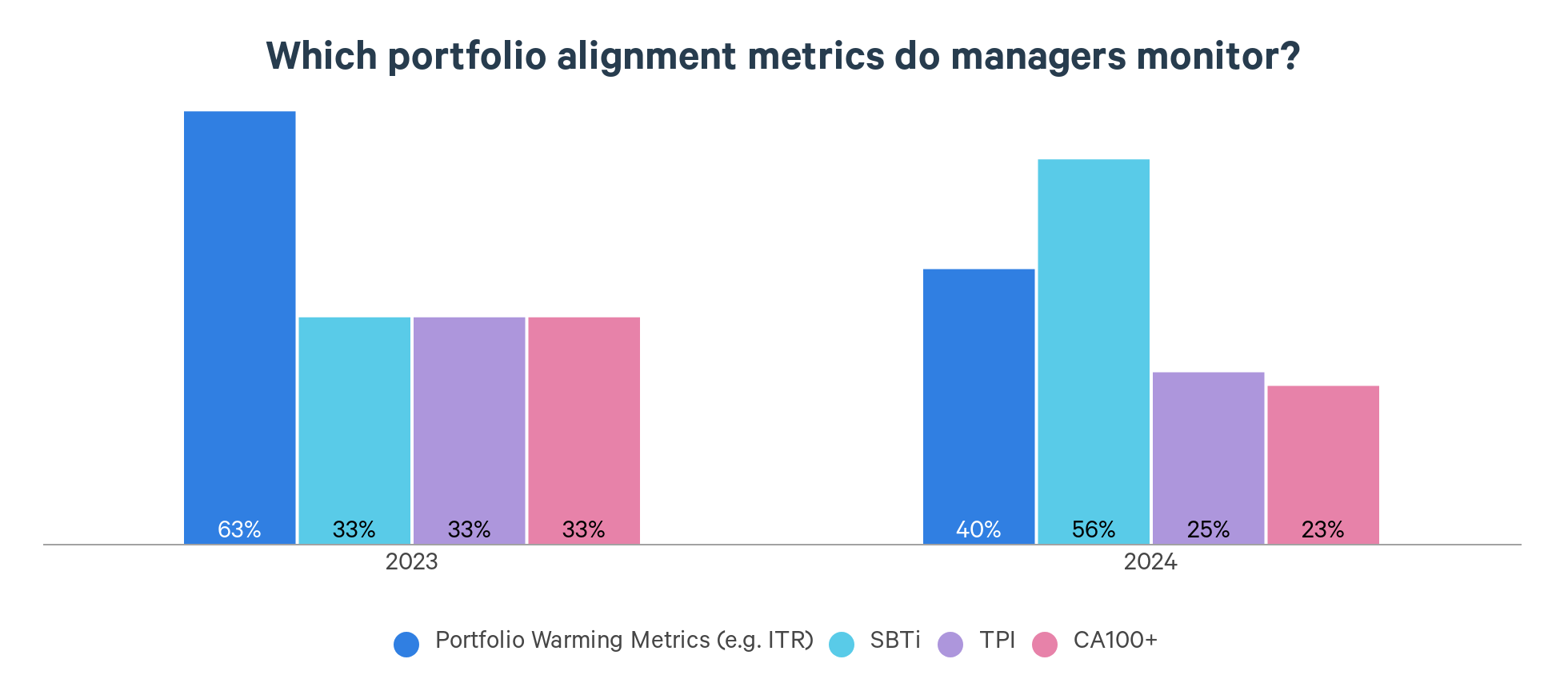

Of those managers monitoring portfolio alignment, support for portfolio warming (ITR) metrics is lower than last year, with support for SBTi increasing. This is likely driven by pension funds requesting this measure as it tends to be the preferred portfolio alignment metric for regulatory reporting.

Other portfolio alignment metrics that managers monitor are asset-class specific ones. For example, 23% of real estate managers track their portfolio against CRREM.

This percentage increases to 93% when only looking at those managers that have a strategy-level net zero target. This year-on-year increase is encouraging.