ESG INTEGRATION & STEWARDSHIP

Disclosure is no longer a differentiating factor

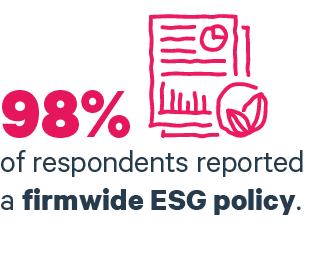

of respondents reported a firmwide ESG policy.

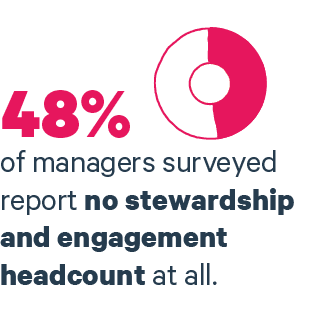

of managers surveyed report no stewardship and engagement headcount at all.

‘Firmwide’ isn’t always translating in practice, with 18% of managers’ ESG policies not covering all strategies.

“Leaving stewardship in the hands of ESG or stewardship specialists should mean greater focus and skill can be brought to bear. From what we can see, managers deploying this approach generally appear to have well-resourced specialist teams, although a gap may arise between stewardship and investment activities.”

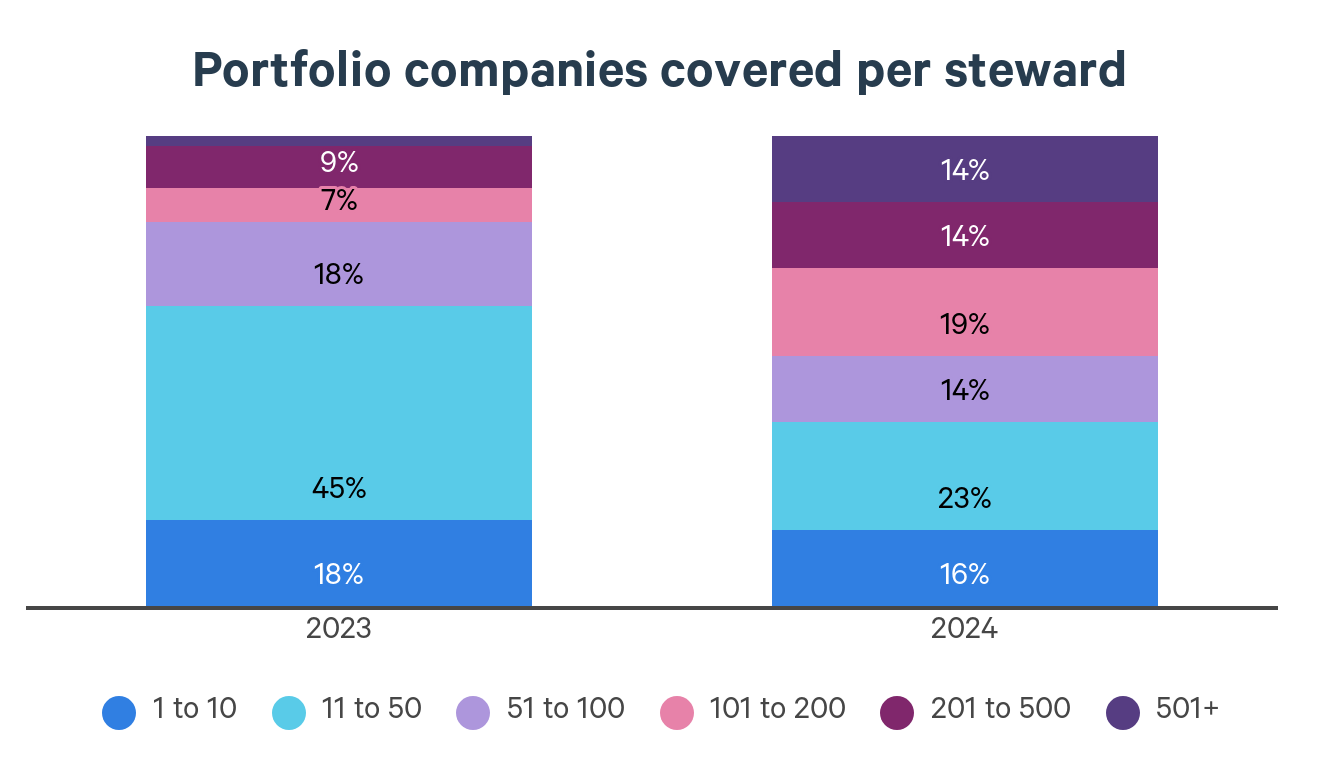

1-10

11-50

51-100

101-200

201-500

501+

Disclosure at the firm level is no longer a differentiating factor between managers on ESG. In line with 2023, 98% of respondents reported a firmwide ESG policy. For those wanting to truly set themselves apart, attention must turn to how policies drive action, and what ‘ESG Integration’ really means to them.

As shown on the right, ‘firmwide’ isn’t always translating in practice, with 18% of managers’ ESG policies not covering all strategies. One respondent even stated that their firmwide policy applies to 0% of AUM, showcasing the risk for investors in assuming disclosure is the same as application in practice.

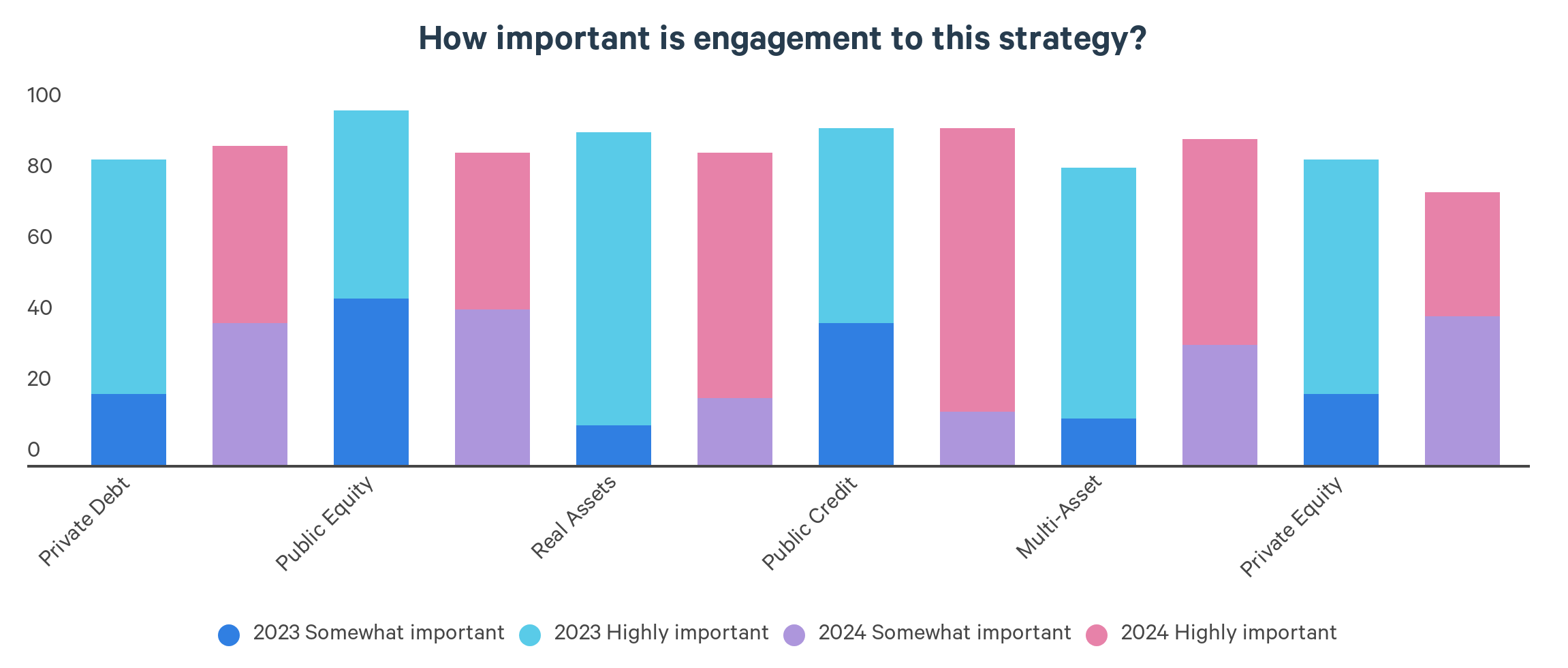

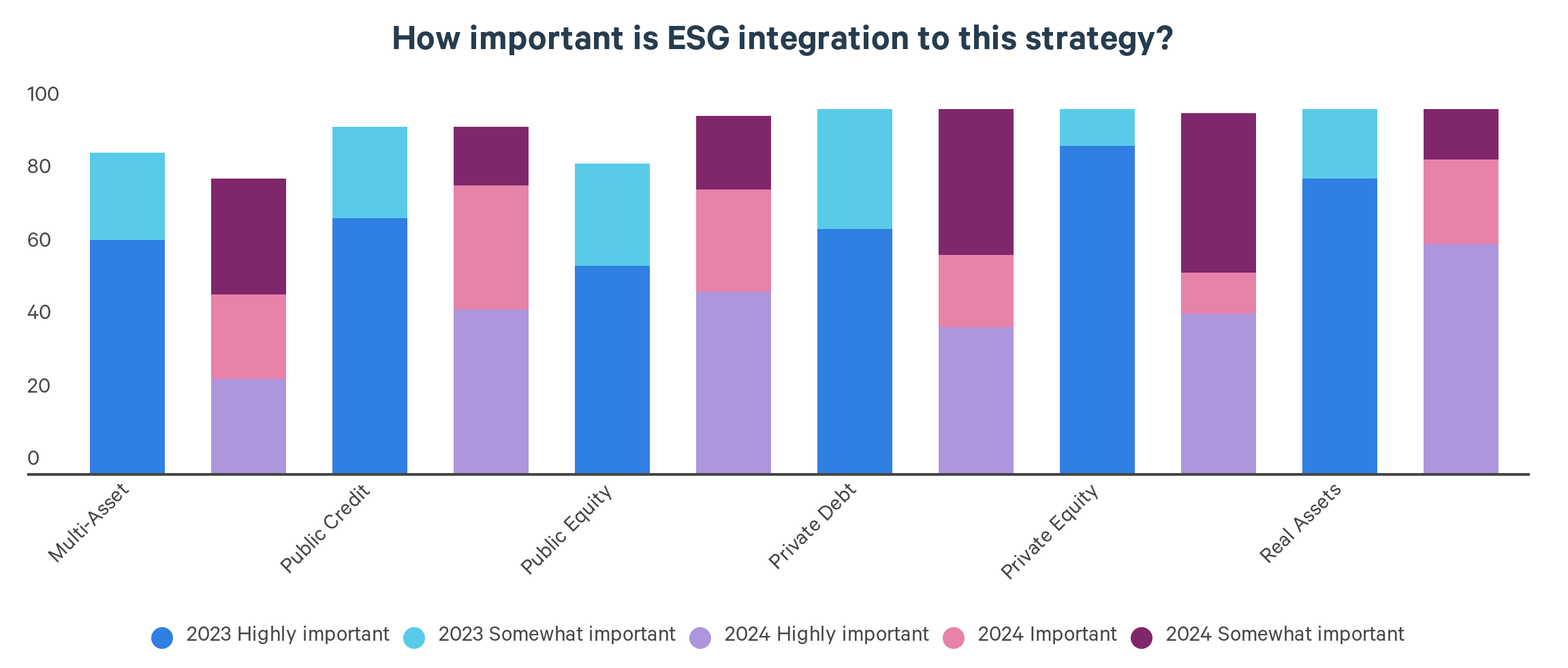

In general, managers surveyed continue to place strong importance on ESG and stewardship integration, both at the firm and strategy levels. Excluding multi-asset and LDI strategies, over 80% of managers across every asset class consider stewardship integration as ‘somewhat’ or ‘highly’ important to their strategies, and almost all consider ESG integration as at least ‘somewhat important’.

With the onset of the UK’s Sustainability Disclosure Requirements (UK SDR), we asked managers to disclose the EU Sustainable Finance Disclosure (EU SFDR) label attached to surveyed funds to give us an insight into the level of ESG and stewardship integration associated with the different labels.

The results are largely as we would expect, with the importance of both ESG integration and stewardship declining down the labels.

The number of managers with a dedicated stewardship and engagement headcount fell from 55% to 52% year-on-year. Those with a dedicated ESG/sustainable investment headcount also reduced marginally (80% to 78%).

Somewhat surprisingly, nearly half (48%) of managers surveyed report no stewardship and engagement headcount at all. This hasn’t been skewed by small firms – 70% of those without dedicated resource have 50+ employees, while 39% have 250+ employees.

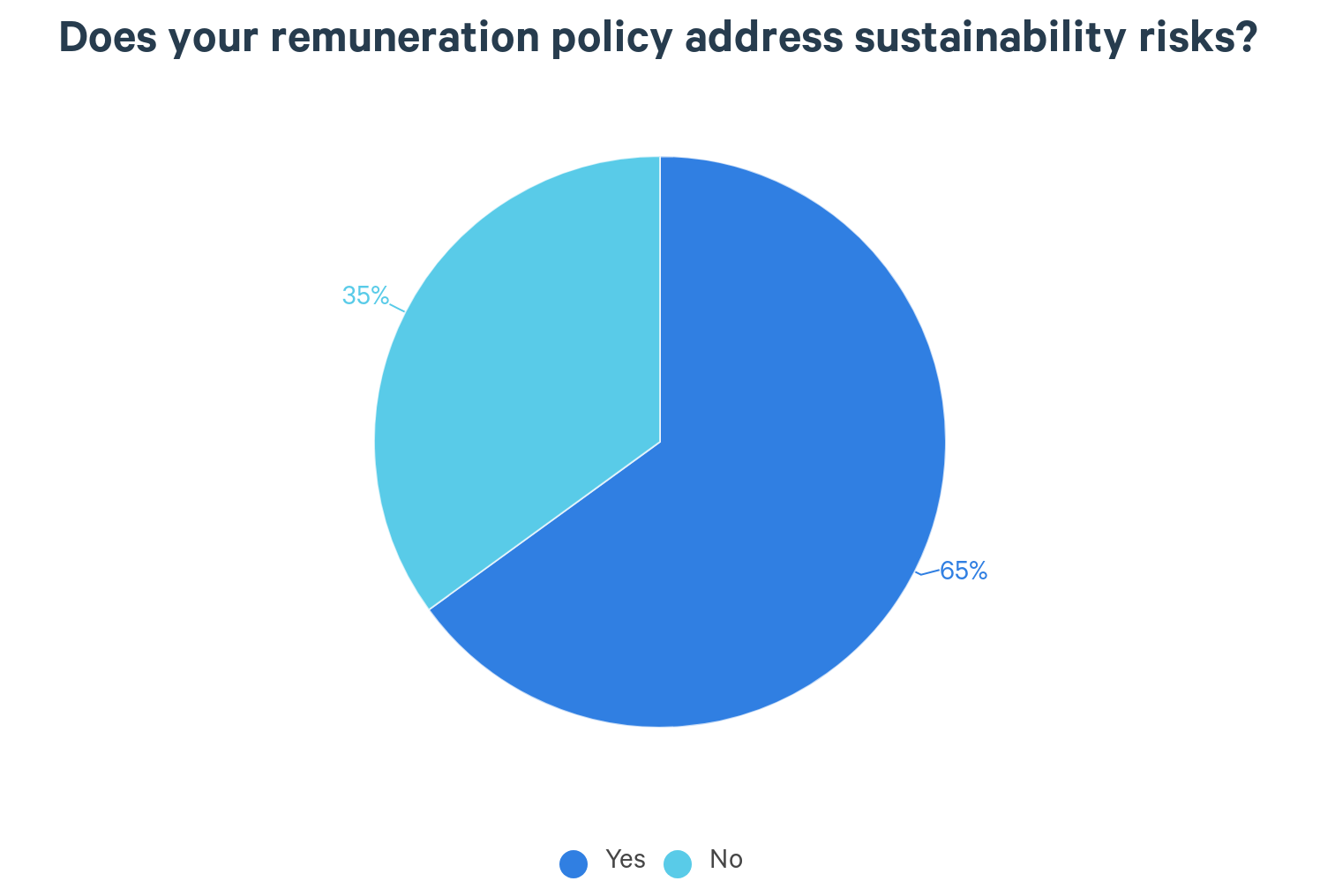

One measure of effective ESG integration is the alignment of remuneration policies with sustainability metrics. Not only do well-structured incentives cut the emphasis on short-term performance targets and encourage long-termism, they also increase the likelihood that these managers will engage with their investee companies to do the same.

The proportion of firms reporting such alignment has increased from 60% to 65% year-on-year. Interestingly, the ESG backlash in the US does not (yet) appear to be affecting these firm-level policies, with US managers accounting for a similar proportion of those not incorporating sustainability risks into remuneration as last year (56% vs 58%).

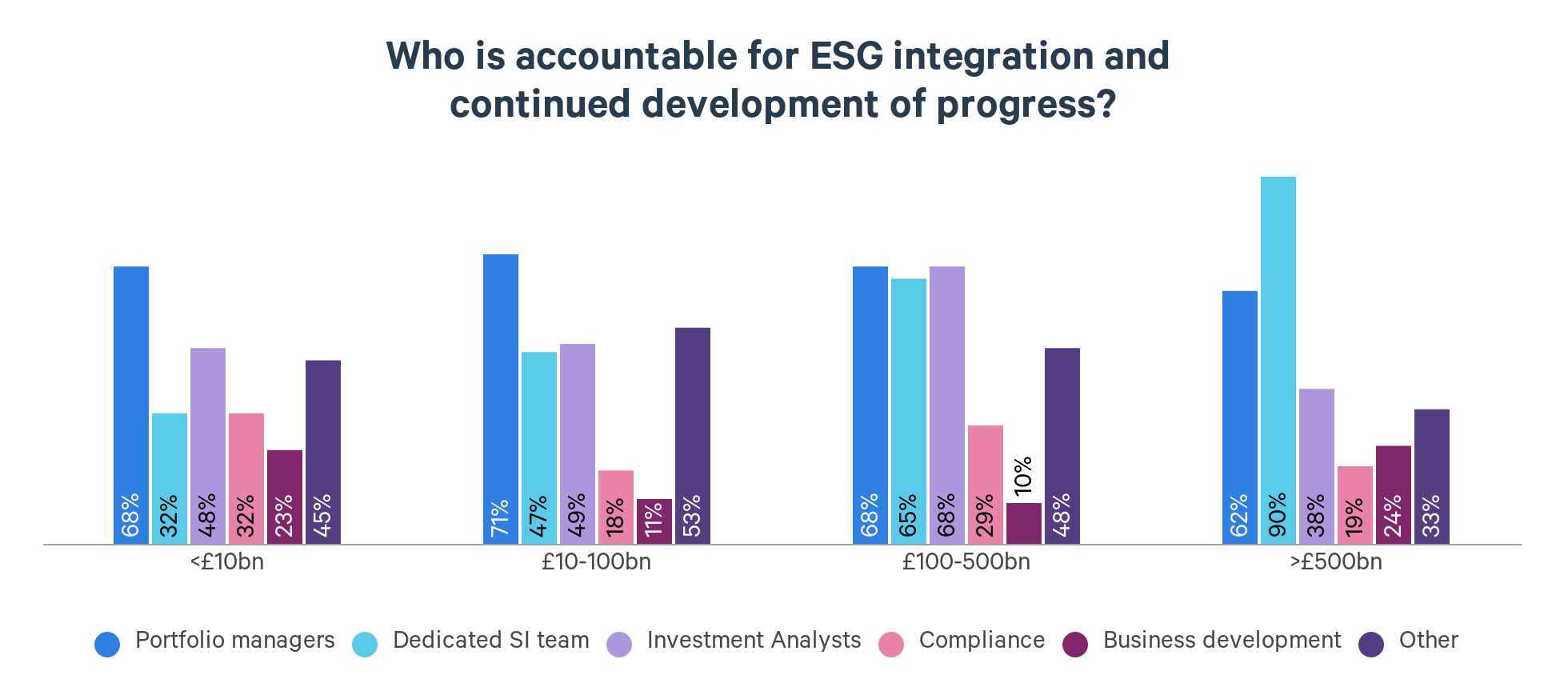

Reviewing who within a firm is accountable for the integration of ESG is a useful factor that can indicate the importance an asset manager places on sustainable investment.

Generally, the more senior the responsible individual, the more assured we can be that ESG integration is genuinely implemented. In 2023 we looked across the asset classes, where real assets and public equity were leading in terms of senior accountability.

Here, we investigate accountability in the context of the firm’s AUM.

Accountability sitting with a dedicated sustainable investment team is directly correlated with AUM size, as scale usually lends itself to greater resource.

Interestingly therefore, the accountability of the portfolio managers and investment analysts appears to decrease marginally as the AUM increases to above £500bn. A large proportion of responses (c.79%), however, referred to a shared responsibility across multiple stakeholders within the firm.

While this might appear a reasonable approach, our concern is that it reflects a lack of clearly defined ownership of ESG integration.

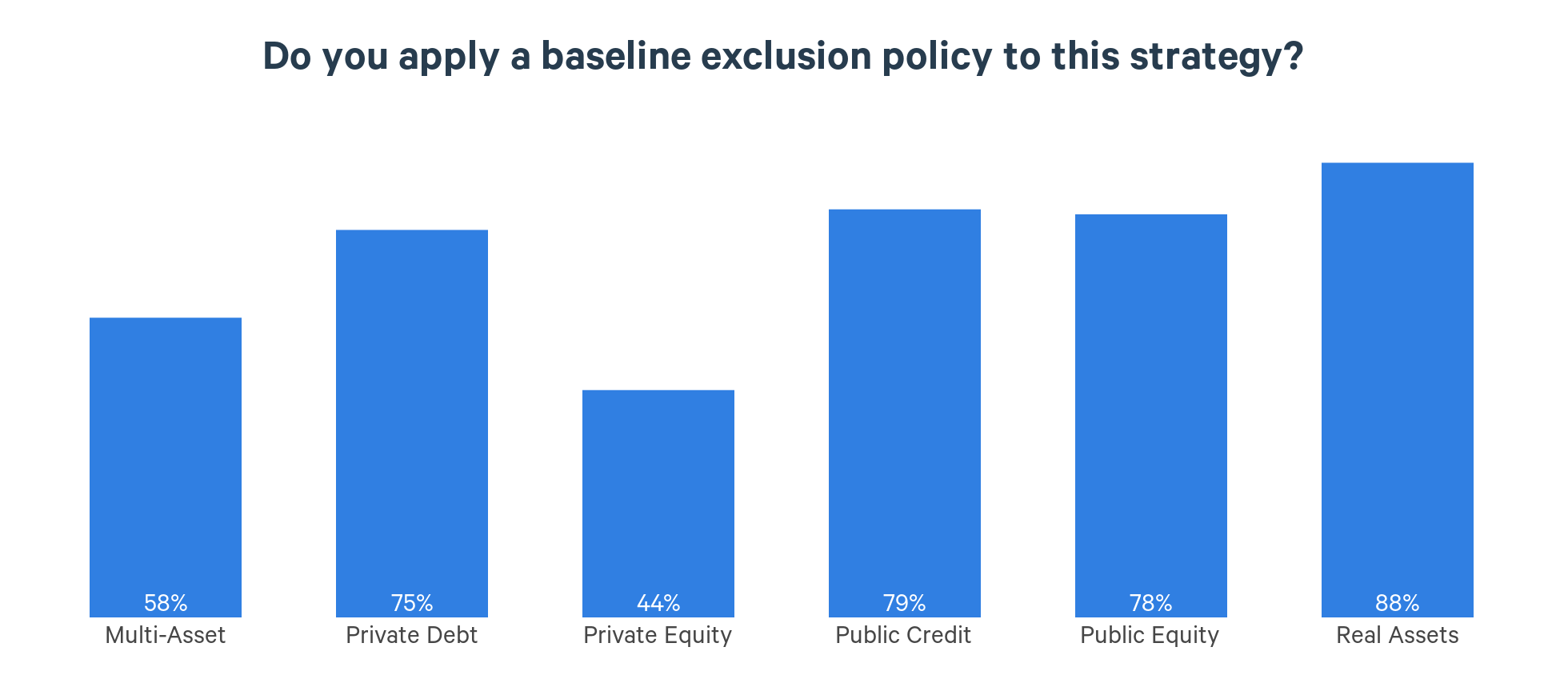

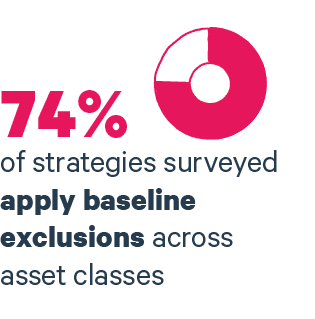

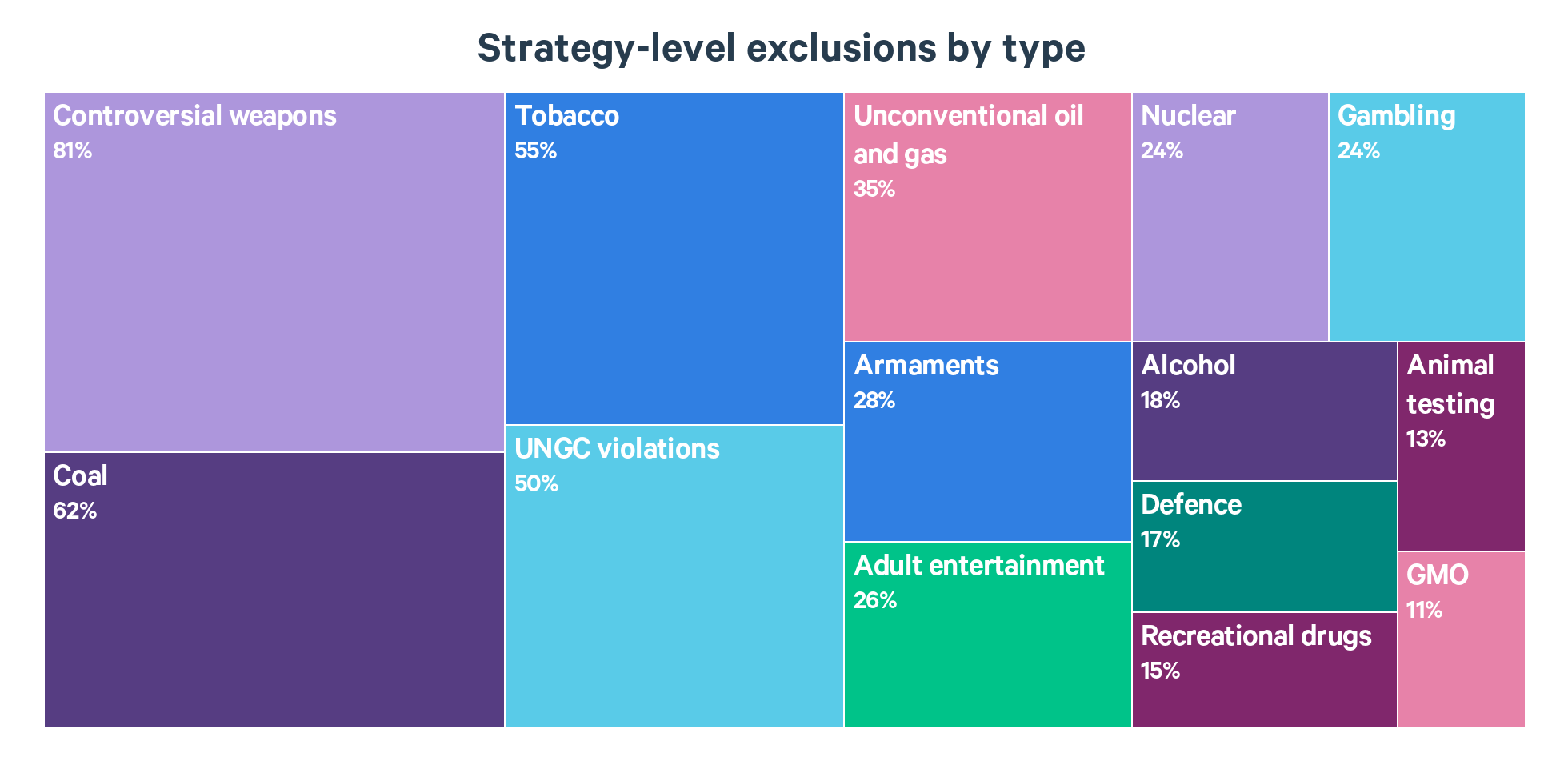

Once upon a time, exclusions were the simplest way for managers to communicate to investors that they were integrating ‘ESG’ into portfolios. The focus has since shifted towards real world impact, rather than portfolio sustainability, and this is reflected in our survey results this year. The proportion of strategies applying a baseline exclusion has decreased year-on year across all asset classes bar real assets and public equity.

The most common factors for exclusion continue to be controversial weapons, coal and tobacco. However, the proportion of strategies implementing these exclusions have fallen by 9%, 6%, and 2% respectively. Exclusions across almost all other types have also reduced.

In contrast, the proportion of exclusions reported as ‘Other’ increased year-on-year, likely reflecting more granular exclusion policies being implemented across the surveyed strategies.

A few of the more interesting excluded sectors included: unsustainable farming and fishing, private prisons, and firms without an ESG Impact Rating.

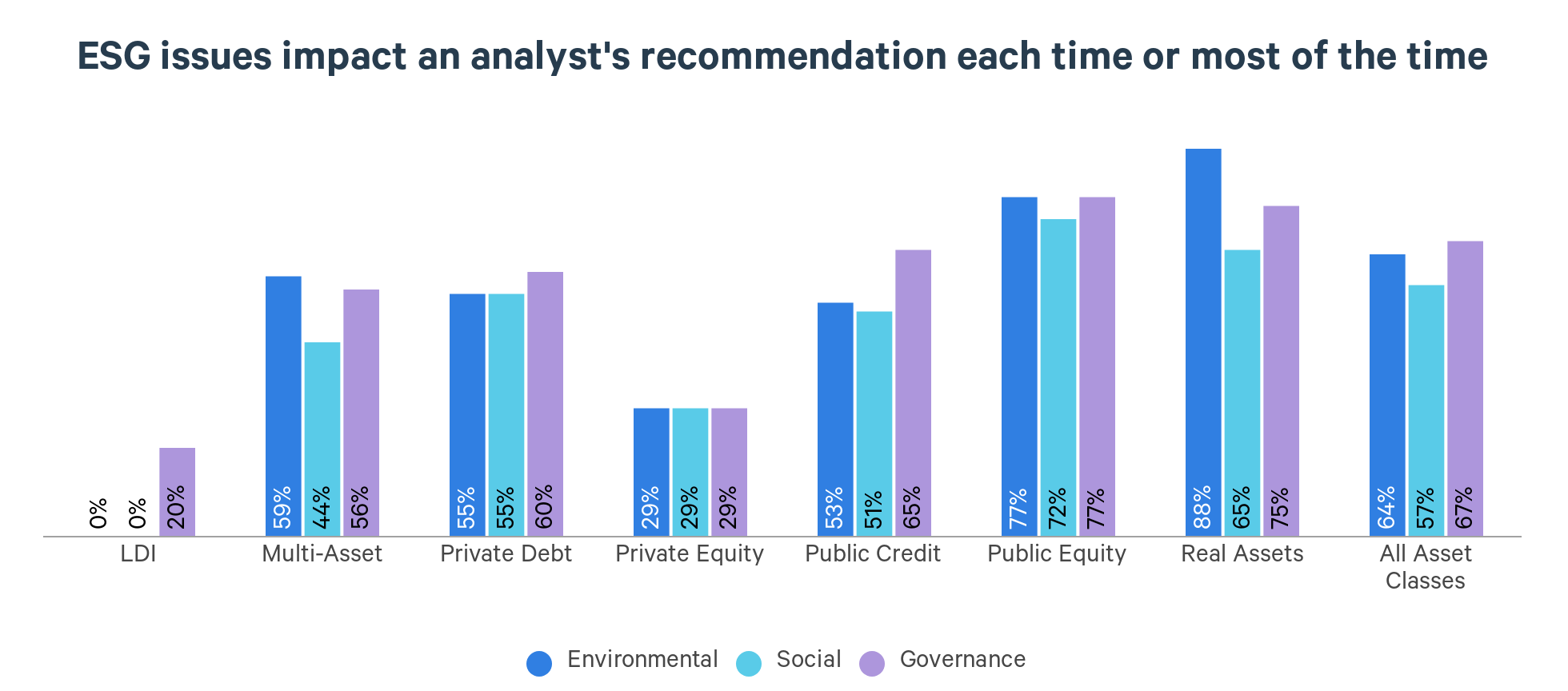

The critical point for sustainable investment is whether ESG factors really influence decision-making, rather than simply supporting existing narratives or acting as a ‘tick-box’ disclosure exercise for asset managers.

As shown in the chart, managers in real assets and public equity report a significant proportion of analyst recommendations being influenced by ESG factors.

However, across the other asset classes ESG factors only influence decision-making about half of the time, and private equity and LDI lag materially. Additionally, social factors continue to lag environmental and governance factors, impacting analyst recommendations a reported 57% of the time, compared to 64% and 67% for environment and governance, respectively.

If managers really believe engagement issues are financially material, why are they not doing more to push companies to address them?”

Good (positive): “Following an engagement with company X, where we discussed its approach to assessing biodiversity and deforestation in its loan book, we doubled our position size given our increased conviction in the company's management of a material topic for the company's long-term value.”

Good (negative): “We sold a holding of an airport operator after its temperature alignment moved above 4 degrees. There were also sales of high carbon intensity issuers in the waste and consumer sectors. We significantly reduced a holding in a pharmaceutical name due to its ESG score being low in its sector, with an F score for Ethics due to its exposure to Opioids in the US.”

We asked managers to provide examples of both where a positive ESG view had led to increased exposure and where a negative ESG view had led to decreased exposure in the last 12 months.

We received many responses stating why they could not provide an example or why the question was not applicable to that specific strategy. However, of those managers who were able to provide a case study, there was a clear lack of specificity and detail in many of the answers, casting doubt on the impact that the ‘ESG view’ did in fact have on decision-making. Generalities don’t cut it. We continue to push managers that claim they incorporate ESG to evidence how exactly ESG factors materially impact decision-making.

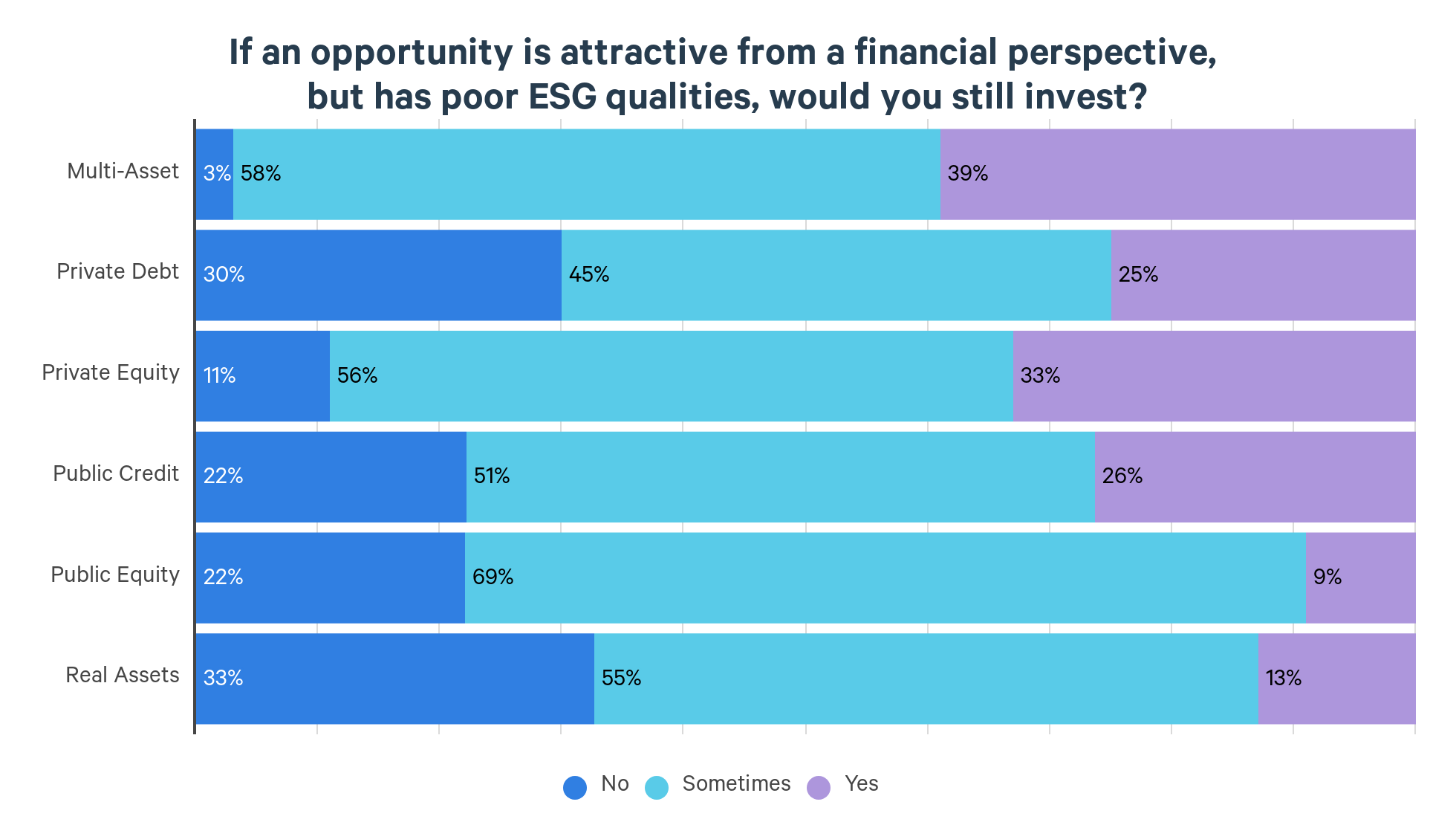

An alternative lens through which to consider the outcomes of ESG integration is the conflict that can manifest between financial and ESG analysis. We asked managers if they would make an investment in an asset with poor ESG qualities. The results were similar to last year, with managers of real assets funds seemingly the least willing to invest in assets with poor ESG characteristics.

Filtering the results by the stated SFDR labels of the strategies provides some interesting insight, with 13% of SFDR Article 8 strategies responding with a ‘Yes’. Given the shifting sustainable investment landscape towards real world impact, investing in an asset with poor ESG qualities is not necessarily negative, assuming the intention is to engage for change.

However, a vote of ‘Yes’ rather than ‘Sometimes’ may indicate a removal of the nuance required when assessing the transition potential of a company with poor ESG characteristics. We’d be surprised if these funds are able to achieve a UK SDR investment label while pursuing such a strategy.

Stewardship continues to be led by the investment team (either the portfolio manager(s), research analysts or some combination of the two) for over half (c.56%) of strategies.

For a fifth of strategies, the role is covered by more specialist ESG or stewardship professionals, with around a quarter leaning on a combination between the investment team and the ESG & stewardship function. We have seen a slight (4%) reduction in this being delegated exclusively to ESG specialists, with an increase (8%) in managers leaning on approaches with combined input from ESG specialists and investment teams.

This suggests managers may be downgrading the role of ESG specialism, placing greater emphasis instead on the roles of investment teams in the stewardship process.

The different approaches have advantages and disadvantages that need to be managed. Responsibility sitting with the investment team should enable a closer integration of stewardship with the investment approach and decision-making, but risks stewardship becoming neglected as other issues may gain priority. Most investment professionals see themselves as investors first, and stewards second at best.

Leaving it in the hands of ESG or stewardship specialists should mean greater focus and skill can be brought to bear. From what we can see, managers deploying this approach generally appear to have well-resourced specialist teams, although a gap may arise between stewardship and investment activities.

Overall, managers seem to be dedicating less resource to stewardship, with the reported number of companies engaged with per member of stewardship teams having meaningfully increased.

In 2023, only 18% of managers reported engagements with more than 100 companies per member of their stewardship function. In 2024, this number increased to 47%. For all of these managers, however, we must assume that the broader investment teams shoulder much of the burden.

In 2023, only 18% of managers reported engagements with more than 100 companies per member of their stewardship function. In 2024, this number increased to 47%."

There is apparent emphasis from many managers on the quantity of engagements as opposed to the quality. Redington is firmly of the view that quality matters much more than quantity – only quality engagements deliver the real-world outcomes that will preserve and enhance value for clients. In this sense, the data suggests we may be moving in the wrong direction.

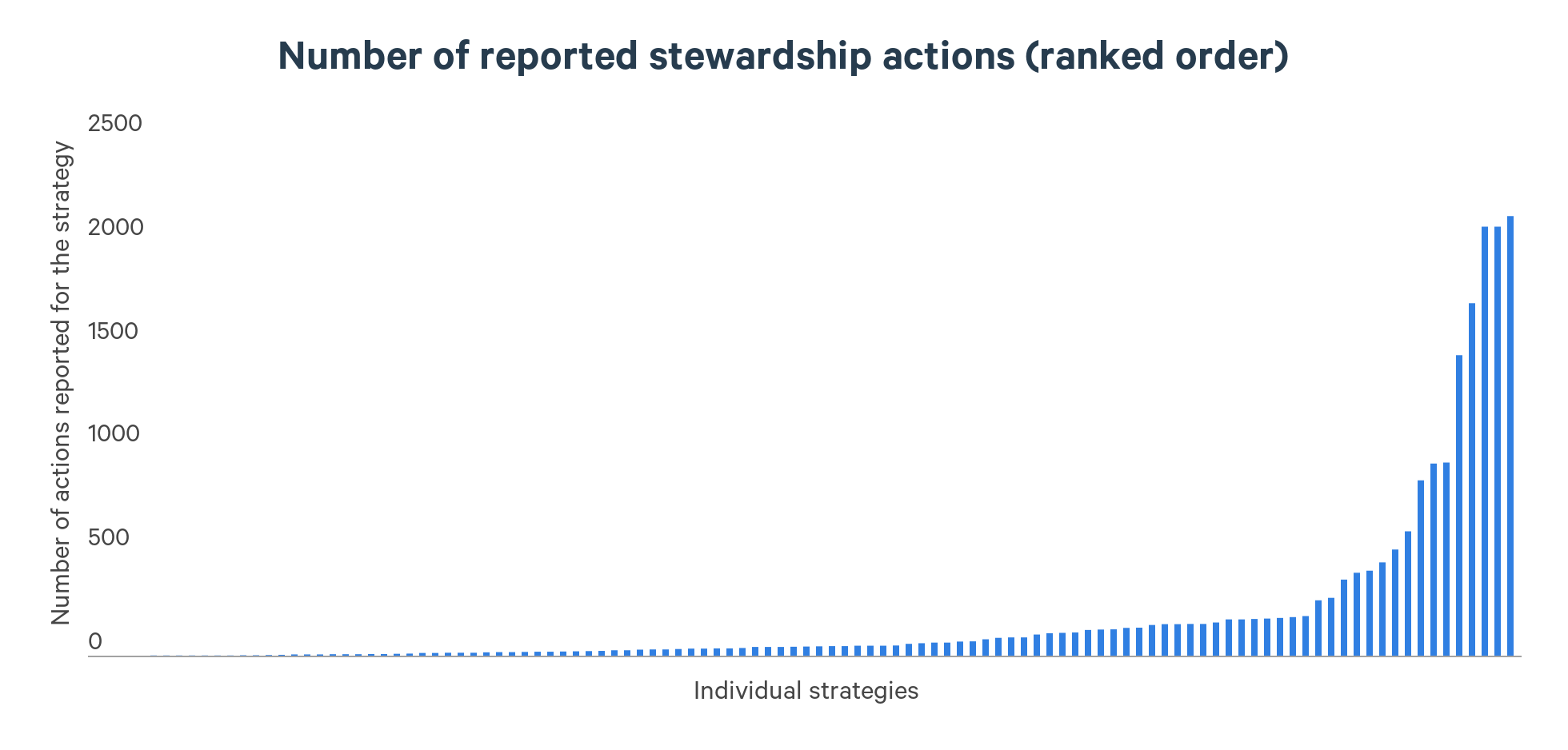

This is further supported by the data here, with multiple managers reporting engagements in the thousands for individual strategies.

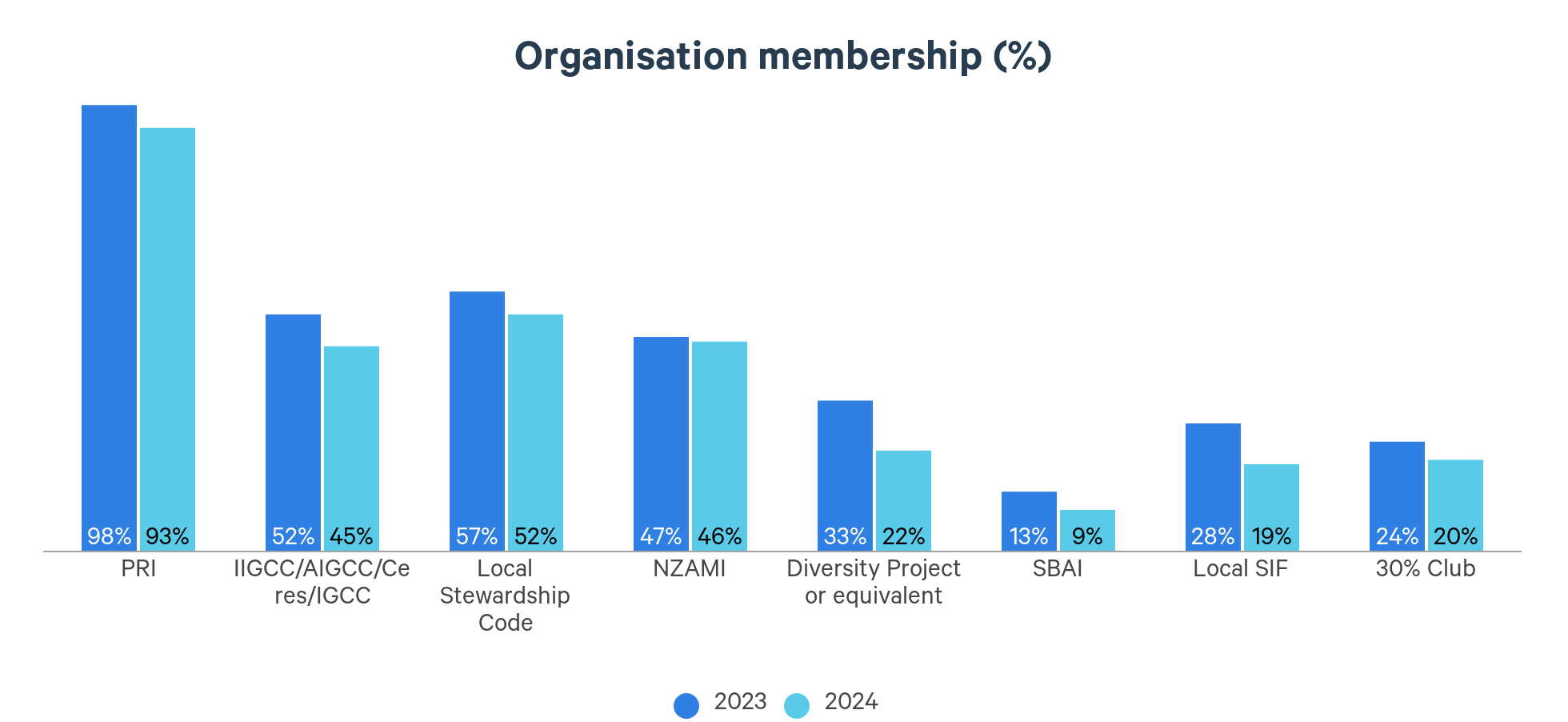

Membership of key organisations is a tried and tested means of amplifying engagement efforts, for both invested assets and throughout the investment industry as a whole.

Across all key organisations, there is evidence of a degree of reduced support from investment managers. Whilst the moves on the whole haven’t been drastic, if this trend continues it risks fragmenting approaches to stewardship and weakening the collective drive for improvement across the industry.

The highest-profile withdrawals from collaborative initiatives have of course been for Climate Action 100+, especially following political pressure in the US. The Principles for Responsible Investment (PRI) – which continues to receive high levels of support from the managers in the survey – has highlighted the potential risks that increasing anti-ESG sentiment poses to collaborative engagement in the near term. Indeed, this trend will be important to monitor as managers continue to reassess their priorities.

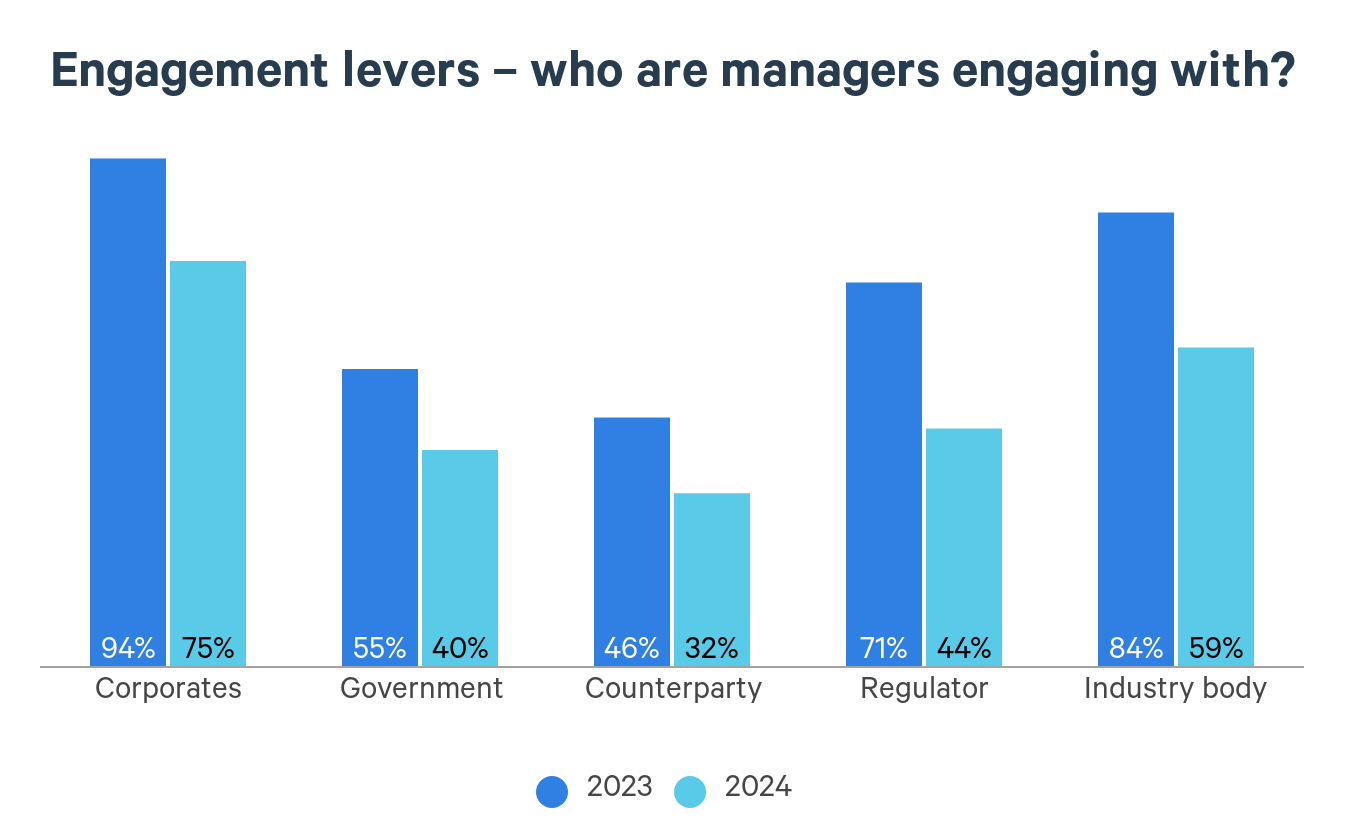

The most effective managers use every available lever for stewardship influence and engage with a variety of organisations.

Unfortunately, the data on with whom managers are engaging also suggests some retrenchment. There is a significantly lower level of engagement across all target organisations, with the falls ranging between 14% and 27% (in absolute terms).

The most significant changes have been the proportion of managers engaging with regulators (-27%) and industry bodies (-25%), a concerning shift given the systemic nature of many sustainable investment issues. This is particularly surprising given we are seeing an increasing focus from asset owner clients on systemic risks and on regulatory engagement as a key tool to seek to address them.

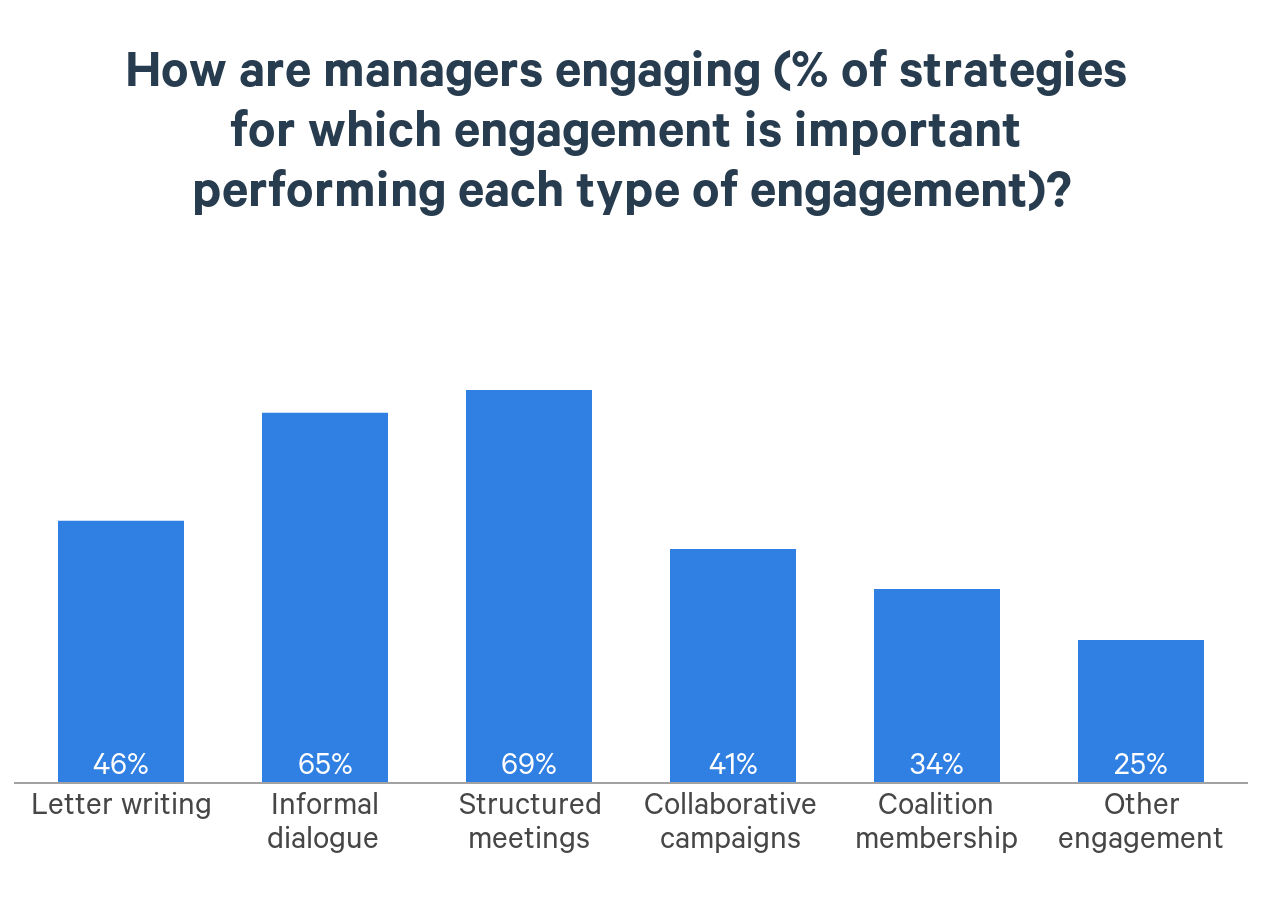

Looking at the quality of engagements that are taking place, we’re pleased to see that structured meetings are the top means of engagement managers are using.

However, only c.70% of managers who say engagement is important are engaging via meetings, while only c.40% are engaging via collaborative campaigns. A large proportion of managers who claim engagement is important for their strategies are therefore still not employing the most effective means of engagement. If managers really believe engagement issues are financially material, why are they not doing more to push companies to address them?

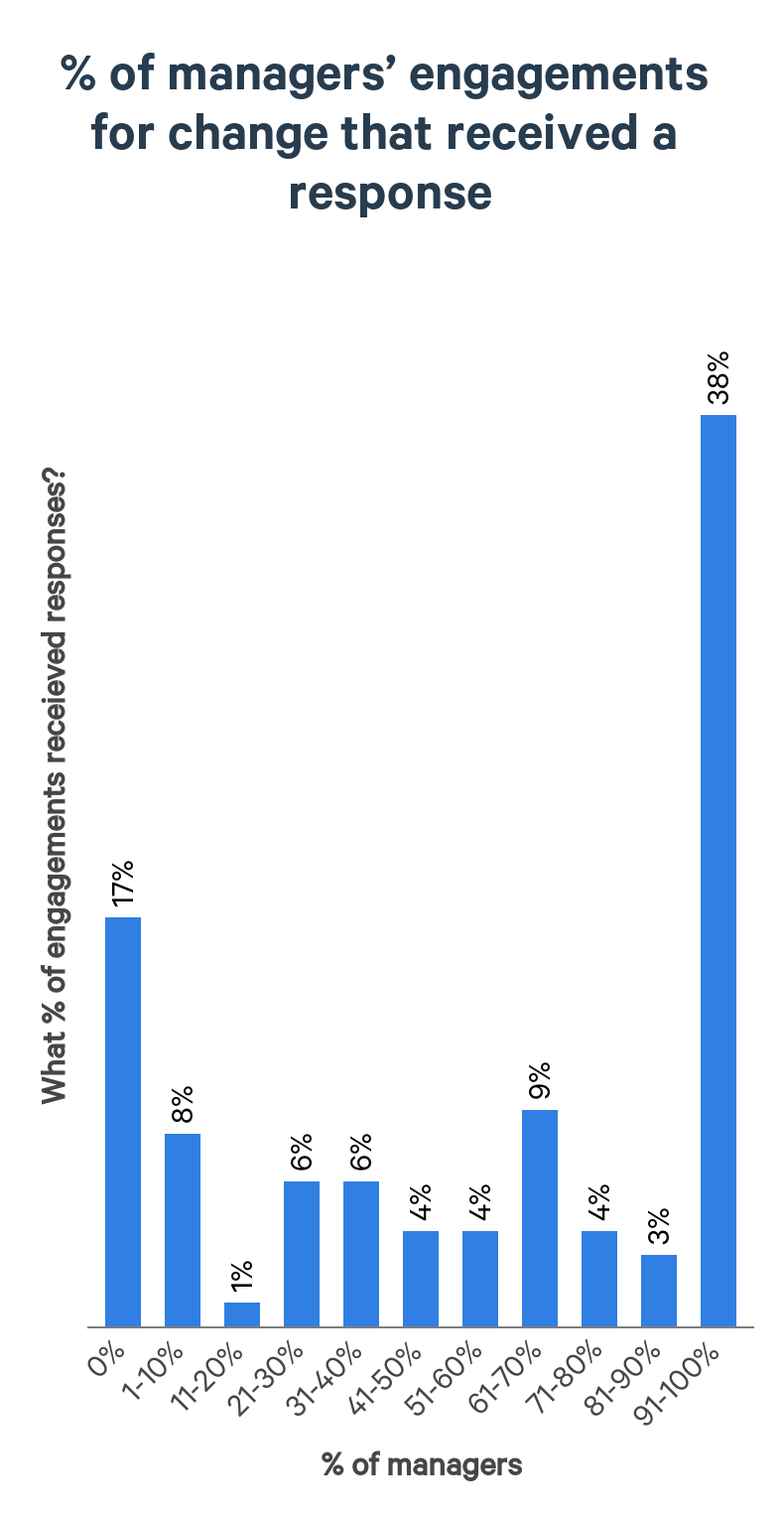

The key is in whether engagements are resulting in companies changing their approaches to address investors’ concerns. It is significant, then, that over three fifths (62%) of managers note they did not receive a response to all engagements. This compounds the notion that some managers may be focusing more on the number of engagements they carry out, rather than the quality of them.

If managers really do believe that these issues are important to the success of their investments, we would expect them to be engaging through means that cannot be ignored.

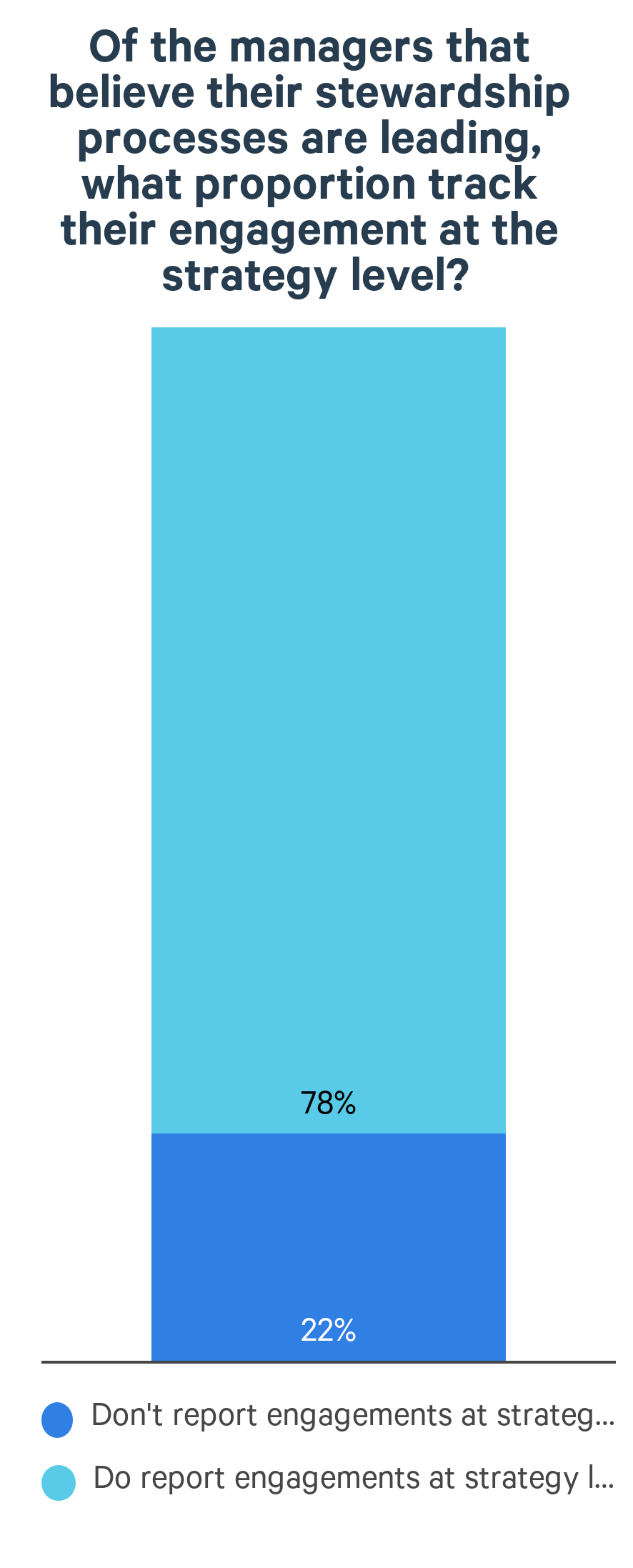

There is a notable disparity between how some managers perceive the quality of their stewardship processes and actions. Nearly a quarter of those who claim to have leading stewardship approaches do not report their engagement activities at the strategy level.

Given the availability of cost-effective technology systems to capture this data, it’s puzzling why managers, especially those who consider their approaches to be market leading, aren’t doing so.

There continue to be material gaps between how important managers say stewardship themes are and what’s happening in practice.

Managers were asked to highlight the key stewardship themes that matter for portfolios, including: climate change, human rights, board governance and effectiveness and transparency and data,

Each of the themes are said to be a focus for more than 70% of strategies (down from over 80% in 2023). However, the proportion of strategies for which managers could evidence stewardship activity on these themes ranged from only 29% (for transparency and data and business ethics) to 43% (for climate change).

Whilst the picture is more positive at the firm level, managers’ ability to demonstrate activity on the themes that they claim are important has seen a marked deterioration over the last year.

To take just one example, in 2023 92% of firms claimed that climate change was a priority, and 89% could demonstrate engagement on it. This year, 82% of firms state it is a priority, yet only 55% demonstrated engagement. This material disconnect is concerning and supports the wider theme of manager retrenchment in this space.

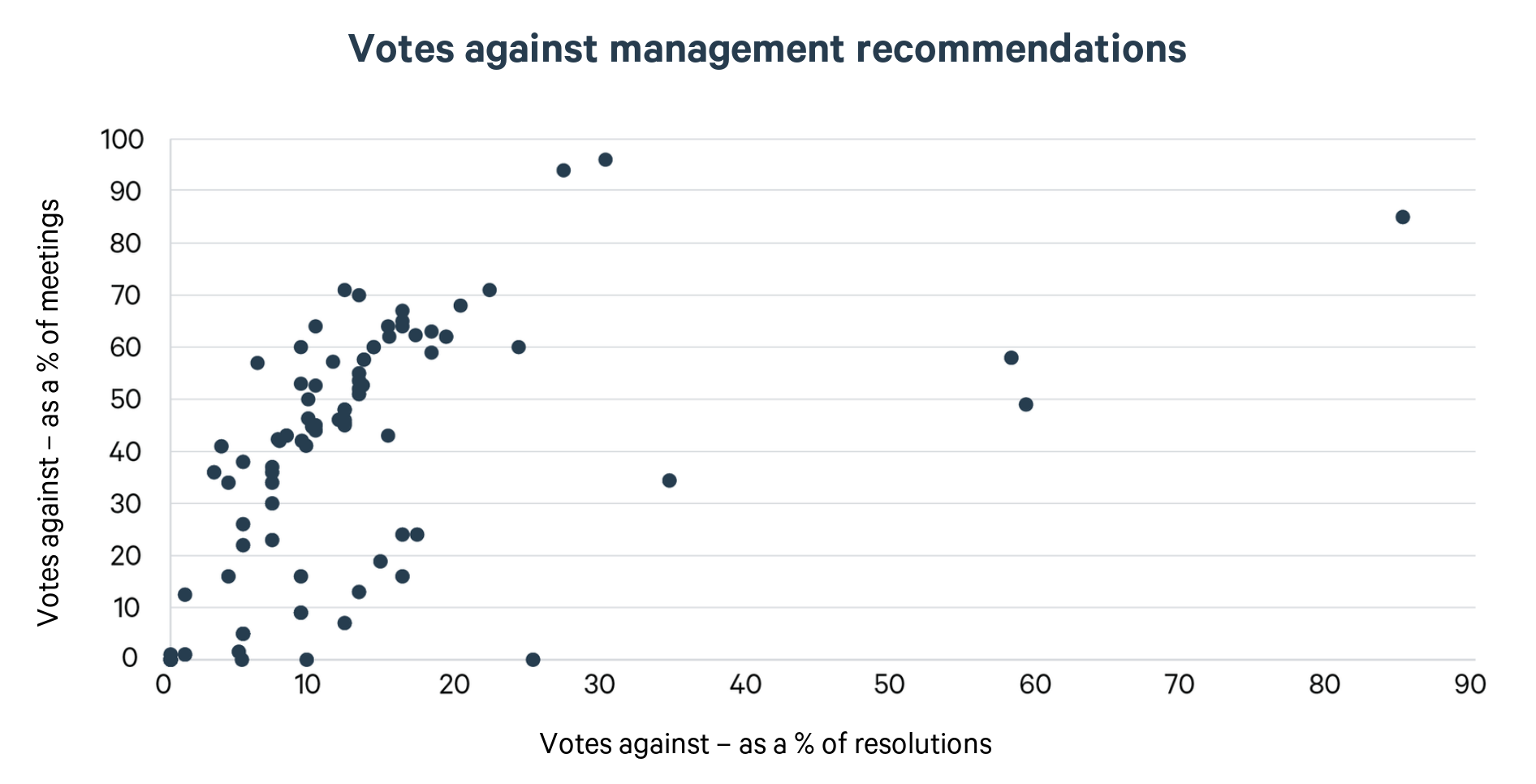

Voting matters as an indicator of good stewardship practice but only applies to equities as an asset class. Even here, the dialogue surrounding any voting decision matters more and enables the votes to be effective.

Nonetheless, capturing an overview of voting data provides insight into the mindset and approach of managers. Apart from a handful of anomalies, managers cluster along a line showing a close relationship between the number of resolutions and the number of meetings opposed. Even though surrounding dialogue and engagement matters more than the vote itself, there is a dramatic difference in approach to voting matters between those voting in support of management on almost every resolution at nearly all AGMs and the manager opposing 30% of all resolutions, including opposing at least one resolution at more than 95% of meetings.