Nick Horsfall Managing Director, Investment Consulting

Find me on LinkedIn

Drop me an email

10-second summary

Once you’ve chosen where you want to get to, and have a good idea about when and how you’re going to get there, it’s crucial you plan for obstacles along the way. As the last couple of years have shown us, things don’t always go to plan; so we can’t set an investment strategy in a vacuum. As with any long-term journey, it’s important to understand the risks involved, and how you can manage them to make your journey as smooth as possible. That’s why we help our clients anticipate and plan for key risks up front, so they’re far less likely to be hit with any nasty surprises along the way. Taking a ‘pitstop’ at the right time can make all the difference.

How do we approach risk management at Redington?

A good investment strategy not only generates returns, but also manages losses. To implement a strategy that does both, you need to be aware of the risks facing your scheme, and plan how to manage them accordingly.

So, how do you estimate risk?

There’s lots of ways of doing this. A widely used measure is Value-at-Risk (VaR), which broadly measures how much you could lose, in pound terms, in a one in 20-year downside scenario. Given the average life of a pension scheme, losses of this scale/frequency are to be expected – so you need to be confident that you can weather it. There are, of course, other measures, such as scenario analysis, which can be very instructive – particularly in relation to sustainability risks.

Pitstop 3: Risk Management Navigating bumps in the road

Once you have an idea of the risk your scheme faces, you can assess the potential impact – is it game over (and PPF-bound) or just an awkward conversation with your sponsor?

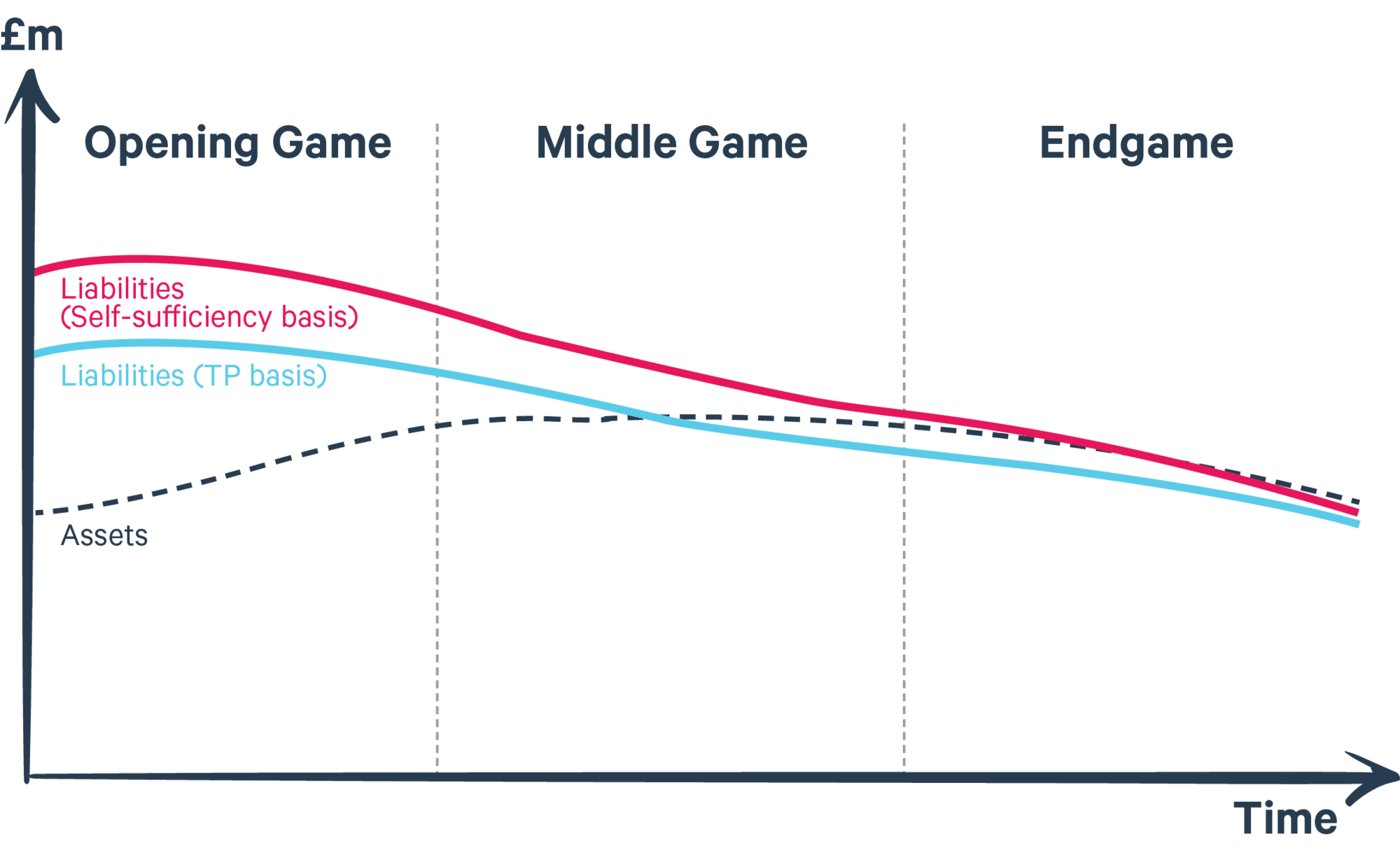

Much like everything we do at Redington, our first port of call is understanding where our clients are going and where they are on that journey. The diagram on the right sets out the typical journey of a pension scheme, split into three phases. Very few UK DB pension schemes are in the ‘Opening Game’ phase – accrual has usually ceased and there has been a detailed discussion around the Endgame. Most schemes typically fall into the Middle or early Endgame phases, and it’s at this point that the real benefits of risk management can be felt.

Once our clients have chosen a suitable risk measure (or multiple), we help them set a risk budget (i.e. the amount they can reasonably afford to lose, based on factors such as the strength of their sponsor covenant, whilst still remaining on track to meeting their objectives). This information is incorporated within their PRMF to ensure that all strategic decisions are guided by the client’s risk tolerance.

A typical pension scheme journey

How do you plan for and manage risk?

In our view, the most thorough approach is to look at the breakdown of risks that your scheme faces over the coming years. Typically, these will be:

You can observe the relative sizes of these risks (see chart on the right) and take a view if any one (or more) is likely to steer you off course. You can also look at the development of these risks over time, together with possible changes to the visibility of your sponsor’s covenant. The latter being helpful in checking whether the expected timeframe of your journey is sensible – is there merit in increasing risk now to reduce the time you’re dependent on your sponsor, or vice versa?

You can also take a view as to why you’re exposing your scheme to unrewarded risks, if the cost of removing them is acceptable. You can even look to reshuffle risks to be proportionately greater or smaller if this would be more efficient.

This type analysis can lead to a range of outcomes, for example:

How does this benefit our clients?

Good risk management is done in advance. It’s inevitable that a pension scheme will run into risks during its lifetime, so relying on luck isn’t an option – especially when member benefits are at stake. This is why we help our clients to understand the risks their schemes face, the impacts on their journey plan if those risks were to materialise and how they can be managed in a robust, disciplined and appropriate manner. This gives our clients confidence that they won’t be faced with any unmanageable bumps along the way.

Redington showed a refreshing approach to risk management and was able to establish a clear path towards full funding on a buyout-type measure.