Karen Heaven Managing Director, Investment Consulting

Find me on LinkedIn

Drop me an email

10-second summary

As with any long journey, it's essential to agree on your destination and intended route before setting out. And, to ensure you reach your end goal as smoothly as possible, it's also important to pull over every once in a while to refuel, check your tyre pressure and look at traffic updates. The same goes for managing a pension scheme, so we’ve designed a bespoke decision-making framework to help our clients do just that.

How do we approach goals & objectives at Redington?

Our philosophy at Redington is to ‘begin with the end in mind’. When we begin working with a new client, we first get together with key stakeholders (typically the trustees, investment committee and sponsor) to understand their investment beliefs.

We use these beliefs to articulate a clear set of investment objectives and constraints – including a funding objective, risk budget, ESG targets and other limitations such as fees, liquidity, governance bandwidth, etc.

Pitstop 1: Goals & Objectives Agreeing your destination

Over the last 10 years, Redington has engrained a solid risk management and governance framework for the Plan which has made the key strategic decisions easier, avoided potential pitfalls and ultimately helped the Trustees produce a stable funding improvement over time. As a full buyout has become closer, the Plan’s framework has been adapted to allow us to be opportunistic in the market and respond in particular to the changing insurer pricing for buy-in/out transactions. Now the portfolio is in good shape for a transfer to an insurer, but also in a good place to continue running on should a transaction not occur. We enjoy the collaborative approach that Redington encourage through all of our advisors in our goal to secure member benefits.

Once these objectives and constraints are agreed, they remain key to guiding ongoing investment decision-making – they’re not just written down in a SIP or reviewed once in a blue moon.

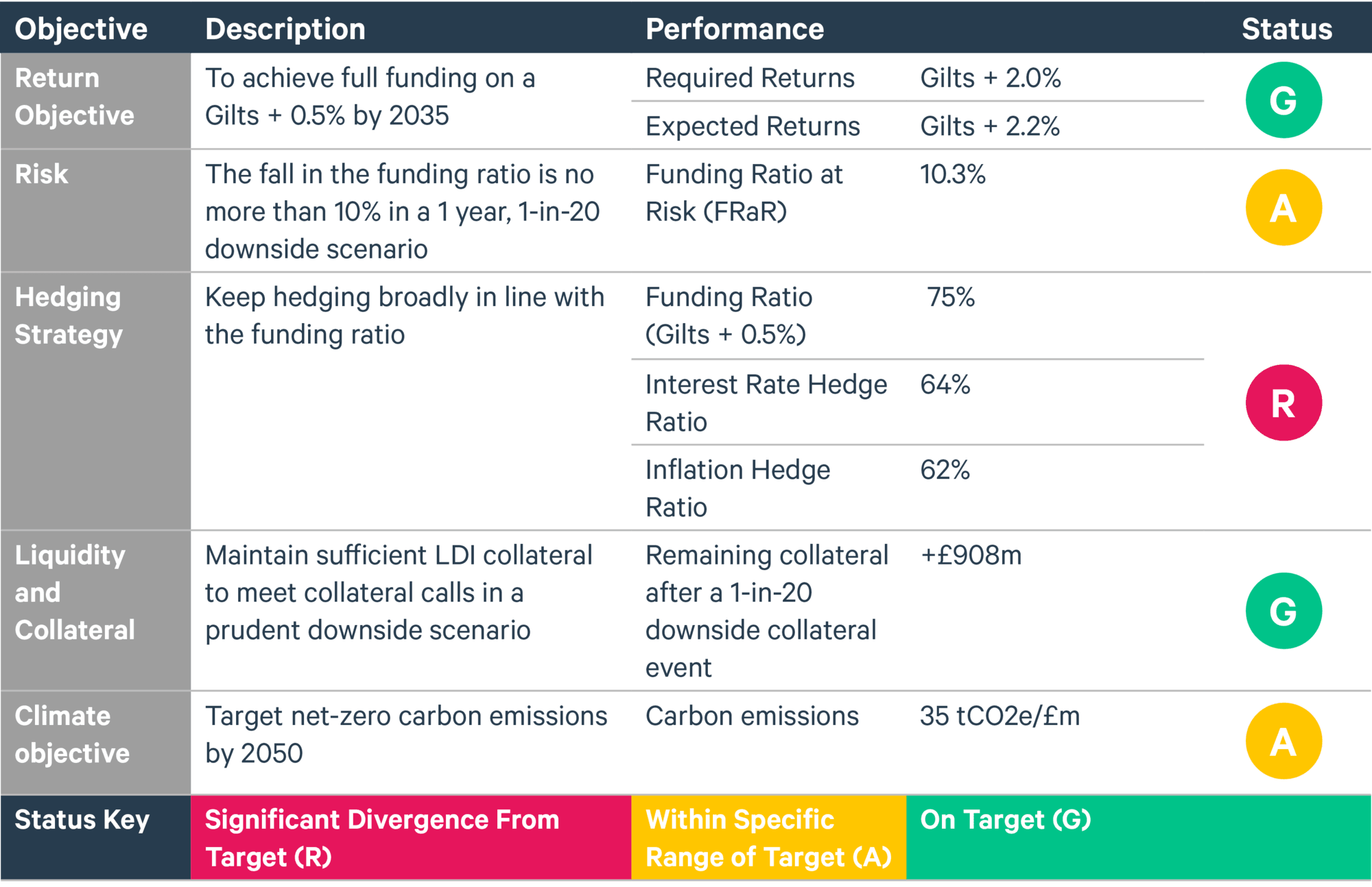

We developed our Pension Risk Management Framework (PRMF) to help achieve this. It’s a simple, one-page dashboard that sets out a pension scheme’s key objectives and constraints.

A PRMF looks a bit like this – it holds all the information you need, without the detail you don’t.

The PRMF forms the basis of all our advice. It’s reviewed at every meeting – i.e. at least once a quarter – to monitor progress and identify whether a scheme is still on track. When a scheme goes off track (highlighted by a red or amber traffic light), it flags a clear call to action. Such actions might include increasing the expected return, recalibrating the hedge or allocating to renewable infrastructure to help meet the scheme’s climate objective.

Some investment decisions might seem inconsequential, but they can soon throw a scheme off track if taken without the endgame in mind; this can result in the need to take fundamental (and sometimes costly) corrective action. Taking investment decisions based on their alignment with meeting the scheme’s ultimate objectives, and monitoring progress against these objectives regularly, reduces the chances of this happening.

How does this benefit our clients?

Agreeing objectives and constraints up front helps to ensure stakeholder alignment from the get-go. This means that stakeholders know where the scheme's headed, what’s needed to get there and how big the risks are. It also helps to cultivate a collaborative and long-term focused working relationship among stakeholders and advisors.

We’re very proud of the funding level performance of our DB pension scheme clients and believe that their success is down to the use of our PRMF, which provides a clear and focused decision-making framework.