Are you keeping a close enough eye on your DFM?

By Redington's Fiduciary Oversight team

There is a great deal of trust when an individual hands over their wealth to an adviser to manage for them. Part of your role as a wealth manager is to select the best third parties to manage certain aspects of the investment strategy. In some cases, it’s appropriate to delegate the investment management of the whole portfolio to a fund of fund or Discretionary Fund Manager (DFM).

When you place your trust in a fund manager on behalf of your clients, you want to be certain they’re acting in their best interests. So how can you make sure they are?

This is a fundamental question of transparency and good governance and – we believe – the business of good investment management.

Institutional investors have been outsourcing investment management to fund of fund managers for decades. Some have learnt the hard way that these are not “set and forget” decisions. Whether it’s a pension fund outsourcing to a “fiduciary manager” or an endowment outsourcing to an “outsourced CIO”, it has become clear that close monitoring and assessment is necessary to ensure trust is well placed on behalf of the underlying beneficiaries.

The market turmoil caused by the LDI crisis revealed drastic dispersion in outcomes between those OCIOs that had high-quality risk management and governance structures versus those that did not. It is critical to find this out before extreme market events unfold through proactivity of assessment and oversight.

With the onset of Consumer Duty, advisers have had to review the appropriateness and suitability of products and services to ensure that everything they have in place is supporting clients’ best interests and not causing foreseeable harm.

But are external providers being incorporated into this review process? And are DFMs being subjected to the same degree of scrutiny as the advisers' own practices?

We believe they should be, on both points. Going further: under Consumer Duty, we believe that there is now an even great onus on the wealth managers to assess and demonstrate how the investment providers that they select are delivering against client objectives, both at the outset and on an ongoing basis.

Asking the right questionsOutsourcing portfolio management does not absolve you of the responsibility of ensuring that investment decisions are made in the best interests of the individual underlying client. However, the wealth businesses that appoint DFMs often do so in order to focus their time and resources on clients. In these situations, simple frameworks and guidelines to assess the DFMs are valuable – perhaps essential.

Asking the right questions sits at the heart of our due diligence process as we undertake research, advise on fund of fund manager appointments, and measure ongoing manager performance.

Key areas we look to cover include how a DFM provider tailors their products to suit each client’s needs, how they provide value for money, and the degree to which they are independent.

If you disaggregate asset allocation from implementation, or fund selection, you can begin to see two different competencies, with different skillsets and different success criteria.

An example here is two different wealth management businesses outsourcing their investment management to the same DFM business. In many instances, the two client cohorts will end up in the same suite of risk-rated portfolios. That might be acceptable if the objective of those two client cohorts is identical in terms of their investment objectives and risk profiling methodology. If they are not, it may not be appropriate for these two groups to be given identical exposures.

Ultimately, you need to know if your provider can cater to your individual bank of clients and if they’ve got the range of funds and investment solutions to support their needs.

Understanding the blind spotsIt isn’t possible to remove all ‘blind spots’ in investing, but there are questions we can ask and data we can analyse to give us the best possible lens on the road around us.

When combating blind spots, one key consideration is familiarity bias. If you’ve had a provider in place for multiple years, how confident are you that they continue to be best in class for your clients?

The industry develops quickly as technology, data and other factors improve, so even if your provider was the best option five years ago, you want to be confident they have kept pace with these improvements. Above all else, you want to be certain that you’re getting optimal value.

Another consideration is investment philosophy. This again links back to ensuring that providers take a holistic approach to client needs and objectives, with value for money front and centre.

For example, a 5% asset allocation to alternatives may well be delivering exactly the right risk and return a client needs. However, if that is implemented via five different funds, you would need to ask questions like, are all these line items contributing sufficiently to justify the added complexity? Would greater economies of scale and commercial leverage be achieved with a larger allocation to a smaller number of funds?

On the subject of risk, it is also important to be sure that your provider is fully cognisant of the risk contributors within a portfolio – and, indeed, that their risk assessments match up with reality.

As an adviser or wealth manager, holding your providers to account on these issues – and doing so consistently through a regular review process – is essential to ensure your clients’ best interests are being met.

For advice firms, particularly those at the smaller end of the spectrum, outsourcing to a DFM may well be seen as a necessary step – and if that is indeed the right path for them to follow, then there are several fantastic providers in the marketplace.

Nevertheless, these guardians of capital must be monitored closely. Whether through your own provider review processes or in conjunction with external support, it’s essential to ensure that the experts entrusted with your clients’ money are making the most effective decisions to deliver on your clients’ desired end game.

If you’d like to hear more about how Redington can help your firm to hold providers to account, please don’t hesitate to get in touch.

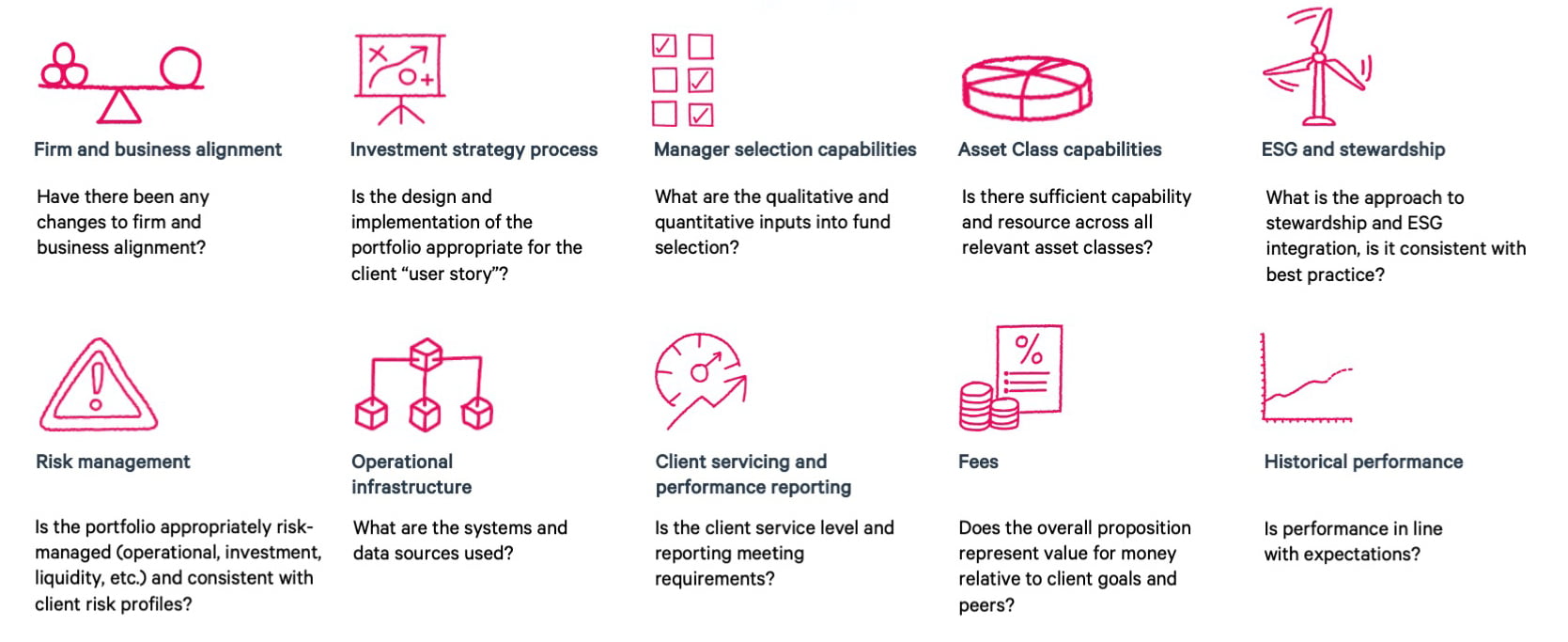

The Redington 10-factor assessment framework that is used to review DFM providers, with example questions.