Should drawdown portfolios be constructed differently?

Arash NasriSenior Vice President,Global Assets

Find me on LinkedIn

This is a question that we are frequently asked as investment consultants advising a range of wealth managers and financial advice businesses. With a growing base of clients approaching decumulation, firms must consider how to advise those using their accumulated wealth as a source of retirement income.

While the key conundrum here relates to risk appetite, we think the answer to this question is “yes”. Yes, decumulation portfolios should be constructed differently. The reasons why are many, though sometimes nuanced.

When giving investment advice, it is important to always start by understanding our clients’ objectives and risk tolerance levels. This risk profiling process often consists of a questionnaire and qualitative conversations around tolerance and attitudes to risk, the measure of which is very often volatility. This risk profile is then used to inform a portfolio designed to maximise the expected return whilst remaining within the agreed risk budget.

Now, that is a simplified summary of the process, but the key point is this: during the accumulation stage, the set of risks applicable and the trade-off with returns are relatively straightforward, the general rule of thumb being: higher risk tolerance = more equities = higher expected return.

However, for an individual in retirement and “decumulating” their assets, it’s a fundamentally different situation from someone in the asset accumulation phase of life. The set of risks applicable to an individual, and an individual’s investment, are not only different and more complex to deal with, but they often evolve over time. Different methodologies for managing these risks must be incorporated into the portfolio construction process.

New risksLongevity, shortfall and sequencing risk become crucial factors in decumulation. Affordability of income drawn from a portfolio must be balanced with the desire to enjoy the money that has been saved. The risk of running out of money becomes absolutely critical in the design of a portfolio which is being relied upon for meeting expenditure.

Some of these considerations fall within the remit of financial planning, whilst others lie within portfolio construction and investment management. Indeed, some components straddle both the financial planning aspect as well as the portfolio management process.

For financial planning reasons, it is sometimes advised to allocate a proportion of the portfolio that is to be drawn upon to cash. The idea being that this pot of cash is used in the event of a market downturn. This helps to prevent realising losses by encashing assets at lower valuations. Encashing for income during periods of market weakness can have an outsized impact on the portfolio's longevity and has been termed ‘pound-cost-ravaging'. It is effectively the opposite of the better-known phrase, ‘pound-cost-averaging' – one of the bedrocks of financial planning.

However, the benefit of holding this cash pot to dip into must be balanced with the cash drag experienced, which will be diluting returns along the way.

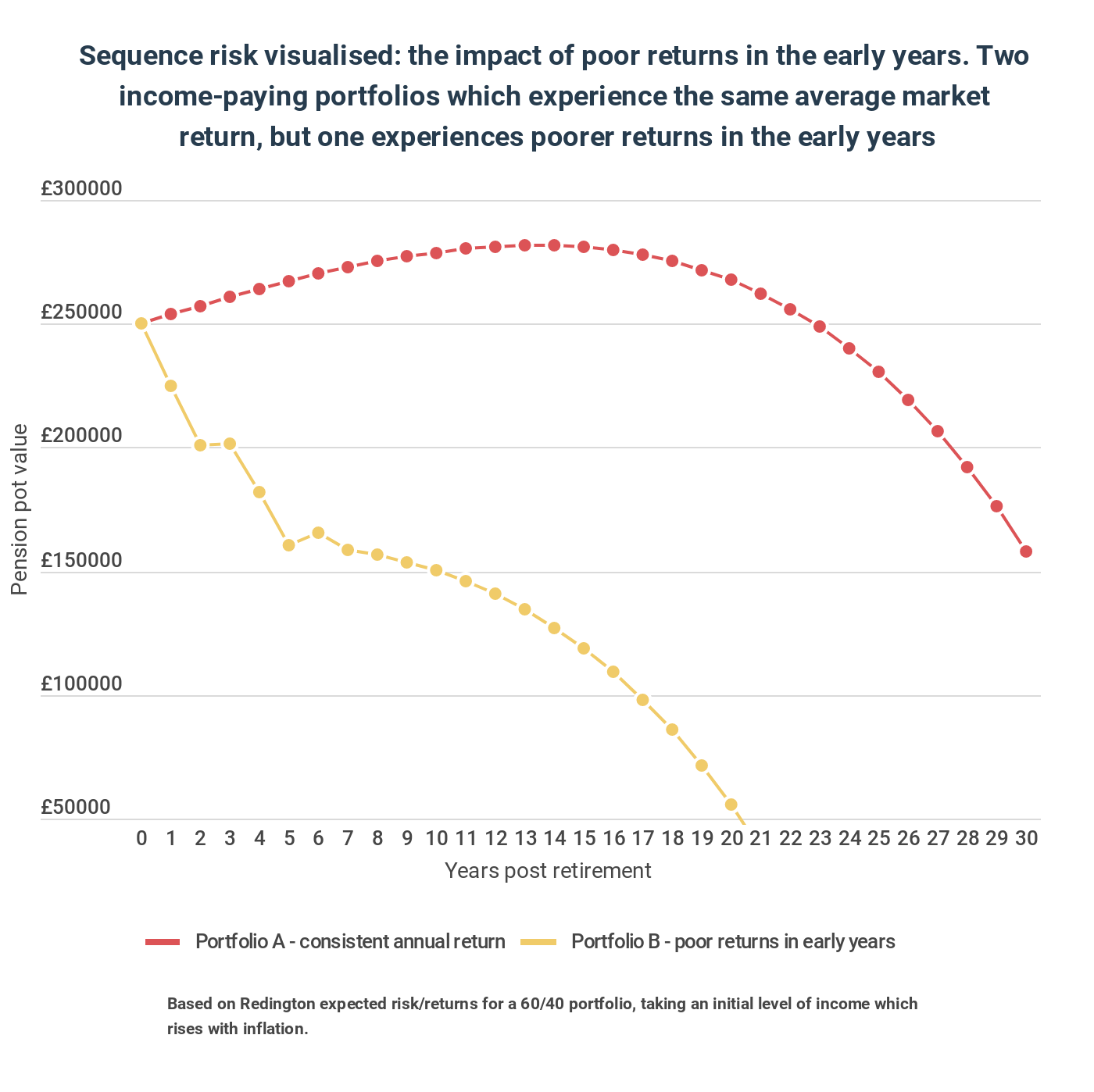

This brings us to sequencing risk – the risk that withdrawals are taken at a “bad time”, which means after a downturn in the early years of decumulation. Sequencing risk can be managed through financial planning, for example by allowing for scope to reduce withdrawals in periods of market stress (more on that later). It can also be managed through portfolio construction by reducing the probability of experiencing large drawdowns. This means reducing the weight to higher volatility assets – less equity, more fixed income – and increasing the weight to genuine diversifiers that protect the portfolio when markets sell off – more alternatives, less traditional assets. This helps to steady the path of returns and reduce the likelihood of these “bad times”.

And finally, longevity risk – the risk you outlive your assets. We see this as a risk best managed through effective financial planning. Lifestyle factors, income requirements and income preferences need to be discussed – as these are often very subjective – alongside sensible expectations of long-term market returns. From a portfolio construction perspective, the priority is to provide a broad range of investment options with clear articulation of the expectations (return and risk) from each portfolio. The adviser can then tailor the journey to the individual, factoring in other solutions, such as insurance products, where appropriate.

How much income can I take?This is one of the most important questions for individuals in decumulation, yet one of the most difficult to answer.

The first principle to getting the most from your portfolio in decumulation is to adopt a “total return” approach. Ultimately, the portfolio returns must be viewed as a whole, and it doesn’t matter whether it’s from capital gains or income. A simplistic view of taking drawdown income is to withdraw the natural income or yield from a pot without touching the capital. This may work well if you have a sufficiently large pot and if you wish to pass on the capital value to a beneficiary. However, it works less well for more modest pots, where income alone may not be sufficient for the required standard of living, as well as situations where the priority is to provide for retirement, with any inheritance or legacy being a nice-to-have.

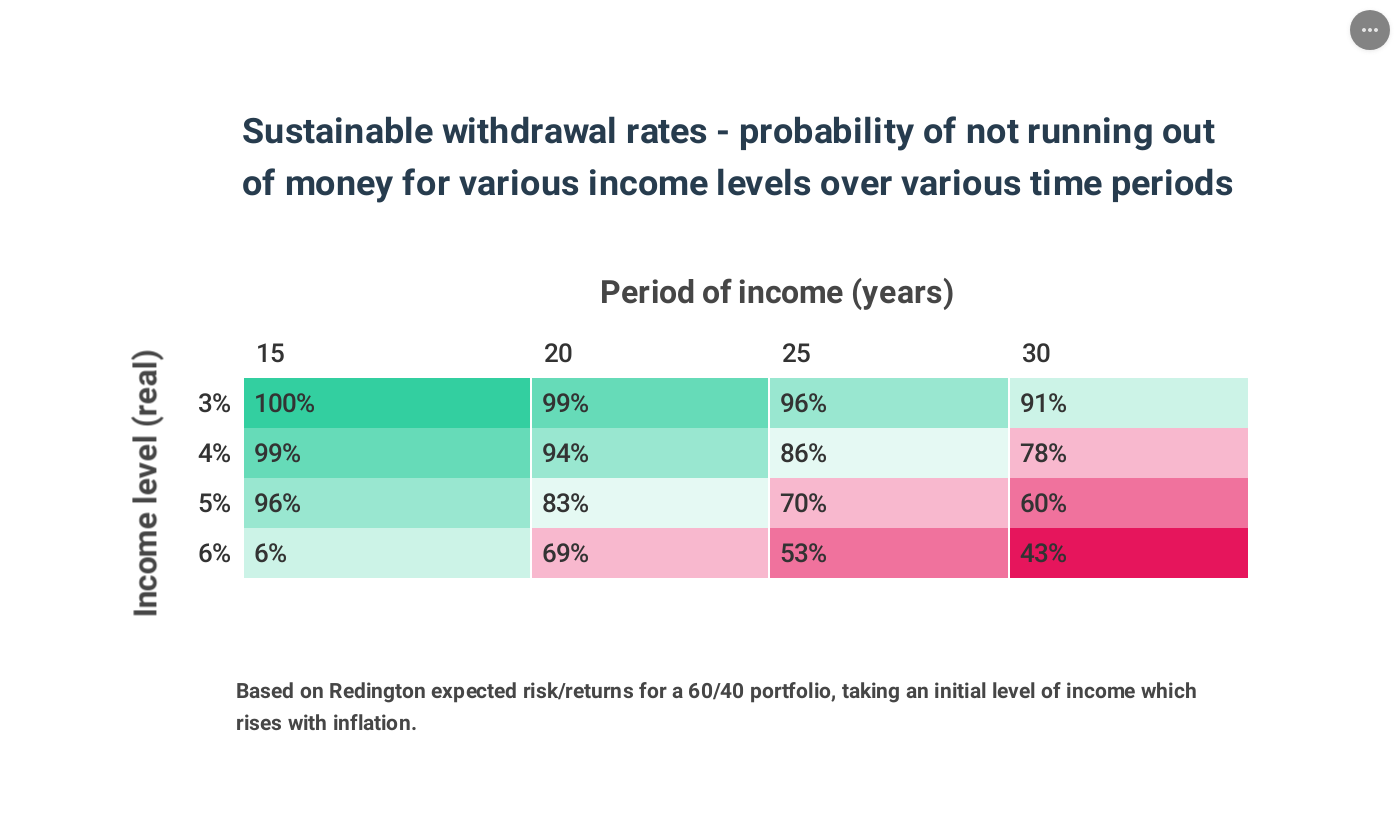

That being said, working out how much to take is easier said than done and requires deep thought and planning. The table to the right gives an indication of the likelihood of not running out of money for different income withdrawals over different time horizons.

In addition to more sophisticated investment strategies, the “probabilities of success” in this table can be enhanced through varying the levels of income withdrawn following poor returns (as mentioned earlier). Here we can learn from the world of endowment investors, as many of them adopt so called “spending rules” – such as the Yale Rule – to link the level of spending each year to the value of the assets. This means that they can spend more when returns are strong, but when capital values are lower the spending is restricted. Even a modest change in income can have a meaningful impact.

Though many may have forgotten that they exist over the last 15 years with rates so low, we must also now remember that annuities are a more attractive option for clients whose only focus is to receive a known amount for the duration of their lives. Indeed, there are likely to be scenarios in which it is sensible for some clients to purchase a degree of fixed income and then take a degree of market risk with the remainder, which includes the benefit of being inheritable.

So, the answer is obvious, right?There are multiple levers which can be pulled to help improve outcomes for individuals in decumulation. Pulling these to different degrees impacts the overall probability of clients successfully achieving their objectives.

There are different philosophies and approaches when it comes to positioning clients and their investment portfolios for the decumulation phase.

Some wealth advisers see it as a financial planning piece, where the decision around asset exposures and withdrawals is largely derived from the client cash flow analysis part of the advice process.

Others see the retirement situation as being part of the portfolio construction process, whereby the make-up of the portfolio is fundamentally different in order to provide for the balance of required expenditure, downside protection, capital growth and legacy.

At Redington, we have experience of constructing decumulation portfolio sets collaboratively with wealth management firms, considering their client types, philosophies, and constraining factors, and we’d be happy to chat more.