Pain versus potential

Laura BampfyldeDirector, WealthFind me on LinkedIn

This article was originallyfeatured in IFA Magazine.

On my commute to work this morning I saw the floors of Waterloo station being cleaned by some kind of robotic mop. I watched it for a minute, impressed to see innovation where I’d least expect it. That was until I saw a member of staff standing nearby supervising the robotic mop…

Incremental improvement or a re-imagining?This got me thinking about the discussions surrounding digital innovation in wealth management. It’s widely acknowledged that the technology used by financial advice businesses and discretionary fund managers (‘DFMs’) is ripe for disruption, but that’s been the case for some time now, and we’re yet to see much action.

There are multiple processes throughout the course of giving financial advice, from client fact-finding and risk assessment to portfolio construction and fund selection, execution and subsequent oversight. Some areas have had more attention than others when it comes to technological overhaul. When it comes to innovation, we typically see two approaches:

Option 1: Identifying areas in the ecosystem that are painful and time-consuming (and therefore costly) and digitally replicating them.

Option 2: Working backwards from the outcome of the process and re-imagining the route to get there.

Option 1 is the most common, with varying levels of impact. The robotic mop I saw in the train station is a perfect example of a business digitising part of its process but not adapting other processes around it. As a result, the business hasn’t saved any time or money and it’s failed to make improvements to the customer experience; the floor is clean either way, but they’ve spent a lot of money on equipment and are still paying a supervisor to watch it. At the other end of the spectrum, we’ve worked with advice firms effectively digitising parts of the fund due diligence process to automate high-touch areas, improve their audit trail and re-deploy staff to higher-value work.

So, what’s putting people off Option 2?

The pain of changeLast year I wrote about the NextWealth research findings that the most common place to store investment decisions is in the minutes of the Investment Committee meetings. Indeed, many DFMs have been known to run their investment proposition through a combination of Microsoft Excel and Word. When I explained to a colleague that this is very much the norm, he said, “Isn’t it painful?”.

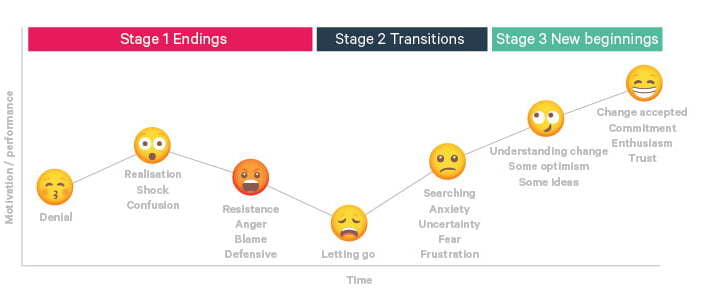

Intuitively, it makes no sense to manage something so important in such a manual way. But then again, I’m a creature of habit. I book the same seat in the office, I use the same mug for my morning coffee and I like to know where my files are saved so I can quickly find what I need. As shown by the Kubler-Ross Change Curve (helpfully illustrated with emojis below), deviating from your day-to-day working methods can be painful.

Source: www.t-three.com/thinking-space/blog/why-change-fails

The trouble is, Option 1 still requires change. It still disrupts the teams who can find files from saved shortcuts and muscle memory. In the NextWealth report, one firm said of their investment process: “Decisions are tracked in Microsoft, Excel, Word, Teams, and OneNote. We are in the early stages of developing a database based in SharePoint”. I’d argue this is the financial services version of the supervised robotic mop.

New beginnings Stage 3 of the Kubler-Ross Change Curve is ‘new beginnings’, where change has been accepted with commitment and enthusiasm. We can’t pretend that implementing new technology into existing processes isn’t going to be hard, but this quote in the NextWealth research exemplifies why change is worth the initial teething issues: “Keeping pace with client expectations and industry expectations is our biggest challenge. We have to invest a lot more in technology than perhaps what wealth managers have done historically…We have 170-200 portfolios. That would not have been possible without technology and our small team.”

Whether you begin by finding incremental ways to improve your business, or you’re all in on Option 2 – re-imagining the process – remember that the potential at the end of the change curve is worth the commitment. And, as the saying goes, “If you stand still, there is only one way to go, and that's backwards”.

At Ada Fintech, we’ve worked with a range of wealth management businesses to improve their fund research and portfolio management processes, enhancing cross-team engagement and governance and demonstrating Consumer Duty standards. Overcoming the inertia of the technological status quo and embracing a digital transformation could be the key to unlocking better outcomes for clients – and to the longevity and resilience of the industry itself. Please get in touch if you’d like to hear more.