Five key questions to ask

Tara GillespieHead of Global Assets

Find me on LinkedIn

For all the books and courses there are on presenting and pitching, isn't it strange we don't get taught to listen?

Listening isn't just about translating the vibrations in your tympanic membrane and ossicles bones into nerve transitions to your auditory cortex.

It's about attention, focus and understanding. It's about picking up the non-verbal cues. It's about withholding judgement whilst you gather the facts. One of the fundamental tenants of a successful relationship is listening.

For a wealth manager, the most important relationship you have is with your clients. No question. Speaking to wealth managers, it is obvious how much energy is invested in nurturing those relationships with time, informative content and compassion. Listening seems to come naturally.

People have a surprising tendency to share deeply personal non-financial issues with their wealth manager because they trust them. But the strength of that trust hangs precariously on the investment outcomes you deliver for them.

This brings us to the importance of the relationship with the investment decision-makers. In recent years there have been sizeable changes to the governance around investment decision-making, spurred by asset consolidation. The outcome of this is converging around two governance models.

The first is acquisition-fuelled larger capital pools held by internal teams within a central investment proposition. The other is partial or full delegation of the investment function to a third-party discretionary fund manager (DFM).

There are a lot of benefits to delegation of investment management, particularly for smaller firms. However, it's critical to select your DFM with care and diligence and closely monitor them. As already highlighted, when you are in the business of investment, the relationship with your client is inextricably linked to the capabilities of your investment manager or DFM.

I often hear phrases such as ‘performance last year was good’ or ‘the CIO is excellent’ as proof statements in support of said chosen DFM. Although these may well be true, I can't help but worry about what bubbles under the surface of these superficial statements.

So, back to the question in hand, how well do you really know your DFM?

To truly understand your DFM and how they are going to deliver for your clients going forward you must pay a lot of attention. You must analyse the non-verbal cues. You must withhold judgement whilst you gather the facts. In short, you must really listen.

Here are five questions we would suggest you ask yourself to understand whether you have really listened to your DFM and, equally as important, whether they have really listened to you:

Rarely do clients ask to outperform ARC or IA sector over five years. If an iteration of that is the only ‘objective’ statement it could suggest a lack of genuine understanding. In the current Consumer Duty climate this needs proper attention.

All eyes are on value for money these days. This isn’t just about fees, there are lots of factors feeding into the value debate. These should be appropriately defined and monitored. You can make that easy through the use of frameworks, data and tech.

It isn't just about historical performance. This is no guarantee of future returns, as we know, but we also don't have crystal balls. There are 10 factors that need to be assessed when considering the future potential for delivering good outcomes, outlined later.

To mitigate the risk of historical returns being random, it's important to understand if the drivers behind the positive outcomes tie up with their philosophy. This includes performance attribution, assessment against multiple lenses and style analysis.

So much has changed in this market. New providers have arrived, fee pressure has ramped up and sustainable investment approaches have evolved. Even if your DFM was best in class historically, you should be confident they have ‘moved with the times’.

If the answer is no to any of these, we would suggest you consider investing some time in 2024 to getting this information.

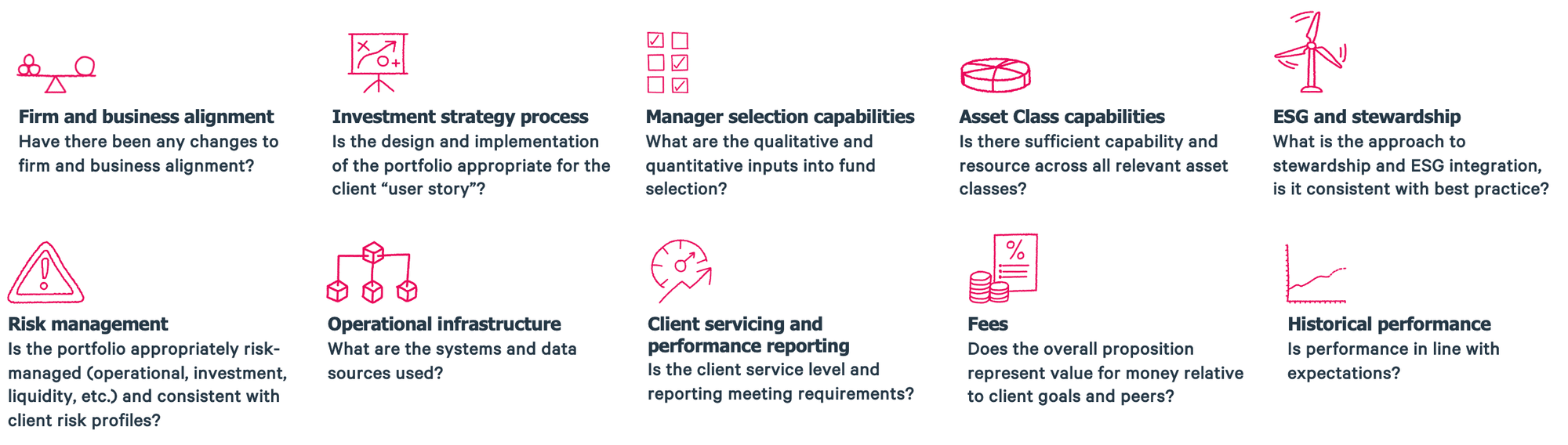

We believe there are 10 factors that need attention when selecting and reviewing DFMs. There are obvious (albeit not necessarily easy to assess) factors such as investment strategy process and manager selection capabilities.

But there are also less exciting areas such as deep diving on risk management, operational infrastructure and how historical performance aligns to the articulated process.

Proper listening isn't easy, but for important relationships it's worth investing the time and energy into doing it properly and getting it right.

Although, for the avoidance of doubt, this 10-factor framework is only suitable for DFM relationships, you might end up with some strange looks if you apply it at home.

Would you like to discuss the service you receive from your current DFM? If you’d like to potentially assess the existing relationship, while considering the best outcomes for clients, we can help. Get in touch with the team to arrange a chat.