WHAT WE DELIVER IN STEWARDSHIP AND SUSTAINABILITY

Jump to a section or flip the page to continue reading.

Through our investment consulting

Through ourmanager research

Through our asset andliability modelling

Through our industryand policy engagement

As an investment consultant, everything we do is driven by a desire to achieve the best possible outcomes for our clients and their beneficiaries. To do so, we follow a framework-based approach focused on reaching client objectives and making a real difference.

Informed by the latest research and insights, we hope to be thought leaders, and aim always to share clear and unbiased views. As we continue to take firm stances on important issues, we thrive on questions and challenges from our clients and the wider industry. They help ensure that our advice and services remain progressive yet pragmatic. This is as true about our work on sustainability and stewardship as elsewhere.

In 2024, we continued to work with clients on a range of sustainable investment topics. We again helped a range of asset owners to further develop their approaches to climate change. For some, this involved helping them to make progress on climate transition plans; others we helped to reframe their approaches to considering climate-related risks. In addition, we worked with clients to further develop their thinking on investment impacts on the wider natural world and society at large, as well as the effects that these could have on their portfolios.

With temperatures (at least temporarily) exceeding 1.5°C above pre-industrial levels for the first time in 2024, digestible, practical and decision-useful climate change analysis and reporting is growing in importance. We recommended that clients build on their learnings from the TCFD reporting process to consider Climate Transition Plans, where a framework is used to identify specific actions to both adapt to and contribute towards the transition to a lower-carbon economy. With this forward-looking approach in mind, we continued to focus on those alignment metrics - such as Implied Temperature Rise - that attempt to capture progress against a real-world emissions target.

Climate Transition Plans are anchored in the actionable and meaningful climate targets that have been set and are tailored to the client type and level of ambition. We worked with clients to consider the principal transition levers of stewardship and investment allocations to achieve the impact implied by these targets. With physical and transition risk in portfolios always front of mind at Redington, we also introduced ideas such as hedging climate-related tail risk or shortening the duration of (or removing exposure to) long-dated credit in the oil and gas majors.

The following case studies show how we work with clients to both support understanding and management of climate risks, while contributing to real economy decarbonisation.

Many of our clients have set climate targets over the past several years. Through 2024 we worked with them to articulate and start to implement Climate Transition Plans.

Transition plans are strategic action plans that organisations (including investors) develop to document the actions they are taking to meet their climate commitments, and the timeframes over which they are delivering these actions.

These plans are vital as they allow for the articulation of a holistic strategy towards Paris alignment, net zero or any other climate ambitions that have been set.

We utilised the existing public guidance on Climate Transition Plans to design a proprietary framework to help clients work through a holistic climate strategy. This focuses on the four levers that can be pulled to make progress towards climate objectives. The four levers are summarised by our IDEAs framework:

Investment: Involves increasing allocations to climate solutions. For example, investing in activities aligned with the climate transition, such as renewable energy and natural capital.

Divestment: Focuses on reducing existing investments that are not aligned with an investor’s climate goals, where there is no or little scope for engagement for change.

Engagement: Involves engaging with fund managers and underlying companies to encourage better delivery of their own decarbonisation trajectories.

Advocacy: Focuses on advocating for policies that support climate goals. It includes influencing the regulatory, legislative, and standards landscape to promote practices in line with climate goals.

We walked our clients through our IDEAs framework, considering their climate objectives, governance structures, and overall investment strategy to allow them to articulate a complete Climate Transition Plan. The clients in question are now working on implementing these plans.

Climate scenario analysis has been a topic of extensive industry debate in recent years. While it offers valuable insights, the limitations of the models used have been widely recognised, rendering it less effective for investors’ decision-making.

In response to these criticisms, the industry’s primary focus to date has been on improving approaches to scenario analysis. However, the challenge remains: modelling something unprecedented and as unpredictable as climate change is inherently difficult.

Given the primary issue with current climate scenario analysis is its limited decision-usefulness, we began exploring alternative approaches to help clients make decisions that better manage their climate risk exposures. We have run workshops with some of our clients to consider potential tail-risk events for their portfolios, and actions they could take to mitigate these. Some of these have used reverse stress tests and other tools to develop clearer understanding of risk exposures.

This remains a key focus for 2025 as we seek to develop our advice further. In particular, we are looking at how clients could tailor their risk management approaches to a world that appears currently on track for temperature rises significantly above the Paris Agreement ambition.

These discussions are ongoing, but we are pleased that our clients are becoming more confident that there are actions that can be taken despite the breadth and scale of the systemic risks that climate change represents.

As in previous years, we are transparent about the progress we are making in supporting clients on climate change matters. The following table provides insight into the extent to which we’ve provided climate-related advice to pension funds, helped them establish metrics and targets, and assisted them in advancing the decarbonisation of their portfolios. We have continued to update this over time to provide insight into the practical outcomes of our advice on climate risks.

We are pleased to report that during, and particularly late in, 2024 we were successful in winning several new clients. One downside of this positive news is that the percentages of our clients shown in various parts of this table have decreased since last year. However, we expect to undertake many relevant activities with these clients over the next year, which means we expect to see these statistics revert to previous levels at least.

Total clients

Trained on climate change

Received carbon emissions data*

Completed TCFD reporting

Invested into climate solutions

Set net-zero commitment

>£5BDefined Benefit

8

88% ↓

63% ↑

100% =

38% ↓

£1-5BDefined Benefit

21

95% ↓

76% ↓

90% ↓

33% ↑

67% ↓

<£1BDefined Benefit

13

77% ↓

23% ↑

15% ↑

Defined Contribution

10

30% ↓

30% ↑

30% =

10% ↑

0% =

*Number notes that climate metrics have been provided by Redington

We are encouraged to see significant increases in the proportions of clients who are invested into climate solutions. As well as reflecting our consulting advice, this reflects the wealth of knowledge our manager research team has on emerging sustainable investment asset classes.

Having worked hard to build strong sustainable research capabilities in recent years, we now have many attractive solutions available for interested clients.

Delivering climate-related advice and services is not only applicable to private sector pension schemes, for many of which it is a regulatory requirement. We continue to work with our wider client base including local authority funds, endowments, foundations, insurers and wealth managers on their approaches in this area.

We are encouraged to see that the proportion of these clients who we have delivered emissions data for, seen invest into climate solutions and which have set a net-zero commitment have all increased. The table below summarises the practical outcomes of our work so far:

20% ↓

32% ↑

48% ↑

*Number notes climate metrics provided by Redington.

We are a member of the Investment Consultants Sustainability Working Group (ICSWG), which brings together leading UK investment consulting firms to improve sustainable investment practices across the investment industry. To support this, in 2021 the ICSWG produced a competency framework to help asset owners assess their consultants’ climate-related investment advice capabilities.

This framework was produced when such advice was relatively nascent. The industry has progressed significantly over the past few years, meaning best practice has also evolved. As a result, we worked with other ICSWG members in 2024 to update the competency framework. In this updated version, several aspects that were previously aspirational are now generally considered a core part of investment consultants’ offerings.

The updated framework also aims better to reflect investment consultants’ important roles in supporting asset owners in keeping abreast of the evolving landscape and the complex interplay of climate competency with related environmental/natural and social factors.

We believe firmly in the importance of asset owners being able properly to assess the capabilities of their consultants, given the importance of their advice to clients’ investment decisions. We are therefore pleased that we have been able to co-author the revised framework, helping asset owners to understand what their advisors should be delivering. Once again this raises the bar for our industry, promoting continued improvement. This report, and the appendix outlining our delivery against the ICSWG expectations, reflects the updated framework.

Stewardship remains a core part of our sustainable investment offering to clients, and we believe that our team’s direct and practical knowledge in this area allows us to provide unique insights. We continue to regard stewardship as a powerful tool that can be used to achieve sustainable investment goals whilst also contributing to real-world outcomes.

Throughout the year we again spoke with many pension funds on the steps they can take to practise better stewardship. In doing so, we helped many select key stewardship themes, a powerful tool to help focus their efforts and provide a basis for assessing and challenging investment managers. We proposed themes that align with the trustees’ - and often the sponsors’ - beliefs. Importantly, we worked to identify potential themes that could be effectively integrated by their investment managers.

One key service that we provide to clients, based on our direct knowledge of stewardship, is assisting them to understand and assess the quality of the stewardship activities that fund managers carry out on their behalf. Our processes and technology seek to hold fund managers accountable for delivering positive stewardship outcomes. Analysis through our proprietary software platform, Ada Fintech, allows clients to make sense of manager voting activity. We also deliver bespoke reports to clients that highlight the votes that matter to them, encompassing but also going far beyond the Most Significant Vote disclosures required by regulation. Additionally, we have developed in-depth assessments of managers’ engagement activities, resourcing, and general approach to stewardship. We deliver these assessments as part of our manager research, as well as on a stand-alone basis for clients already invested in investment managers’ fund offerings.

We frame our approach to stewardship through three key elements: report, assess and engage. We provide tools and advice that enable clients to: understand and make sense of what is being done on their behalf (report); consider whether that is good enough and identify any areas of weakness (assess); and challenge and press managers to deliver more (engage).

We provide each element independently or as a bundle, depending on clients’ specific needs. Overall, our stewardship services respond to two distinct needs among asset owner clients:

To have insightful material for their own reporting needs (including Implementation Statements, Stewardship Code responses, and/or other public disclosures of stewardship)

To hold their fund managers accountable and call for more from them, ensuring that asset owners can play their role in delivering good stewardship.

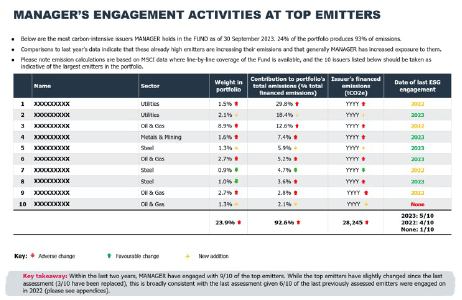

We provided a large UK asset owner with unique insights into the stewardship delivery by two of its leading managers.

Below are examples of the key insights gathered and presented

As well as highlighting the engagement coverage of key investment exposures (assessed according to several characteristics – the listing of the top 10 exposures in terms of financed emissions, as shown, is just one of these), this revealed gaps in engagement activity.

We also looked in detail at the substance of the engagement that was delivered, and shared views on the quality of delivery by the manager, as well as of its voting policies and practices.

Alongside this detailed quality assessment, we highlighted particular investments of concern as well as the need for engagement with these companies. This analysis provided tools for client understanding and specific questions that might be asked of each manager.

We also sat alongside the client in meetings with the managers, supporting them in the use of the tools and analysis we had provided, thus enabling an especially robust discussion of the managers’ approach and practical delivery.

One manager was providing a stewardship update to the client for the second year in a row, and we shared the client’s disappointment that the problems we had previously identified and communicated to the manager persisted. If anything, the manager had increased the risk exposures in the fund, but had not sought to mitigate them through heightened engagement.

Subsequent to the meeting, the client decided to replace the manager.

Asset owners are increasingly recognising the importance to long-term investment returns of the political and regulatory context within which they invest. Many are keen to consider systemic risks, and to participate in public policy debates as a way of mitigating and managing these risks.

A client of ours, a large UK asset owner, is one such, and we worked with them to enhance their industry-shaping engagement process by considering the appointment of a specialist public policy engagement service provider. Once the client agreed that this was a worthwhile approach, we also led a process by which a provider was chosen.

We extended the opportunity for appointment to a selection of potential providers and critically reviewed responses in order to find the best solution for the client’s requirements. As part of the review, we assessed the breadth of providers' offerings across geographies and issues, as well as alignment with the client's existing active stewardship themes.

We provided the client with our recommendation for a preferred specialist engagement provider and the client has subsequently appointed the provider to undertake its industry shaping work. By appointing a provider, the client will be better placed to collaborate at an industry-level and leverage its influence as an asset owner.

We have also taken the opportunity to provide detailed feedback to the provider whose offering was determined to be second best in this case. We are keen to foster multiple quality providers of these services, which we believe will become increasingly important to clients in the coming years. The provider welcomed the feedback and made clear that it would be working to respond to it.

ESG, stewardship and impact considerations play an integral role in our approach to manager screening, selection, and monitoring. We are committed to identifying managers with the philosophy and skillset to support asset owners on their sustainability journey.

In 2024, we advised clients on converting their sustainable investment objectives and strategy into impactful allocations. Notably, we researched and provided new, sustainable options in Social & Affordable Housing, Nature-Based Solutions, Impact Private Credit, and Passive Equity – seeing clients make capital allocations to each of these Preferred Lists by year-end.

Furthermore, we continue to leverage data and embed sustainability considerations as part of our research process. We issue an annual Sustainable Investment Survey which covers topics at both the strategy and firm level related to ESG integration, stewardship & engagement, climate change, impact investing, and diversity, equity & inclusion. Data can be accessed by research and client teams alike to find both strengths and areas for improvement in managers’ approaches, empowering us with the tools to better hold managers to account.

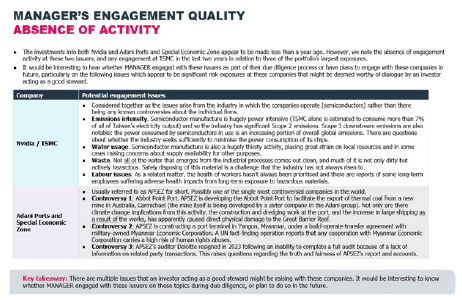

In the prior year, Redington had raised questions with a fund manager regarding exposure to potential corruption risks. This was due to the proximity of a client asset to an area about which significant allegations have consistently been made in recent years. At the time, we received full reassurances that there was no risk of the client asset becoming exposed to these risks.

We were therefore disappointed this year to see news that made clear that there was an attempt being made to encompass the asset and its surrounding site into the area that is subject to alleged corruption. We raised our concerns directly and fully with the manager and followed up in discussion with the client, which also maintains a direct relationship with the manager.

During subsequent discussions with the manager and client, we uncovered reports from reputable sources that made clear that the asset itself was directly contacted by the parties to the alleged corruption. Disappointingly, our conversation was the first the manager had heard of these reports.

By raising these issues directly and frankly with the manager, as well as sharing insights with the client, there should be greater protection of this asset from the risk of corruption. In particular, by the management of the asset itself having been contacted by one of its underlying asset owners, the potential for reputational issues may provide a readier protection from corrupting influences should any further approaches be made.

Passive managers are required to track an index closely, which means they cannot simply divest of companies with poor ESG characteristics. As a result, their delivery of engagement and voting is of critical importance. We found limited differences between the top passive managers’ performance and tracking error against the benchmark. However, there was significant variation in their approaches to stewardship, making it a key differentiating factor in our process of identifying a passive equity preferred list of managers.

When evaluating a passive manager’s approach to stewardship, we focus on several key factors. We seek evidence of active engagement and voting across the full passive equity platform, including a willingness to use (where appropriate) escalation tools such as AGM attendance, the proposal of shareholder resolutions, and public statements relating to contentious issues. Managers should have robust voting policies, apply appropriate judgment and take an active stance when necessary.

We expect managers’ sustainable investment teams to be well resourced and deployed proportionately across all fund management teams, supported by the technology and systems necessary to track stewardship efforts. Firm-wide accessibility to voting and engagement data is crucial for informing broader perspectives. In addition, active participation in key investor groups and coalitions enhances a manager’s engagement effectiveness through greater access to companies and collaboration with other investors.

Our assessment of the passive equity universe led us to rate a global leader in indexation as "remove" (our most negative rating) due to significant shortcomings in their stewardship approach. We judged the manager’s engagement efforts to be negligible due to the limited headcount in their stewardship team, with a focus on disclosure rather than advancing sustainability issues within companies. Furthermore, the manager’s activities are heavily focused on the US market, with insufficient delivery in other regions. Additionally, we found their participation in investor groups was weaker than peers, limiting the impact of their engagement efforts. Unlike its competitors, the manager lacks robust tools for escalating and delivering change, which is essential for effective stewardship.

The “remove” rating of a leading global passive provider signals our commitment to maintaining high standards in stewardship and engagement. Several clients have shifted mandates, or are considering changes, based on this advice.

Following the passive equity preferred list process, we have been actively working with the manager, offering guidance on enhancing their stewardship practices. This collaborative effort reflects our dedication to improving the sustainable investment landscape. Our goal is to ensure that asset owners benefit from sound investment practices and that managers act as responsible and effective stewards of investors’ capital.

We believe better governance processes are key to unlocking long-term value for these firms and their clients.

In 2024, Redington continued to work with various managers to institutionalise their processes. This year, we identified areas for improvement in certain firms’ governance practices and engaged with them, with the core objective of improving the quality of their decision-making inputs.

For example, we worked with one of our preferred list managers in the impact private credit space to formalise a veto right for its Head of Stewardship on deals in the sustainable portfolio. This provision explicitly enables the Head of Stewardship to block investments should they not satisfy the Fund’s impact objectives. Whilst the manager would not invest if there were red flags from an impact perspective in practice, we believed formalising this was important from a governance perspective to validate the Fund’s impact credentials.

Similarly, we engaged with a social & affordable housing manager on the overrepresentation of deal team professionals in its Investment Committee. Following our conversations, the firm brought in two external non-executive Investment Committee members, leading to more independent and robust decision-making.

We have seen changes from these dialogues, and we aim to continue our engagement efforts to drive better outcomes for managers and asset owners.

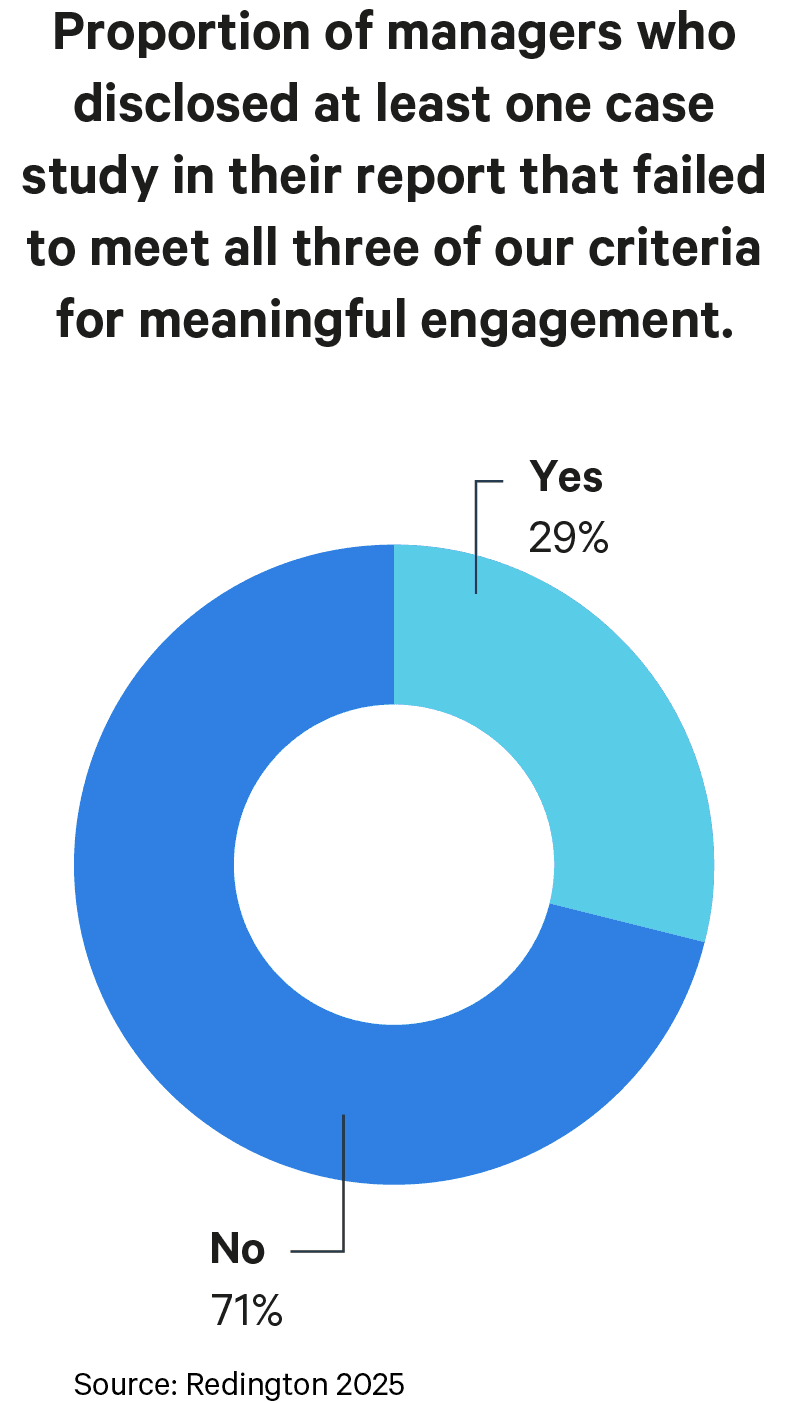

For the third year running in 2024, we assessed how investment managers reported against the Stewardship Code, sharing our findings in our annual analysis of reporting. We use this to assess engagement quality across the investment industry and highlight to managers where improvements can be made.

Whilst we were encouraged to see a considerable increase in disclosure of key statistics from managers – for example engagement theme and geography – we still emphasise that managers can do more. This is particularly the case regarding the overall quality of engagements that managers are delivering.

Following on from our work last year to assess case study materiality within reports, we looked to identify managers falling behind the pack. We did this by assessing the proportion of managers who disclosed at least one case study in their report that failed to meet all three of our criteria for meaningful engagement. These criteria are: proactivity, engagement on substantive issues (not just disclosure or voting) and engagement aiming to deliver a material outcome. As shown, the results were eye opening, with 29% of managers disclosing at least one case study that did not meet any of these criteria. Given that case studies represent a cherry-picked small proportion of the overall activity, this failure is of particular concern.

We will continue to use this analysis to shine light on where managers can make stewardship and engagement improvements.

At the core of what we do sits asset and liability modelling. Carried out by a dedicated team, this quantitative analysis drives our investment advice to clients. Our team has integrated ESG analytics into their modelling capabilities, with this providing helpful insights to aid decision-making. Their outputs are also central to client reporting, most notably for climate. This involves a wide range of metrics, from calculating the emissions associated with investments to assessing how portfolios might be affected in different climate scenarios.

In 2024 the modelling team made numerous developments to our approach, from releasing sovereign bond emissions reporting to incorporating updates into our climate scenario analysis methodology. Our modelling team has also worked to refine their climate reporting outputs. This has consolidated our offering after having developed this over several years to support reporting in line with the Taskforce on Climate-related Financial Disclosures framework.

The result is an enhanced report, with a clear narrative and outputs on the different metrics and underlying assumptions, which can readily be transferred to client reports. This not only improves the utility of the report for clients but also enhances efficiency and minimises the risk of errors when using the information in compliance reports.

Implied Temperature Rise (ITR) is a metric used to estimate the potential future temperature increase associated with a portfolio's carbon emissions. ITR provides investors with a forward-looking view of the climate impact of their investments by translating carbon emissions into an estimated temperature rise. Our clients use ITR primarily for:

Assessing Climate Alignment: Investors use ITR to determine how well their portfolios align with global climate goals. It helps identify whether investments are on track to meet the targets set by the Paris Agreement, which aims to limit global warming to well below 2°C, ideally closer to 1.5°C.

Enhanced Decision-Making: ITR provides investors with a clearer picture of the long-term climate impact of their investments. This drives more informed decisions that can help the portfolio align with temperature goals.

Engaging with Companies: ITR can be used to identify those companies in a portfolio that contribute the most to climate change. This information can be used to prioritise investor engagement.

While ITR is in itself helpful to investors, it does not account for the benefits of investing in climate solutions (such as natural capital, renewable energy infrastructure, or climate-focussed impact private equity). To address this issue, we have adapted the traditional ITR metric to create an impact-adjusted ITR, which provides a more comprehensive view of the carbon impacts of investments, taking into account - for example - the carbon sequestration benefits of natural capital assets in calculating an asset’s ITR.

We now deliver to clients a more intuitive forward-looking climate metric, which more fully reflects the impacts that particular investment allocations can have. This helps frame proactive climate-aware decision-making by trustee boards and potentially facilitates more investment into climate solutions.

We recognise that in many areas we can be more effective and deliver more for our clients by working collaboratively with others. We also know that many sustainability issues can only effectively be addressed through broad industry-wide and/or policy approaches that reflect the systemic nature of the issues.

We are therefore active in working with other investment consultants – and other participants in the investment chain – to engage on public policy and best practice developments. We maintain strong networks across the investment industry and often work with peers to promote consistent responses to consultations on those frequent occasions when our perspectives coincide.

Redington was instrumental in the creation of the two collaborative bodies in the investment consultant community, the Investment Consultants’ Sustainability Working Group (ICSWG) and the Net-Zero Investment Consultants Initiative (NZICI – our industry’s contribution to the Glasgow Financial Alliance for Net Zero, or GFANZ) and remain represented on each group’s steering committee and various working groups.

During the year, we have worked as part of ICSWG to update and enhance some of its existing guidance and continue to be part of the NZICI members’ progress to deliver their stated commitments. Most notably at ICSWG we were part of the group that led the update of the climate competency framework for consultants, as well as the group that spearheads direct dialogue with regulators.

In the following pages we provide case studies of some of our key activities in these areas over the last year. We also set out our memberships of various collective bodies, and our approach and involvement in regulatory consultations.

We were pleased to provide one of only two investment consultant participants in the fiduciary duties working group of the Financial Markets Law Committee (FMLC), which produced its final report early in 2024.

We believe that we were invited to join the working group because of our prior work in the area (notably our work in highlighting the limitations, arising from current interpretations of fiduciary duty, that constrain pension scheme investment in green gilts), and we actively participated in the development of the report, bringing to bear our real-life experience of the challenges of decision-making in trustee boardrooms.

We were pleased by the final report, which in its 18 pages deals accessibly with issues that were discussed over hundreds of pages by the Law Commission a decade ago. It is enormously valuable that the report avoids the Law Commission’s complex approach to so-called ‘non-financial’ factors, clarifying that as long as trustees approach climate and other sustainability matters through the lens of investment risk and return, they are acting fully within their fiduciary duties.

While we regard the final report as a major step forwards in itself, that was not the end of the story for us. Most important is that the report’s clarifications are heard by trustees and that they actually help to shift decision-making. We therefore took multiple opportunities to promote the report from public platforms, as well as within trustee boardrooms. We presented on the FMLC work to two of the major firms of professional trustees as well as to several individual client boards.

We also had an active dialogue with the regulators about what more they might do to promote the report, before this work went on hold in the pre-election sensitivity period and as the new government sets its strategic aims. We remain in discussions with industry peers about how to further advance the broad understanding that incorporating climate and other sustainability factors into investment decision-making is wholly in accord with trustees’ fiduciary duties.

Having played an active role in their development, Redington was pleased to be a founding signatory of the Sustainability Principles Charter for the Bulk Annuity Process, launched in early 2024 under the banner of Accounting for Sustainability (A4S). This initiative seeks to ensure that pension fund trustees can have confidence that their sustainability ambitions will be met by the insurers that provide buy-ins or buy-outs of their scheme liabilities. The Principles – signed by most of the insurers providing bulk annuities – set out clarity on transparency, reporting and engagement before and after such transactions.

We have reinforced this launch over 2024 by collaborating with other working group participants on a common questionnaire for insurers regarding their sustainability commitments, resourcing and delivery. This common questionnaire should streamline the marketplace by reducing overall reporting burdens on insurers, while making clear the broadly shared industry ambition to effectively deliver on sustainability matters. This common questionnaire was published on the anniversary of the launch of the Charter.

This initiative shines a key light on a neglected area of the market from a sustainability perspective. While buy-outs in particular are one-off transactions and trustees have no ongoing oversight role, many wish to ensure that their commitment to sustainable investment on behalf of beneficiaries is carried forwards after the transaction as effectively as it was before. For many, this means the sustainability credentials of the insurer are a key element of decision-making. This industry-wide effort raises the status of these issues and provides a clear basis for transparency and competition to develop on sustainability delivery by insurers.

Overall, we’re active participants in the following groups:

Diversity Project – the industry-wide group promoting diversity across all dimensions in the investment industry. We are active participants in a wide range of workstreams, supporting the development of best practices.

Financial Markets Law Committee’s fiduciary duty working group (FMLC) – FMLC was asked by the government to take forward a project making clear that addressing climate change is consistent with fiduciary duty. See case study.

Glasgow Financial Alliance for Net Zero (GFANZ) Sectoral Decarbonisation Working Group – we are members of this group, which aims to develop guidance to support financial institutions’ use of sectoral pathways in the creation of net-zero transition plans, alignment of portfolios, and engagement with real-economy firms, consistent with climate science to achieve 1.5°C targets.

Institutional Investors Group on Climate Change (IIGCC) – as members of this group representing investors that consider the implications of climate change in their investment approaches, we have actively participated in the development of IIGCC best practice guidance.

Investment Consultants’ Sustainability Working Group (ICSWG) – we were a founder of this initiative, focused on sharing best practices and raising standards among investment consultants and the investment industry as a whole. We remain represented on the steering committee.

LGPS Scheme Advisory Board – a responsible Investment Advisory Group, supporting local authority funds and pools in responding to developments, with a particular focus on fiduciary duty and the possible forthcoming climate reporting requirements.

Net-Zero Investment Consultants Initiative (NZICI) – investment consulting’s contribution to GFANZ, the finance industry’s commitment to net-zero. We and a dozen other consulting firms have committed to deliver net zero in our own businesses but more significantly through our advice. We sit on its steering committee.

Taskforce on Social Factors – a group fostered by government departments working to assist pension funds to think through the challenge of the S in ESG, and how to respond effectively. We were the sole investment consultant sitting on the steering committee. The Taskforce reported during 2024, and we actively promoted its conclusions over the year.

Among other groups we’re also members of:

Pensions and Lifetime Savings Association (PLSA)

the International Corporate Governance Network (ICGN)

UN-supported Principles for Responsible Investment (PRI)

We actively respond to relevant public consultations on policy matters. As a service provided to clients at their request, we will also support their responses to consultations that they deem relevant. In addition, Redington colleagues are active participants in a number of industry representative committees and other groups that respond to some consultations (including at CFA UK, the Corporate Reporting Users’ Forum and ICSWG), on which we also seek to have influence to ensure that the broader voice of the investment community is heard on relevant issues.

As one example, in Q3 2024 we responded to the Financial Conduct Authority (FCA) consultation on the Value for Money Framework. We also actively participated in roundtables held by the FRC considering potential changes to the UK Stewardship Code.

Redington also supports its staff in becoming members of key public policy bodies, with one individual joining the UK Sustainability Disclosure Technical Advisory Committee (TAC) when it was founded in 2024. The TAC held detailed technical discussions through the year and in December issued its formal recommendations to the Secretary of State on the UK’s adoption of the International Sustainability Standards Board’s reporting standards S1 and S2. These seem likely to be reflected in the government’s consultation on adoption, expected in 2025.