WHAT WE DELIVER IN STEWARDSHIP AND SUSTAINABILITY

Jump to a section or flip the page to continue reading.

Through our investment consulting

Through our manager research

Through our industry and policy engagement

Looking to the future

As an investment consultant, everything we do is driven by a desire to achieve the best possible outcomes for our clients and their beneficiaries. To do so, we follow a framework-based approach focused on reaching our clients’ objectives and making a real difference.

Informed by the latest research and insights, we hope to be thought leaders, and aim always to share clear and unbiased views with our clients. As we continue to take firm stances on important issues, we thrive on questions and challenges from our clients. They help ensure that our advice and services remain progressive yet pragmatic. This is as true about our work on sustainability and stewardship as elsewhere.

Following a turbulent end to 2022, when navigating the gilts crisis captured all and more of our clients’ governance bandwidth and agendas, we welcomed the opportunity to spend more time discussing sustainable investment topics in 2023. As we continued to support our clients in their approach to stewardship, climate change and TCFD reporting, we were able to go further in setting actionable targets and holding fund managers to account. We were also able to turn our client’s attention to society’s impact on the natural world, working with clients on understanding nature-related risks and how to invest in a nature-positive way that can help address the challenge of delivering net zero carbon emissions.

2023 saw the requirement for DB pension schemes over £1bn to implement climate change governance requirements and publish TCFD reports under the DWP’s Occupational Pension Schemes (Climate Change Governance and Reporting) Regulations 2021. To help our clients meet this requirement, we updated our default climate advice. This is designed to be practical and actionable for each of our clients based on their priorities and constraints.

Based on our clients’ objectives, our advice seeks to manage climate risk and achieve real economy decarbonisation. To do so, we favour forward-looking metrics rather than backward-looking reporting on emissions from client portfolios. Similarly, we favour metrics considering outcomes over those capturing processes.

Specifically, we updated our advice to reference Implied Temperature Rise (ITR) as a recommended portfolio alignment metric for TCFD reporting. Recognising that emission measures are inherently backward-looking, this metric allows our clients to capture progress against a real-world emissions target.

We recommend our clients set both an actionable and meaningful target, tailored to their client type and level of ambition. As setting a target implies a change in behaviour, we then work with our clients to use stewardship and investment allocations as their primary levers of influence to achieve the impact implied by the target.

The following case studies show how we work with clients to set targets in practice.

Our client was a local government pension scheme which had agreed a commitment to achieve carbon neutrality (net-zero carbon emissions) by 2040. Given the long-term nature of this target, we worked with them to set shorter-term targets that could be monitored in the interim, helping shape decision-making over the next few years.

Whilst the 2040 net zero ambition, and the client’s progress to date, demonstrated a desire to achieve portfolio decarbonisation, we began by recommending that any interim target set should be focused on real economy outcomes. More specifically, given the client’s climate ambitions, we recommended that they should adopt climate targets for emissions reduction, portfolio alignment and climate solutions.

To ensure any proposed target was suitably ambitious and aligned with the client’s beliefs, we discussed and agreed the following criteria:

Widen the scope of climate targets: the target should allow the client to track a wider scope of assets and sources of emissions in the portfolio.

Requires action: the target should spark a change in investment mindset, striving to achieve real economy decarbonisation.

Aligned with peers and established norms: the target should clearly demonstrate a meaningful but credible commitment.

Forward-looking: given the existing emissions target is inherently backward-looking, the proposed target should provide insights into the forward-looking trajectory of the portfolio.

To meet the final criterion, we introduced the client to the Implied Temperature Rise (“ITR”) metric.

We recommended a three-pronged approach to interim target setting, focused on emissions reduction, alignment of assets and allocation to climate solutions. The targets, which were agreed by the client, will provide a framing for future decisions on the shape of its investment portfolio.

Our client, another local government pension scheme, had already set an interim decarbonisation target for the Fund’s equity allocation, and was looking to take the next steps in its net zero journey by extending its decarbonisation targets to other asset classes. We agreed that illiquid assets would be a pragmatic next step, and narrowed this down to the Fund’s Real Estate allocation given availability of data and the convergence of available methodologies for this asset class.

We started with a training session for the client on industry best-practice and the key challenges of setting decarbonisation targets for illiquid mandates. We also highlighted opportunities for the Scheme, notably helping to decarbonise the built environment – a contributor of c.40% of annual global emissions.

The next phase of the project included baselining both the building emissions intensity and the carbon footprint of the client’s portfolio. We also analysed decarbonisation pathways using the Carbon Risk Real Estate Monitor (CRREM) tool.

We recommended that the Scheme set three climate targets for the directly-held property within its real estate fund focused on decarbonisation, coverage and engagement respectively.

We also highlighted some future considerations for the Scheme:

Set targets for the Real Estate Equity Funds allocation over the subsequent 12 months.

Monitor developments in the measurement of embodied carbon emissions (covering whole-life carbon) so that these could in future be incorporated in target-setting for both Directly-held Real Estate and Real Estate Equity Funds.

The following table provides insight into the extent to which we’ve provided climate-related advice to pension fund clients, helped them establish metrics and targets and assisted them in advancing the decarbonisation of their portfolios. We have undertaken to continue to publish this table over time to provide insight into the practical outcomes of our advice on climate risks.

We are encouraged to see the majority of statistics increase, choosing to also report this year the percentage of clients who have set a net-zero commitment. Whilst we provide carbon emissions data to a smaller proportion of our >£5bn defined benefit clients, this is in large part due to a number of clients falling below the £5bn threshold following the gilts-crisis. Likewise, the proportion of DC clients trained on climate change has decreased owing to new clients onboarded in the year and the nature of our advisory relationships with them.

Total clients

Trained on climate change

Received carbon emissions data*

Completed TCFD reporting

Invested into climate solutions

Set net-zero commitment

>£5BDefined Benefit

6

100% =

50% ↓

100% ↑

50% ↑

100%

£1-5BDefined Benefit

22

77% ↑

91% ↑

27% ↑

68%

<£1BDefined Benefit

16

80% ↑

19% ↑

13% ↓

6% ↑

20%

Defined Contribution

10

40% ↓

10% ↑

30% ↑

0% =

0%

*Number notes that climate metrics have been provided by Redington

Delivering climate-related advice and services is not only applicable to our private sector pension scheme clients, for many of which it is a regulatory requirement. We continue to work with our wider client base including local authority funds, endowments, foundations, insurers and wealth managers on their approach to climate change. The table below summarises the practical outcomes of this work so far:

24%

28%

44%

*Number notes that climate metrics have been provided by Redington.

With the Kunming-Montreal Global Biodiversity Framework agreed at COP15 in December 2022 and the final recommendations of the Taskforce on Nature-related Financial Disclosures (TNFD) released in September 2023, it is safe to say that protecting the natural world around us has shifted into the spotlight for policymakers, companies and investors.

Until recently, human pressures on nature have been less appreciated than our impacts on the climate, even though we have already passed the safe operating space for biodiversity loss, and climate change and nature are deeply interrelated. More than half of the world’s GDP is dependent on nature, with deforestation, land degradation and biodiversity loss the primary nature-related risks facing the global economy.1

Nature is, however, a challenging area for investors for several reasons: measurement is more difficult than for climate, impact is local (and so aggregating measures is harder), investing in biodiversity is about avoiding the worst and restoring what’s been altered, and biodiversity themes overlap with other environmental themes. However, it is now widely accepted that climate change and biodiversity loss are interlinked and should therefore be considered together. As a result, the focus is shifting towards nature-positive net zero, with frameworks being produced for nature that build on those for climate change, and a range of investment solutions emerging.

We have therefore been working with clients to establish nature-positive net-zero strategies.

1 World Economic Forum, 2020: Half of World’s GDP Moderately or Highly Dependent on Nature, Says New Report > Press releases | World Economic Forum (weforum.org)

Over the last year, we have been working with a large UK endowment to develop a net-zero strategy that is ambitious, achievable, and, crucially, nature-positive.

We started with detailed training on the inter-relationship between nature and climate, and the need to consider both in tandem on the road to a net-zero world. This included, among other things, the regulatory environment, net-zero in the real economy, the key drivers of nature loss, the importance of natural carbon sinks, and also an introduction to some of the metrics available for investors to start identifying nature-related risks within portfolios. We then proceeded with an in-depth climate and nature analysis of the endowment’s portfolio, baselining the portfolio on a variety of metrics and highlighting any specific companies, funds and sectors particularly exposed to climate and nature risk.

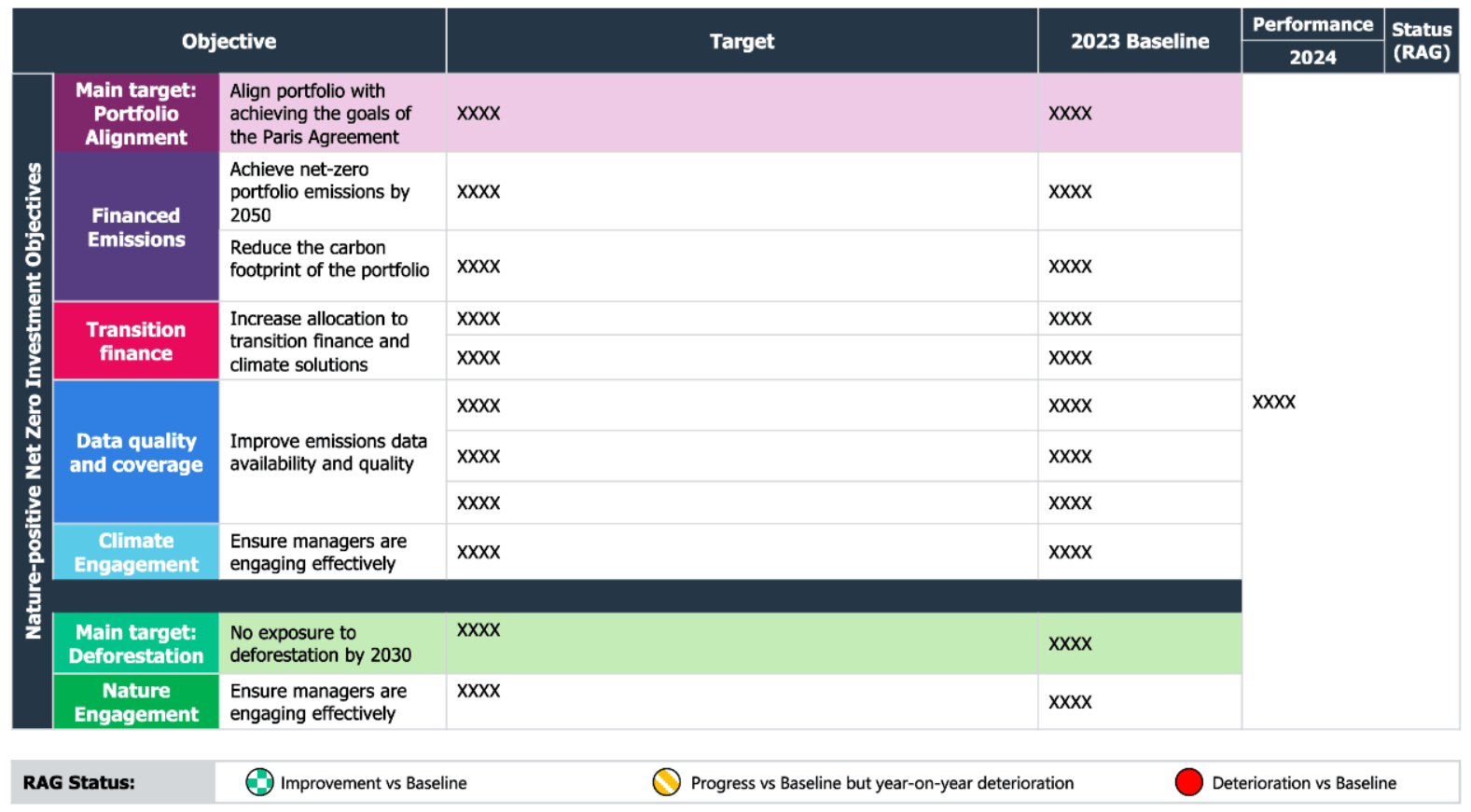

We took this analysis one step further and worked with the client to set ambitious and robust nature-positive net-zero targets. We also developed a Net-Zero Dashboard to ensure monitoring of progress against the stated targets. The endowment’s chosen targets centre around forward-looking climate objectives and deforestation-oriented engagement objectives to respond to the nature challenge. We continue to work with the client to ensure accurate monitoring of progress against these nature-positive net-zero targets.

We recognise stewardship is a powerful tool that our clients can use to help achieve their sustainable investment goals whilst also contributing to real-world outcomes.

Throughout the year we were pleased to have the opportunity to speak to many of our clients on the steps they can take to practise better stewardship. In doing so, we helped many select key stewardship themes, a mechanism to help focus their efforts and provide a basis for assessing and challenging their investment managers on stewardship. We proposed themes that were aligned to the trustees’ and sponsors’ beliefs and, importantly, could be effectively integrated going forward. The stewardship themes chosen by our client base are outlined below.

We are keenly aware of the difficulties our clients face in understanding and assessing the stewardship activities that fund managers carry out on their behalf.

In response to this challenge, we have developed processes and technology to hold fund managers accountable for delivering positive stewardship outcomes. We’ve implemented tools via our proprietary software platform, Ada Fintech, allowing clients to make sense of manager voting activity, and delivered bespoke reports to clients that highlight the votes that matter to them. Additionally, we have developed in-depth assessments of managers’ engagement activities, resourcing, and general approach to stewardship.

We frame our approach to stewardship through three key elements: report, assess and engage. We provide tools and advice that enable our clients to: understand and make sense of what is being done on their behalf (report); consider whether that is good enough and identify any areas of particular weakness (assess); and challenge and press managers to deliver more (engage).

We provide each element independently or as a bundle, depending on our clients’ specific needs. Overall, our stewardship services respond to two distinct needs among our asset owner clients:

To have insightful material for their own reporting needs (including Implementation Statements, Stewardship Code responses, and/or other public disclosures of stewardship)

To hold their fund managers accountable and call for more from them, ensuring that asset owners can play their role in delivering good stewardship.

Over 2023, we rolled out a more systematic process for working with clients on each of the three key elements mentioned above. One such example is described in the following case study.

We worked with a large UK asset owner to give them an in-depth understanding of the stewardship activities undertaken on their behalf by two equity fund managers.

We provided detailed analysis of each manager for the client in advance, looking at both engagement coverage and quality with the leading exposures within the fund, and also voting policies and practices. Following this analysis, we took part in meetings with the managers alongside the client, enabling robust discussions of the managers’ approach and practical delivery.

For one manager, we and the client were largely content with the approach and reassured by what we heard in the meeting, and only limited follow-up was needed.

For the other manager, our analysis identified significant gaps in their stewardship approach, across both engagement and voting. The dialogue served to confirm this analysis, and following the meeting the client agreed with the depth of our concerns. We agreed an approach to seeking enhancement of the manager’s delivery of stewardship. This included drafting for the client a letter setting out their areas of concern and where a change in the manager’s approach is needed, a follow-up discussion to provide further feedback, and a request for a further similar meeting with the manager after a year has elapsed. We look forward to exploring any developments to their approach at that forthcoming meeting, and then to working with the client on further next steps.

In manager research, we recognise our privileged position and duty to be responsible gatekeepers of capital – acting as a critical link between asset owners and asset managers. As such, ESG, stewardship, and impact considerations continue to play an integral role in our approach to manager research, selection, and monitoring.

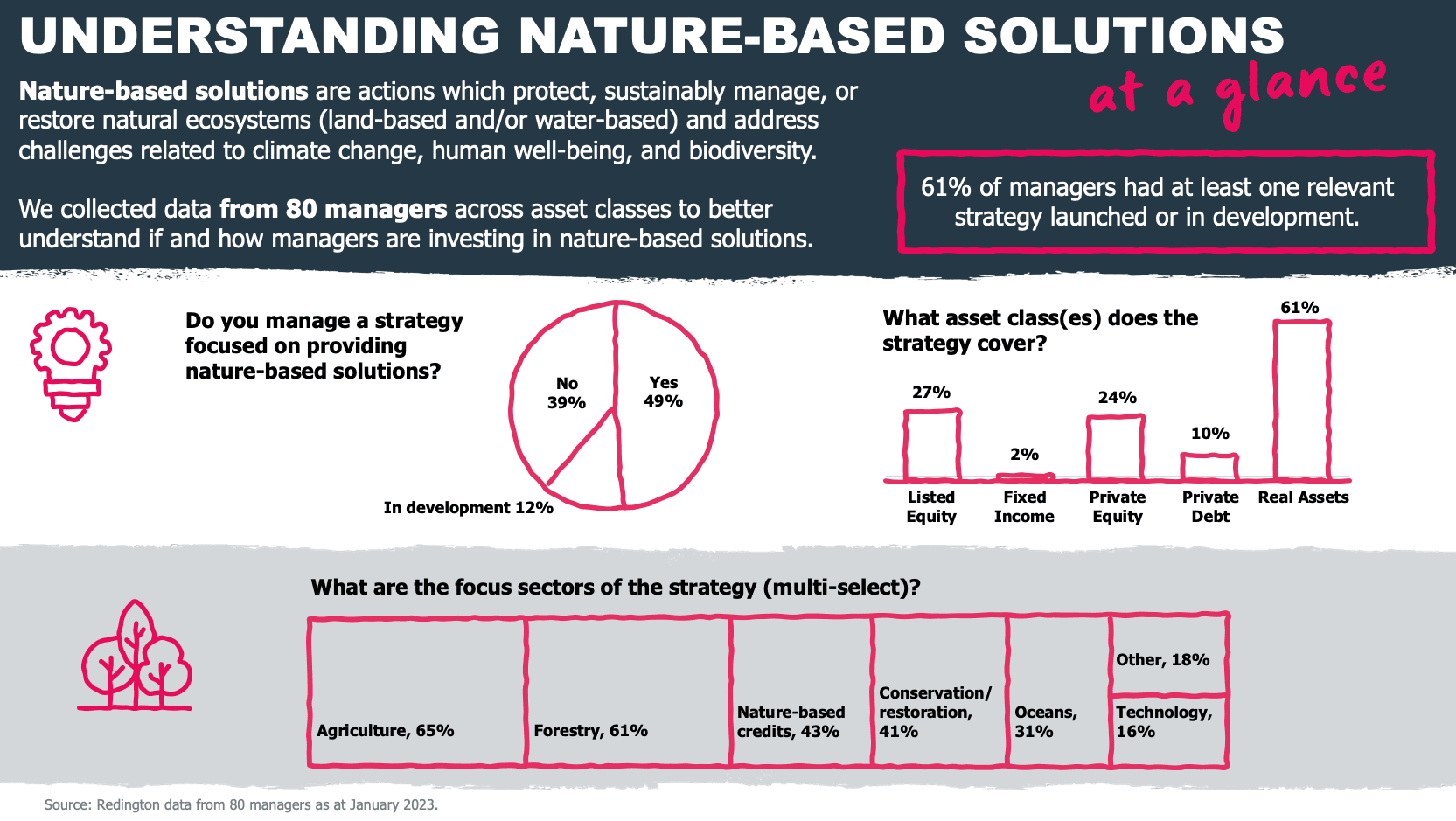

We research impact or sustainable asset classes and products to support our clients in meeting both their sustainable investment objectives and their financial objectives. As part of this, we have identified best-in-class opportunities in the impact and sustainability space across numerous asset classes, including Impact Private Equity, Low Carbon Absolute Return Bonds, Social & Affordable Housing, Renewables, Impact Private Credit, Climate Impact Listed Equity, and, most recently, Nature-based Solutions. We continue to be at the forefront of impact research – acknowledging our role in supporting the allocation of asset owner capital towards positive, real-world solutions.

Beyond finding impact or sustainable investment solutions for clients, we embed sustainability into our research process across our entire manager universe, regardless of asset class. In particular, we undertake ESG integration, stewardship, diversity, and culture reviews and assessments through desk-based research, portfolio reviews, face-to-face meetings dedicated to ESG, and the issuance of an annual Sustainable Investment Survey. We leverage the insights to form views on managers, and to hold them to account for lagging performance. We engage with managers on an ongoing basis (both proactively and reactively) to support them on their respective sustainable investment journeys. Our effectiveness is underpinned by our established relationships with managers, founded on trust, collaboration, and industry-recognised sustainable investment expertise.

We are constantly looking for innovative solutions which meet both the financial and impact objectives of our clients. Nature-based solutions offer an incredible opportunity to benefit from financial returns that are attractive whilst also contributing to the restoration of our natural ecosystems. As gatekeepers of institutional capital, we recognise that we can play a key role in helping to expand nature markets. Given this, we spent 18 months researching nature-based solutions to develop our Preferred List of best-in-class investible solutions for clients.

In August 2023, our Investment Strategy Committee signed off two managers for our Nature-based Solutions Preferred List. Based on this work, we are now positioned to support our clients in making allocations to nature-based assets which deliver financially whilst also providing long-term positive impacts for people and the planet. We hope to expand our list over time as the nature space develops further.

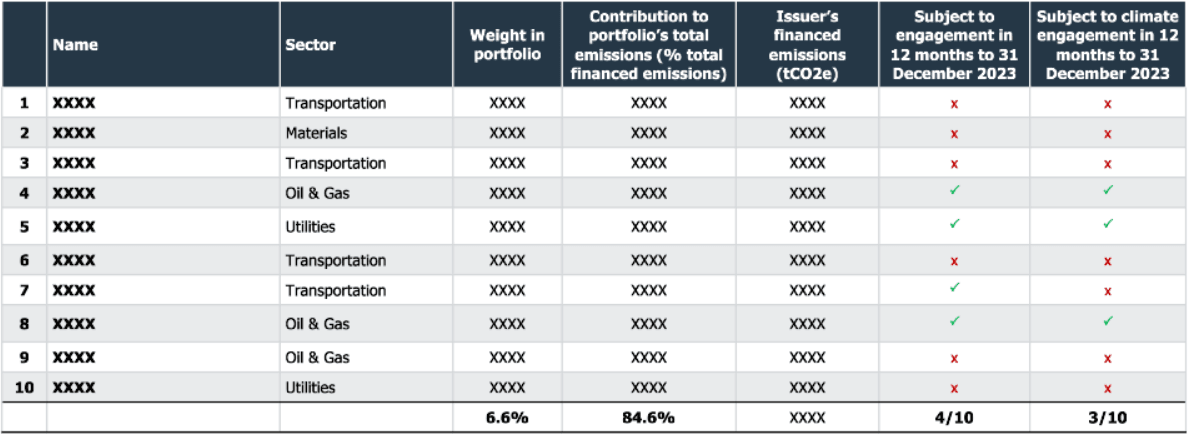

We worked with a pension fund client to review their voting approach and subsequently identified a systemic failure to vote by one of their managers.

We identified a fund among their equity investments where the number of delivered votes did not align with the level which we would expect given the nature and breadth of the fund universe. We subsequently challenged the manager and discovered that they had not been voting at any of the US holdings within the fund since 2014, when the fund vehicle was established. We also discovered that this was the case for a second sister fund run by the manager.

Given this information, we worked to detect the gaps in their voting system which had allowed this failure to arise. We sought to understand how the issue had persisted for so long without detection by the manager.

Following our advice, the investment manager has tightened up its voting procedure to avoid such an issue occurring again in the future. The manager also confirmed that it would communicate details of the issue to all relevant clients, not just those who are mutual clients of ours. As a result of our analysis and intervention, our clients, and other clients of this manager, are now receiving a fuller voting service on their investments than would otherwise have been the case.

In our analysis of multiple managers' voting data, we identified an anomaly regarding their approaches to voting on gender diversity.

We found that managers who are promoting board gender diversity actually appear to be voting against women on boards in order to reflect this intent. For the most part, these women were chairs or members of the nomination committees at companies with fewer women directors than the relevant market threshold for diversity.

This occurrence was usually a reflection of mechanical voting approaches which did not incorporate human intervention to override anomalous results, and voting policies which were not diligent enough to avoid these. In some cases, managers voted against all women on particular boards whilst purporting to promote board gender diversity. We clearly regard this as extremely counter-intuitive, as do our asset owner clients when we have discussed this with them.

We have challenged individual managers on this approach, urging them to update their voting policies to avoid this from happening or manually intervene where this is occurring. We also highlighted this issue at our Investment Conference in December 2023 and will continue to press for change. Some managers have already responded; others appear to continue to believe that their approach is appropriate. We will maintain our engagement with them.

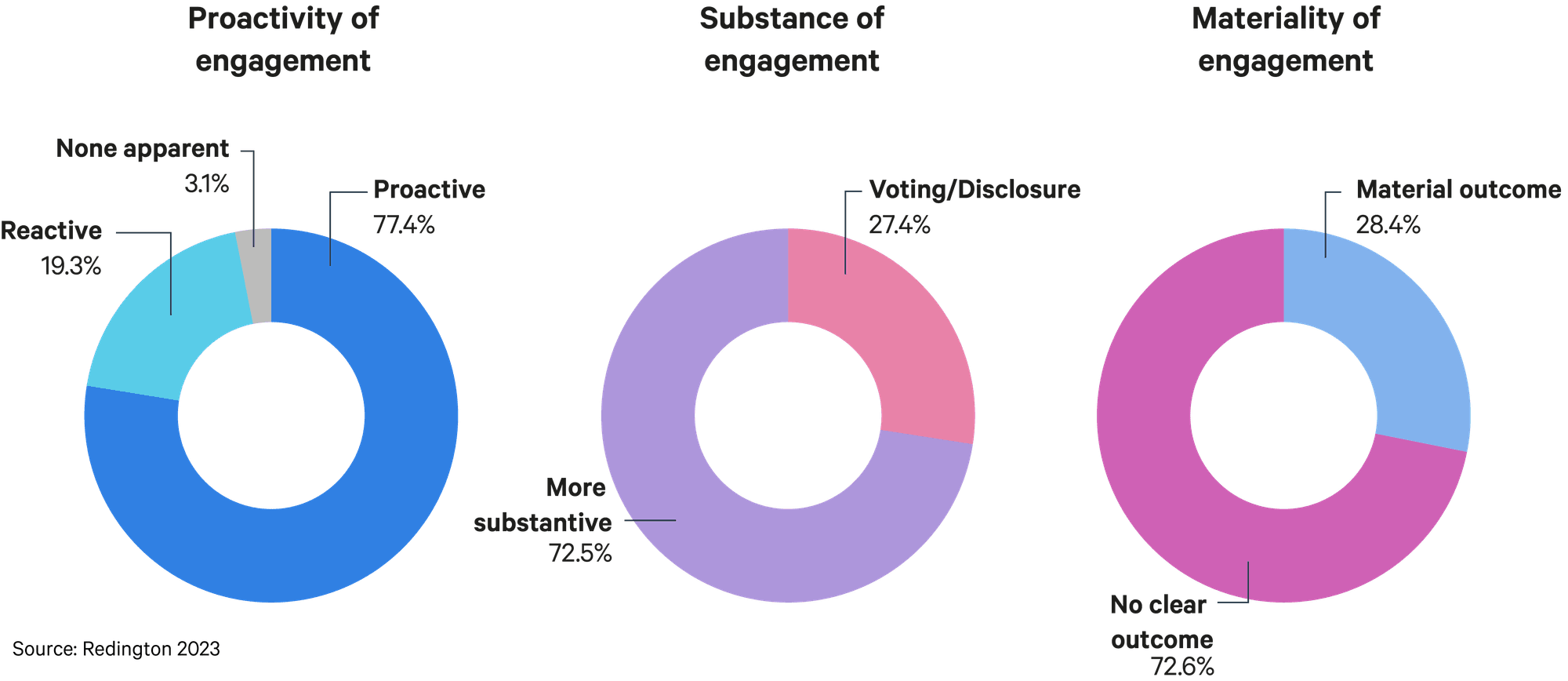

For the second year running we analysed how investment managers reported against the Stewardship Code, sharing our findings in our annual report. Whilst it was encouraging to see positive change in some areas of disclosure since last year, there is more to be done.

With the key message from last year’s report being “it’s not just a numbers game”, this year we shone a light on engagement quality by assessing case study materiality. It was of great concern to us that the majority of case studies disclosed by managers did not appear to us to be delivering material outcomes. We will continue to use this analysis as part of our wider efforts to assess investment manager stewardship and press them for improvements where necessary.

We recognise that in many areas we can be more effective and deliver more for our clients by working collaboratively with others. We also know that many sustainability issues can only effectively be addressed through broad industry-wide and/or policy approaches that reflect the systemic nature of the issues.

We are therefore active in working with other investment consultants – and other participants in the investment chain – and in actively engaging on public policy and best practice developments. We maintain strong networks across the investment industry and often work with peers to promote consistent responses to consultations on those frequent occasions when our perspectives coincide.

Redington was instrumental in the creation of the two collaborative bodies in the investment consultant community, the Investment Consultants’ Sustainability Working Group (ICSWG) and the Net-Zero Investment Consultants Initiative (NZICI – our industry’s contribution to the Glasgow Financial Alliance for Net-Zero, GFANZ) and remains represented on each group’s steering committee. During the year, we have worked as part of ICSWG to update and enhance some of its existing guidance, and we continue discussions at NZICI to move beyond it being simply a group reporting against delivery of its stated commitments.

Two highlights of our public policy and best practice work this year have been on the Taskforce on Social Factors, outlined in the below case study, and the Financial Markets Law Committee’s (FMLC) fiduciary duty working group. The FMLC was invited by the UK government to take forward a project making clear how addressing climate change is entirely consistent with trustees’ fiduciary duties to their beneficiaries. We believe that we were invited to join the working group because of our prior work in the area (we included a case study regarding fiduciary duty and green bonds in last year’s report). We provided detailed input throughout the development of the guidance, and actively participated in roundtable discussions. As at the year end, the publication of the FMLC guidance is pending. We are hopeful that it will be positively influential.

We discuss our latest Sustainable Investment Survey and our second annual Stewardship Code reporting analysis elsewhere in this report. We continue to regard each as an important contribution to increasing visibility of stewardship and sustainability quality and delivery by the investment management community – and so also therefore to encouraging enhanced performance over time.

We provided the ICSWG’s representative for the TSF, meaning we were the sole investment consultant on the steering group of the Taskforce.

We played a part in robust discussions about the development of the guide issued for consultation in October 2023, helping shape the style and quality of the output. We also took a leading role in a number of areas of drafting of the guidance. In particular, we had key responsibility for the creation of the appendix of potential questions to ask fund managers (and investment consultants!) to challenge them on their knowledge and experience of, and delivery with respect to, social factors. This appendix covers both investment integration and stewardship and considers both the RFP and ongoing monitoring stages of a relationship. It also considers investment managers’ own due diligence of clients, and of wider human rights exposures that they face.

We look forward to updating and finalising the guide further to the responses to the consultation, which closed shortly before the end of 2023. And we look forward to the final guide assisting investors to pay more attention to social factors in their investment approaches.

Overall, we’re active participants in the following groups:

Diversity Project – the industry-wide group promoting diversity across all dimensions in the investment industry. We are active participants in a wide range of workstreams, supporting the development of best practices.

Financial Markets Law Committee’s fiduciary duty working group – FMLC was asked by the government to take forward a project making clear that addressing climate change is consistent with fiduciary duty. See discussion in main text above.

Glasgow Financial Alliance for Net Zero (GFANZ) Sectoral Decarbonisation Working Group – we’re members of this group, which aims to develop guidance to support financial institutions’ use of sectoral pathways in the creation of net-zero transition plans, alignment of portfolios, and engagement with real-economy firms, consistent with climate science to achieve 1.5°C targets.

Institutional Investors Group on Climate Change (IIGCC) – as members of this group representing investors that consider the implications of climate change in their investment approaches, we’ve actively participated in the development of IIGCC best practice guidance. We’re also members of the associated Paris Aligned Investment Initiative’s Net-Zero Technical Working Group.

Investment Consultants’ Sustainability Working Group (ICSWG) – we were a founder of this initiative, focused on sharing best practice and raising standards across investment consultants and the investment industry as a whole. We remain represented on the steering committee.

LGPS Scheme Advisory Board – Responsible Investment Advisory Group, supporting local authority funds and pools in responding to developments, with a particular focus on the forthcoming TCFD reporting requirements.

Net-Zero Investment Consultants Initiative (NZICI) – investment consulting’s contribution to the broader Glasgow Financial Alliance for Net-Zero, the finance industry’s commitment to net-zero. We and a dozen other consulting firms have undertaken to deliver net-zero in our own businesses but more significantly through our advice. We sit on its steering committee.

Taskforce on Social Factors – a group fostered by government departments working to assist pension funds to think through the challenge of the S in ESG, and how to respond effectively. We are the sole investment consultant sitting on the steering committee. See case study.

Among other groups we’re also members of:

Pensions and Lifetime Savings Association (PLSA)

the International Corporate Governance Network (ICGN)

UN-supported Principles for Responsible Investment (PRI)

We actively respond to relevant public consultations on policy matters. As a service provided to clients at their request, we will also support their responses to consultations that they deem relevant. In addition, Redington colleagues are active participants in a number of industry representative committees and other groups that respond to some consultations (including at CFA UK, the Corporate Reporting Users’ Forum and ICSWG), on which we also seek to have influence to ensure that the broader voice of the investment community is heard on relevant issues.

Among the consultations and initiatives we responded to in 2023 were:

FCA (Financial Conduct Authority) Consultation on Sustainability Disclosure Requirements (SDR) and investment labels (January 2023)

AMNT (Association of Member Nominated Trustees) Survey on the Impact of a 4C World (February 2023)

FCA (Financial Conduct Authority), DWP (Department of Work and Pensions), TPR (The Pensions Regulator) Consultation on Value for Money (March 2023)

TNFD (Taskforce on Nature-related Financial Disclosures) v0.4 Beta Framework Consultation (June 2023)

ISSB (International Sustainability Standards Board) Sustainability Account Standards Board (SASB) Consultation (July 2023)

ISSB (International Sustainability Standards Board) Consultation on Agenda Priorities (August 2023)

VRG (Vote Reporting Group) Consultation (September 2023)

ICMA (International Capital Market Association) and IRSG (International Regulatory Strategy Group) Consultation on Draft Code of Conduct for ESG Ratings and Data Product Providers (October 2023)

TPT (Transition Plan Taskforce) Asset Owner Consultation (December 2023)

FCA (Financial Conduct Authority) Consultation on Diversity and Inclusion in the Financial Sector (December 2023)

We must consistently evolve the way we advise our clients to help them navigate the new and emerging challenges they face. This is true for all of the advice we provide, but in particular when it comes to the sustainability risks our clients are exposed to.

Deepening our research process: We will be expanding our coverage of impact and sustainable solutions our clients can invest in. This will include a wider array of nature-based solutions, social and affordable housing, and health-based investments. We will also be refreshing our ESG Integration and Stewardship assessment process and output to account for our increased expectations of the fund managers we research and rate.

Evolving our approach to risk management: 2023 was the hottest year on record.1 There is a growing scientific consensus that our proximity to, and the impact of material physical climate risks has been understated. We will refresh how we advise our clients to measure, mitigate, and potentially hedge exposure to climate risk, alongside greater emphasis of measuring and reducing our clients' real-world impact on the environment.

Tightening our monitoring and oversight: we will widen the aperture of data points we use to oversee the delivery of stewardship and engagement by the managers our clients invest with. We will scrutinise systems-level engagement, policy advocacy, corporate lobbying, and industry affiliations to build a holistic view of whether the actions of the fund managers are aligned with the requirements of our clients.

These specific initiatives complement the work we began last year to fully integrate nature-related risks into our investment advice, aligning our default client advice with net zero, and continue to build our stewardship platform allowing clients to fully scrutinise the actions of their fund managers.

1 NASA, 2023 NASA Analysis Confirms 2023 as Warmest Year on Record - NASA