WHAT WE DELIVER IN STEWARDSHIP AND SUSTAINABILITY

Jump to a section or flip the page to continue reading.

THROUGH OUR INVESTMENT CONSULTING

THROUGH OUR MANAGER RESEARCH

THROUGH INDUSTRY AND POLICY ENGAGEMENT

LOOKING TO THE FUTURE

We take a framework-based approach to helping our clients make difficult decisions effectively. Among our guiding principles are to focus on decisions that’ll make a real difference and to keep the end objective in mind.

We provide clear and unbiased advice – and we’re not shy of taking bold stances on particular issues. We welcome the constant challenge from our clients to advance our offering and enhance the delivery of all our services, including sustainability and stewardship.

Our clients, alongside other asset owners, faced a number of challenges in 2022. Among these for UK pension schemes was the gilts crisis in Q3. Our investment consultants worked closely with clients throughout this time, helping to protect them from the worst impacts of this market disruption. At the end of this crisis, many clients found themselves nearer to funding maturity but with the need to rebalance their portfolios and consider fundamental asset allocation changes. This upheaval somewhat diverted attention from sustainable investment matters for some clients, especially in Q4. However, despite these challenges, during 2022, we worked on sustainable investment topics with all of our clients in different forms and capacities. With limited time on agendas, we remained focused on the sustainable investment matters most material and important to our clients.

The majority of our work over the year focused on two areas: climate change and TCFD reporting, and stewardship.

In particular, we helped a number of clients with their Task Force on Climate-related Financial Disclosures (TCFD) reporting. Among these were our Master Trust and DB pension clients with assets over £5bn, who were required to implement TCFD reports per the DWP’s Occupational Pension Schemes (Climate Change Governance and Reporting) Regulations 2021.

Our work included providing our clients with comprehensive training on climate change in an investment context and helping them establish a suitable climate governance process, understand climate metrics and scenario analysis and how stewardship can be a used as an effective lever to meet climate-related objectives. Our framework-based approach focuses on helping our clients adopt efficient processes tailored to their specific structures, integrate climate stress tests into strategic decision-making and select and monitor the most suitable climate-related metrics and target(s) for their circumstances, including time horizons.

In 2021, we committed to aligning our default client advice with net zero. In 2022, we helped many clients set specific net zero and other decarbonisation objectives, with advice tailored to each client and focused on what moves the dial for their particular scheme.

Also tailorable is our regular reporting to clients on climate-related matters, which provides regular insight (either annually or quarterly) into the key emissions and alignment of their portfolios and relevant comparatives. Our reports are designed to provide valuable insights to aid decision-making on climate matters.

TCFD CLIMATE METRICS REVIEW

The following table provides insight into the extent to which we’ve provided climate-related advice to clients, helped them establish metrics and targets and assisted them in advancing the decarbonisation of their portfolios:

Total clients

Trained on climate change

Completed TCFD governance element

Received carbon emissions data

Completed TCFD reporting

Invested in climate solutions

>£5B

12

12 (100%)

10 (83%)

7 (58%)

6 (50%)

£1-5B

24

24 (100%)

19 (86%)

13 (54%)

0 (0%)

6 (25%)

<£1B

17

12 (71%)

1 (6%)

Defined Contribution

9

5 (56%)

N/A

Source: Redington. 2022

We’ve undertaken to continue to publish this table over time to provide insight into the practical outcomes of our advice on climate risks.

We’ve identified stewardship as a key challenge for our clients and have developed processes and technology to hold fund managers accountable for delivering positive stewardship outcomes. We’ve implemented new tools via our proprietary software platform, Ada Fintech, allowing clients to make sense of manager voting activity, and delivered bespoke reports to clients that highlight the votes that matter to them. This helps our clients improve their stewardship activity ahead of the DWP’s recent moves to raise their stewardship expectations of pension schemes.

We frame our approach to stewardship through three key elements: report, assess and engage. We provide tools and advice that enable our clients to understand and make sense of what is being done on their behalf (report), consider whether that is good enough and identify any areas of particular weakness (assess); and challenge and press managers to deliver more (engage).

We provide each element independently or as a bundle, depending on our clients’ specific needs. Overall, our stewardship services respond to two distinct needs among our asset owner clients:

To have insightful material for their own reporting needs (including Implementation Statements, Stewardship Code responses, and/or other public disclosures of stewardship);

To hold their fund managers accountable and call for more from them, ensuring that asset owners can play their role in delivering good stewardship.

Our sustainability work with clients extends beyond these two key areas. Our broader work in sustainable investment includes among other things developing clarity on their sustainable investment beliefs, detailed advice on investment approaches that can effectively reflect their sustainability ambitions, assessing the appropriateness of relevant service providers, and helping our clients identify relevant responsible investment bodies to join. The two case studies highlight some particularly in-depth work on climate and stewardship we’ve conducted for specific clients.

Within stewardship, one of our areas of focus in 2022 has been voting. During the year, we developed a tool that allows our clients to analyse their managers’ voting behaviour and turn that weight of data into decision-useful information. The tool allows our clients to identify the votes that most matter to them, based on their exposure and relevance to their specific focus themes. We also launched the Most Significant Votes blog, aggregating news on key votes across the different voting seasons, recognising that there were limited channels through which our clients were receiving this information from their other service providers.

OUTCOME: This output gives trustees and other asset owner representatives an insight into key votes on which they might choose to challenge their fund managers – and urge improvements if their approaches seem weak.

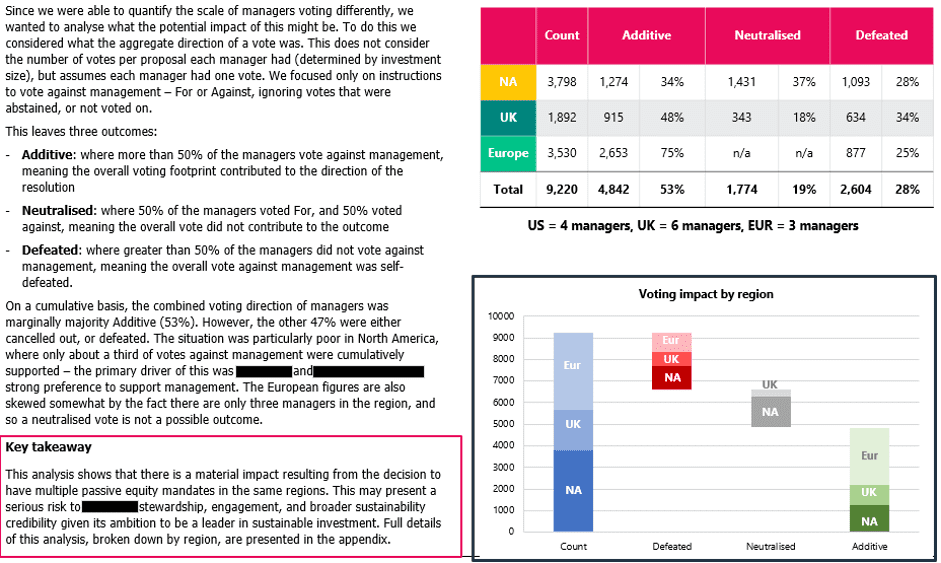

We worked with a large UK asset owner to provide analysis and advice regarding their approach to voting on equity investments.

Our client had multiple segregated equity mandates split across six different fund managers in three regions, generating concerns over the net impact that votes were having. We found inconsistent voting across the fund managers – only 53% were adding weight to each other, with the remaining cancelling each other out or voting in contrary ways. The primary source of this inconsistency was the client’s outsourced voting model and the large number of fund managers in each region.

We spent three months working closely with the stewardship lead of the asset owner, analysing different voting models against regulatory requirements, global best practice, peer group comparisons and capacity to overcome inconsistent voting. Based on insights from this analysis, we recommended insourcing the client’s voting activity and proposed a roadmap for implementing change over time in the most effective way.

OUTCOME: The client is still in the implementation stage but has adopted the core of our proposed solution. Through enacting the recommendations of our advice, the client is on their way to maximising their ability to make a positive impact through voting and wider engagement with the underlying companies in which their fund managers invest. Once fully implemented, this model will allow the client to have greater control over voting outcomes, resulting in consistency in the client’s voting across different fund managers and shareholder resolutions, including ones focused on key ESG topics.

The impact of managers voting differently

We advised a large local authority pension scheme on a suitable and ambitious interim climate target for its largest active global equity fund.

Through a period of months working closely with a specially created subcommittee of the trustees, we assessed the trustee’s initial climate targets for their active global equity fund. We explored different steps that could be taken to raise the ambition of the target.

We designed a framework to help our client interrogate a series of options and, using the framework, we suggested a self-decarbonisation target that was more ambitious than the existing target. We mapped the scheme’s allocation to relevant sectoral decarbonisation pathways to determine the most appropriate emissions-based metric for the client. Recognising the challenges and limitations of using backward-looking emissions metrics in isolation, we also recommended adopting a forward-looking climate target to measure how the fund contributes to real-world decarbonisation. We suggested adopting an Implied Temperature Rise secondary goal, allowing the client to measure the progress made towards portfolio-alignment and engagement targets.

OUTCOME: The client adopted an interim emissions reduction target alongside an Implied Temperature Rise goal to maintain a portfolio consistent with the Paris Agreement.

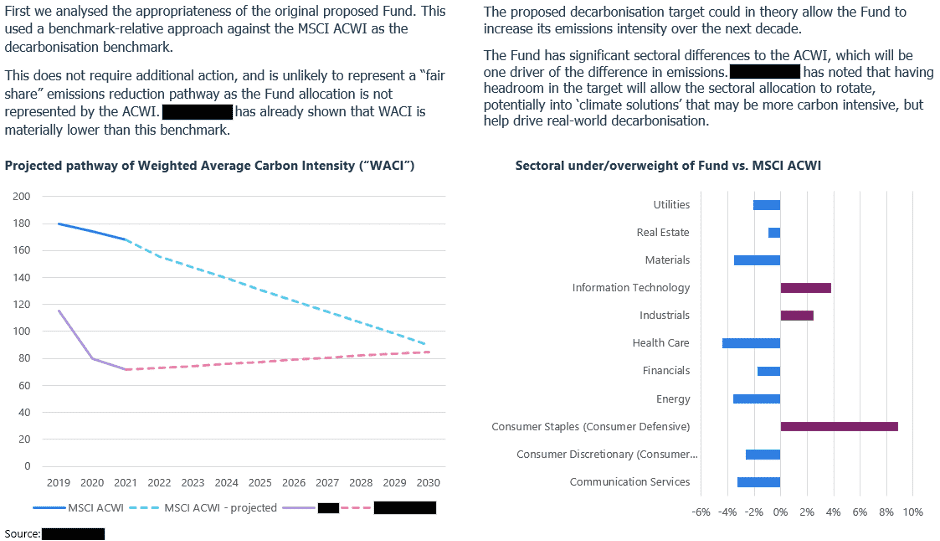

Is the ACWI an appropriate decarbonisation benchmark?

We believe that to be good investment consultants, we must communicate with our clients clearly and proactively. During periods of market turmoil, such as the gilts crisis of Autumn 2022, we make sure to keep our clients aware of what’s going on and what they need to focus on. We also produce several periodic communications, listed in the appendix. It’s the responsibility of our Investment Consulting team, in conjunction with Marketing colleagues, to assess how effective these communications are and to enhance them over time to ensure we deliver the right messages, at the right time. We regularly review our correspondence with clients to ensure we don’t over-communicate.

From a manager research perspective, in 2021 we focused on introducing new assessment frameworks to hold fund managers to account on ESG integration, stewardship, culture, and inclusion and diversity. In 2022 we focused on the effective roll out of these new frameworks across our Manager Research team.

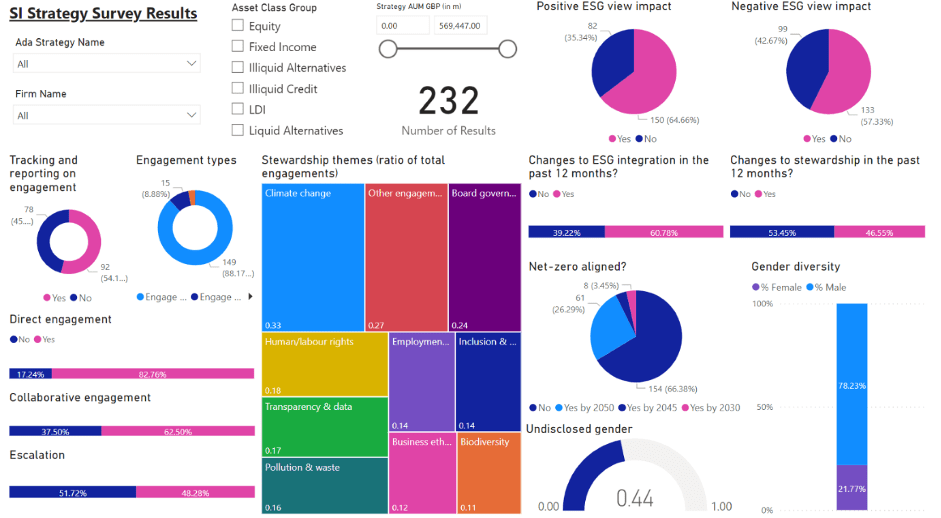

Since ‘ESG & Stewardship’ is one of our core manager selection factors, ESG has long been a key agenda item when we speak with new fund managers or ones we already research and monitor. However, to aid our team’s research process and ESG evaluations, this year, we built ESG dashboards which pull in data from our annual Sustainable Investment Survey. This enables our team more readily review insights related to ESG integration, stewardship, climate, and inclusion and diversity for over 230 strategies and 120 fund managers.

Data is updated annually (in line with our survey), and we encourage our Manager Research team to consider these dashboards when making fund manager evaluations across asset classes. We also use these dashboards to challenge fund managers when they lag in comparison to peers.

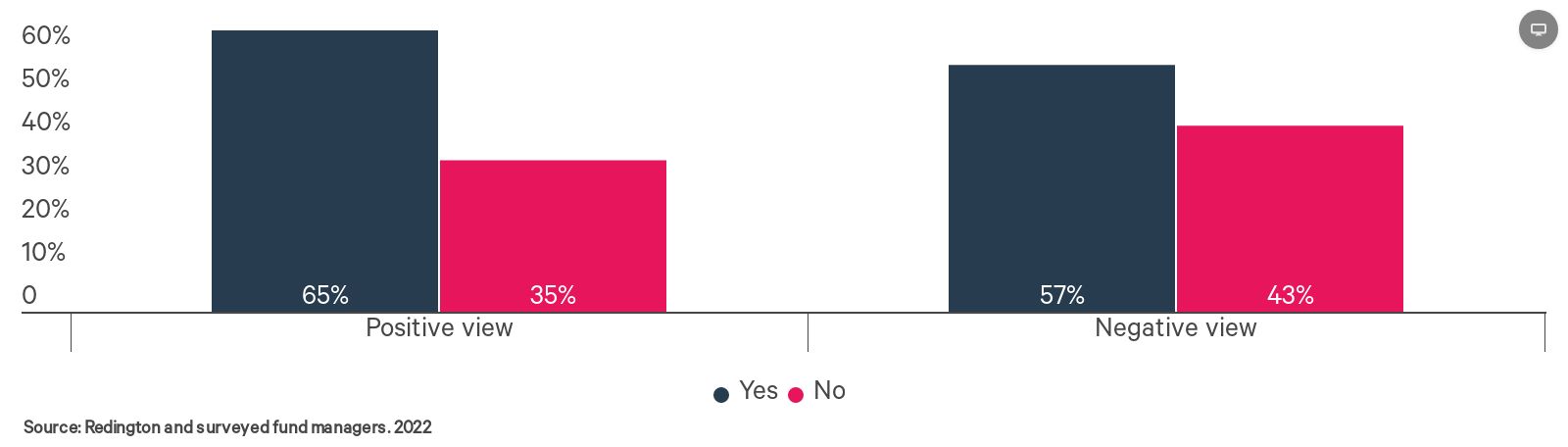

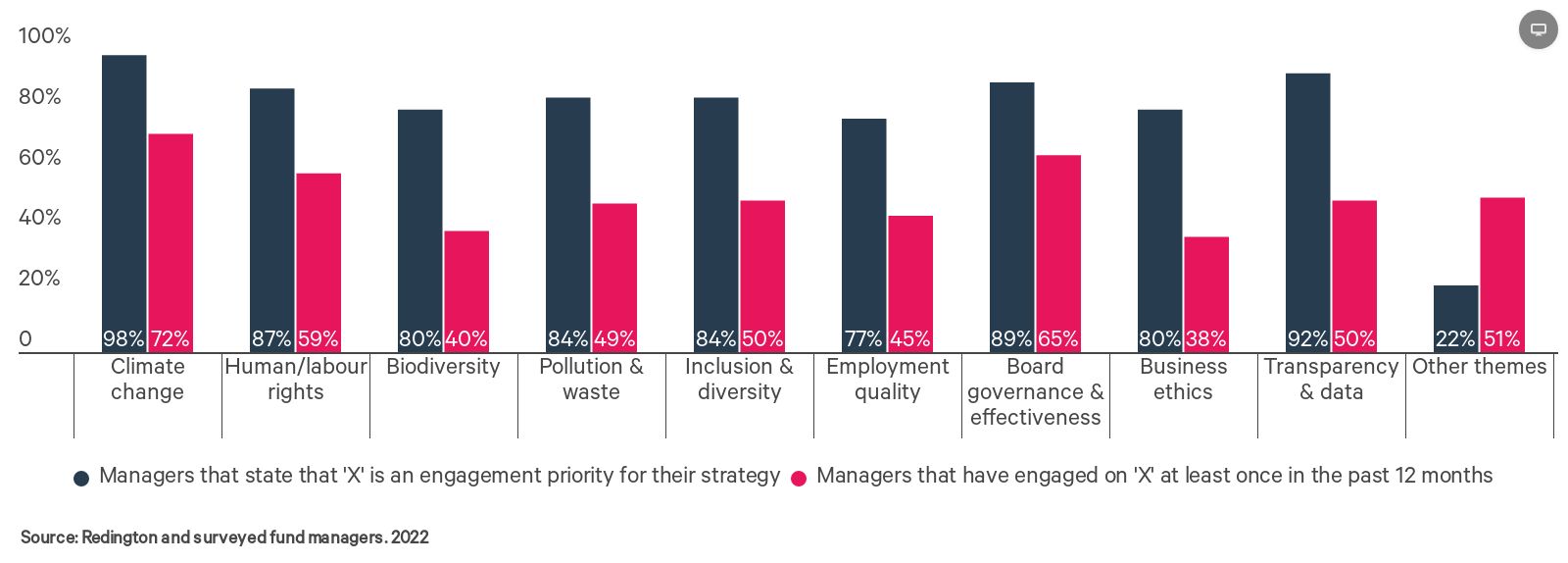

Our 2022 Sustainable Investment Survey again provided a powerful moment for us in gaining real insights into the approach of fund managers to ESG matters. We took the opportunity to reflect what we’d learnt to both the fund managers and asset owners. We expressed disappointment about the continued failure of the industry to evidence properly their delivery of ESG in practice, in particular:

A failure to provide clear examples of buy and/or sell decisions that were driven by ESG criteria; and

A failure to deliver concrete engagement even on issues that fund managers state as their priorities.

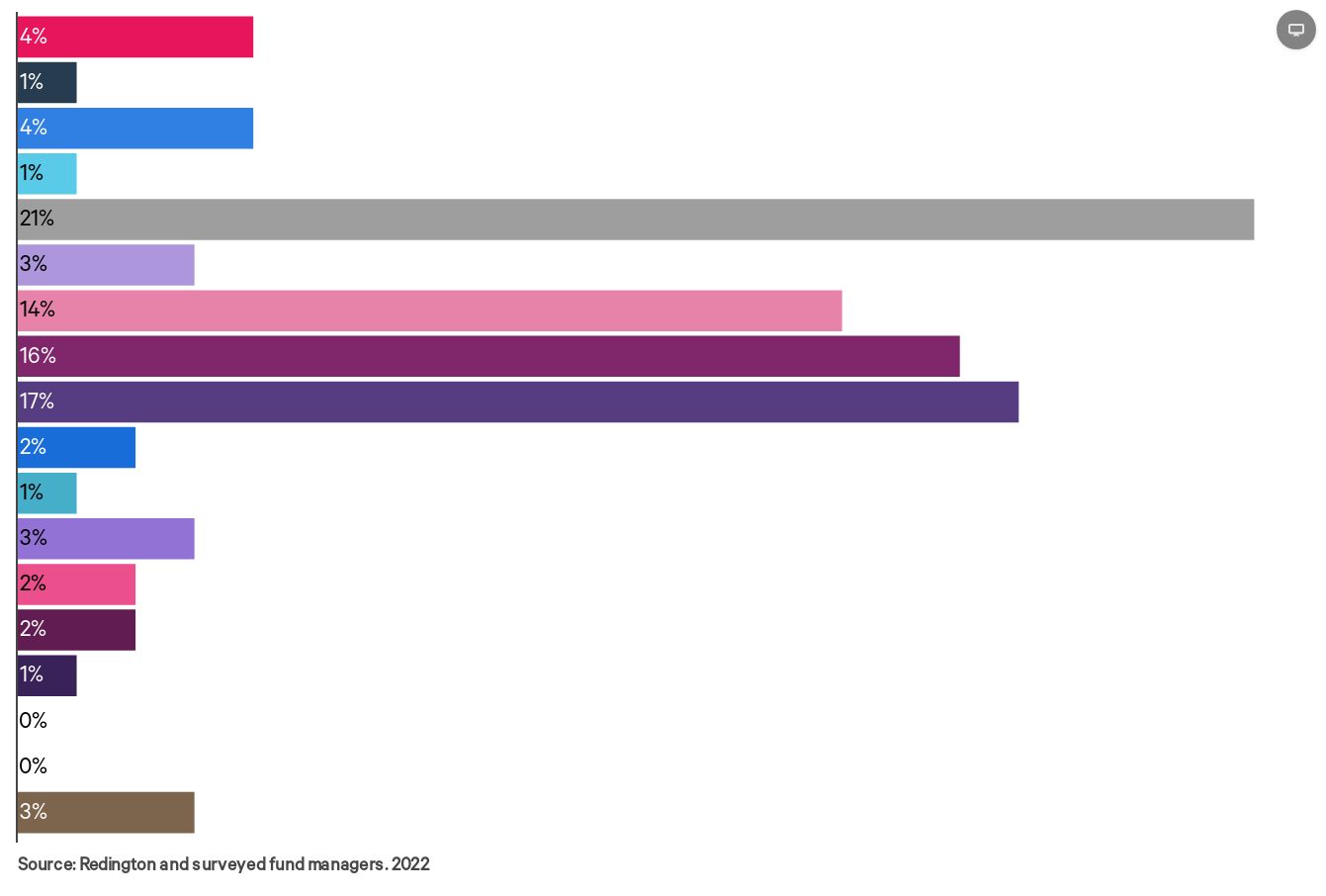

CAN YOU PROVIDE AN EXAMPLE OF A NEGATIVE/POSITIVE ESG VIEW THAT LED TO DECREASED/INCREASED EXPOSURE IN THE LAST 12 MONTHS?

WHAT MANAGERS SAY VS. WHAT THEY DO

(of those managers that approach, track and report on stewardship at the strategy level)

This year, we also asked questions regarding the defence sector arising from Russia’s invasion of Ukraine. We recognised this as a major systemic event and sought some additional transparency on how fund managers are considering and responding to the relevant risks. Through these questions, and a standalone blog on the issue, we’re encouraging fund managers to learn from the events of 2022, both in respect of their approach to managing and mitigating geopolitical risks, and their exclusion policies in ESG products.

We recently provided a client with more in-depth ESG and stewardship reporting across its key fund managers, in the form of an annual set of slides on each fund manager. They were seeking to better understand the approaches of their fund managers and potential areas for improvement so that they could hold their fund managers to account in line with their duties as a responsible asset owner.

We utilised our data infrastructure to review information on the fund managers at scale related to ESG integration, stewardship activities, inclusion and diversity, climate risk and industry affiliations. In each case, we sought to use data points that didn’t just cover issues on a superficial level, but that delved beneath the surface.

This process also provided an opportunity for challenge and engagement with the fund managers in question. For example, we tested one sustainability-focused fund manager on why they had responded ‘No’ to our survey on whether their remuneration policy considers ESG risks and opportunities. We were able to clarify the true situation, gaining confirmation and evidence about how ESG risks and opportunities are considered in pay structures, and update our dataset accordingly to ensure an accurate representation of the fund manager.

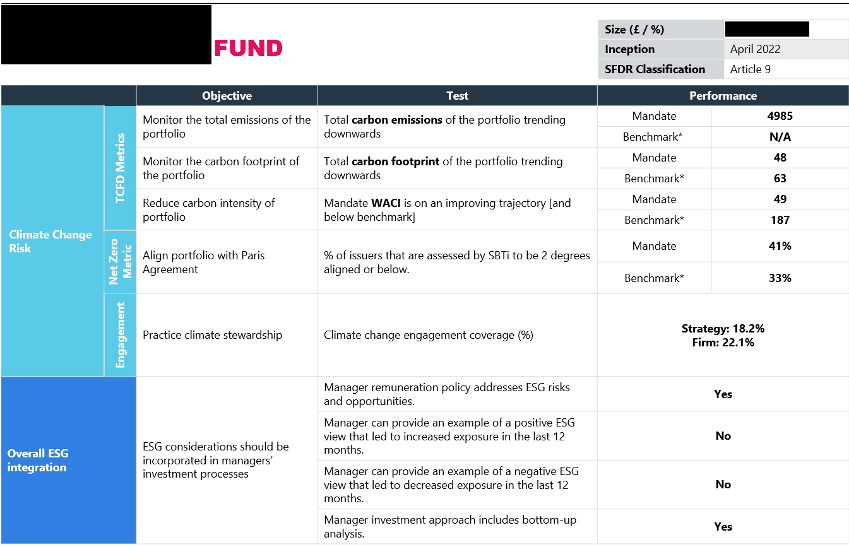

OUTCOME: We produced a decision-useful enhanced ESG report covering ESG integration, stewardship statistics and climate metrics across the client’s key fund managers – complete with our views on their fund managers’ approaches relative to peers. This provided our client with the tools and insights necessary for engaging with their fund managers, holding them to account on material topics. The screenshot shows a sample page from our ESG report.

We recognise our privileged position as gatekeepers between fund managers and asset owners, and the influence we have on institutional capital through our advice.

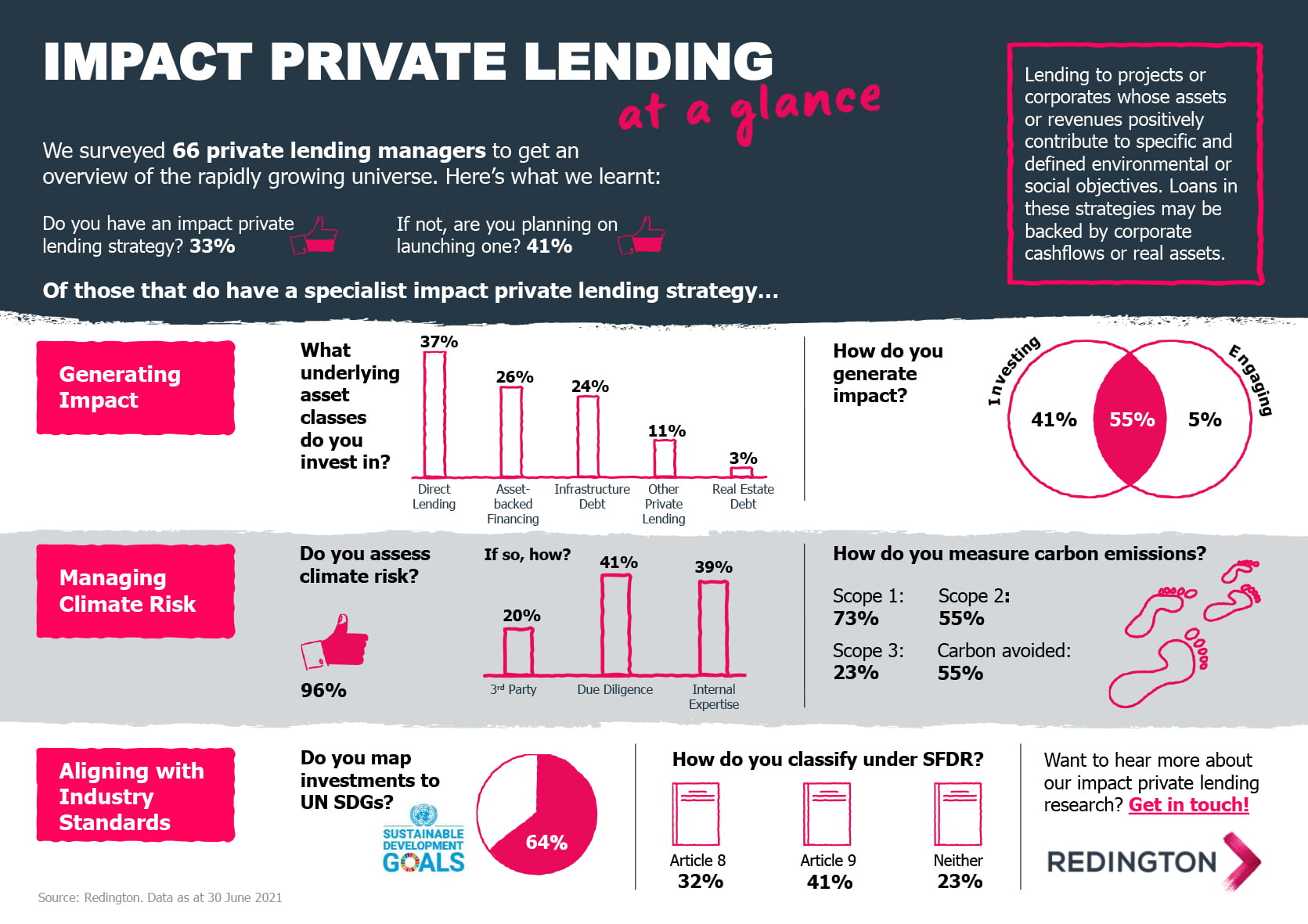

Currently, investor commitments to impact funds are slow compared to the rapid proliferation of impact-related products. In our interactions with asset owners, there seems to be some apprehension regarding impact strategies due to perceived risks and limited awareness of impact options outside of private equity. However, it’s evident that in order to achieve a net-zero future or make meaningful contributions towards the SDGs, private institutional capital is required to drive positive change.

As a result, we researched impact options within private credit because we believe that this offers investors an untapped opportunity to invest in positive real-world impact alongside attractive risk-adjusted returns. The aim of our research was to dispel misconceptions around the relationship between impact, returns and risk, present investors with credible impact private credit investment products and provide a compelling case for the mobilisation of institutional capital towards these impact solutions.

Surveying a broad universe of private credit fund managers to understand the products currently available;

Conducting several investment and impact due diligence meetings with fund managers;

Analysing track records, deal pipelines and other available data; and

Engaging with the Investment Consulting team to understand client priorities to guide research.

OUTCOME: We took our impact private credit research to our Investment Strategy Committee and presented the market and asset class context and proposed a ‘Preferred’ rating for two fund managers in which we have high conviction. The research was well-received and approved by the Committee in March 2022. Following this, we’ve presented the asset class to several clients – and to the fund managers in question.

In addition to our regular monitoring meetings and requests for information from fund managers, we stay on top of news flow and notable fund manager events (e.g. team departures, changes in ownership, etc.) to ensure we hold fund managers fully to account on an ongoing basis.

In 2022, one of our rated fund managers was under scrutiny in the mainstream media for the practices of one of its private equity-held companies. The company in question was in the healthcare industry, and a small portion of its business included managing care homes for people with intellectual or developmental disabilities.

The article claimed poor living conditions for patients and an undersupply of staff relative to patient needs.

Soon after the article was published, we arranged a meeting with the fund manager to discuss the article, their response and any remediation efforts undertaken. Whilst we don’t have any direct exposure to this asset, we believed it was important to engage with the fund manager on this topic to understand any implications or learnings for other healthcare companies in their funds.

OUTCOME: The fund manager was very transparent in discussions with us and provided useful context about the investment and the article in question. They set out a clear plan for improvements to staffing, client care and records. We also discussed hiring an independent consultant to assess the allegations and provide recommendations to the Board. Overall, whilst some of the events described in the article were tragic, we didn’t believe there to be a systemic issue within the fund manager regarding the provision of healthcare services. We were comfortable with their due diligence process in acquiring the asset and the remediation efforts undertaken following the news event. We continue to monitor the fund manager regularly.

During the year, a fund manager to which many of our clients have entrusted money revealed that the outcomes of its vote decisions would look very different over 2022 when compared with its statistics from 2021. The fund manager indicated that this was driven by external changes rather than a change in its own approach. Through formal and informal dialogue with its staff, and through a close analysis of the fund manager’s public reporting of its activities, we reached a clear conclusion that the change being made was in fact rather less about the external changes and much more a deliberate decision by the manager to shift its approach – and that this indicated that there was likely to have been a change across stewardship more broadly, not just voting. We shared a brief paper setting out this analysis and our view with relevant and interested clients.

OUTCOME: We know that some of our clients had active dialogue with the fund manager, and used our analysis as the basis for challenging the change in approach. We know that at least two clients reached the conclusion that they needed to change their intended relationships with the fund manager as a result.

At the end of the year, we published our first analysis of investment manager reporting against the Stewardship Code – an analysis we aim to produce annually. We revealed a notable range in approaches to definitions of the engagement that fund managers report on – which means that careful assessment is required. Fund managers seem to be tempted to report the largest number of actions possible, which we believe is unhelpful – stewardship should be about quality rather than just quantity – hence the overall message of our report that it’s not just a numbers game.

We engage on policy matters to help solve market-wide issues that we identify as significant and systemic. We recognise that by working together with our clients, we can have an outsized impact on the evolution of sustainable finance. We work closely with our clients to assist them in their thinking about such systemic issues and to engage on policy matters as appropriate.

Having been a co-founder of the Investment Consultants Sustainability Working Group (ICSWG) in 2020, we continue to use this as our principal vehicle for collaboration with our peers and for influencing policy and regulation as appropriate. We sit on the ICSWG steering group and the Net-Zero Investment Consultants’ Initiative (NZICI) and are strong supporters of both organisations – recognising their role in expecting more from our profession as well as in influencing the marketplace.

Recognising the systemic importance of rising inequalities and other social issues, which have so far been poorly identified and reflected by institutional investors, we welcomed the opportunity to join the Taskforce on Social Factors (TSF) as the ICSWG’s representative on the TSF’s steering group. The TSF was established by the Department for Work and Pensions, in collaboration with other arms of government and regulators, to assist pension schemes in thinking more actively about the ‘S’ in ESG. We look forward to delivering a report in 2023 that provides guidance and support to trustees in approaching these issues.

During the year, we participated in a range of discussions regarding fiduciary duty, with the aim of aiding the understanding of practical constraints to pension scheme sustainable investment actions arising from current interpretations of fiduciary duty. We discuss one particular set of activities in the case study.

We continue to regard our Sustainable Investment Survey as a key contribution to engaging with our industry for collective benefit. The 2022 report was based on the responses to our survey from 122 global fund managers representing over £37 trillion in combined assets under management. We urged fund managers to deliver more action across sustainability issues, highlighting our message through a public webinar and broader media activity.

This year we also published our first analysis of fund manager stewardship reporting (their responses to the UK Stewardship Code). We noted a tendency to inflate the number of activities and highlighted ways in which the best reports reveal the quality of stewardship activity rather than fixating on quantitative measures. Often, we were more impressed by the reporting from managers who downplayed their numbers overall but demonstrated the delivery of tangible outcomes. It’s not just a numbers game.

We actively respond to public consultations ourselves, collaboratively with other members of the ICSWG and by supporting clients to submit their own responses. Through individual members of our team sitting on industry committees, we also ensure broader-based finance sector involvement in policy developments. Similarly, we actively participate in the development of industry best practices.

DWP Consultation on Climate and Investment Reporting (January 2022)

IIGCC Consultation on Net Zero Investment Framework for Private Equity (February 2022)

TNFD (Taskforce on Nature-related Financial Disclosures) Beta Framework (June 2022)

US SEC (Securities and Exchange Commission) Climate-related Disclosure Standard (June 2022)

ISSB (International Sustainability Standards Board) S1 (Framework) Consultation (June 2022)

ISSB (International Sustainability Standards Board) S2 (Climate) Consultation (June 2022)

GFANZ (Glasgow Financial Alliance for Net Zero) Portfolio Alignment (September 2022)

GFANZ (Glasgow Financial Alliance for Net Zero) Sectoral Decarbonisation (September 2022)

DWP (Department for Work & Pensions) Funding and Investment Strategy (October 2022)

LGPS (Local Government Pension Scheme) Proposals for Governance and Reporting of Climate Change Risks (November 2022)

Glasgow Financial Alliance for Net Zero (GFANZ) Sectoral Decarbonisation Working Group – we’re members of this group, which aims to develop guidance to support financial institutions’ use of sectoral pathways in the creation of net-zero transition plans, alignment of portfolios and engagement with real-economy firms, consistent with climate science to achieve 1.5°C targets. To help shape this work, during 2022, the group met with companies from three highly-exposed sectors – airlines, oil and gas, and steel – to discuss detailed realistic pathways for their industries.

Institutional Investors Group on Climate Change (IIGCC) – as members of this group representing investors that consider the implications of climate change in their investment approaches, we’ve actively participated in the development of IIGCC best practice guidance. We’re also members of the associated Paris Aligned Investment Initiative’s Net-Zero Technical Working Group.

Investment Consultants’ Sustainability Working Group (ICSWG) – we were a co-founder of this initiative, focused on sharing best practices and raising standards across investment consultants and the investment industry as a whole. We remain represented on the steering committee.

LGPS Scheme Advisory Board – Responsible Investment Advisory Group – supporting local authority funds and pools in responding to developments, with a particular focus on the forthcoming TCFD reporting requirements.

Net-Zero Investment Consultants Initiative (NZICI) – created in 2021, NZICI is investment consulting’s contribution to the broader Glasgow Financial Alliance for Net-Zero, the finance industry’s commitment to net zero. We and a dozen other consulting firms have undertaken to deliver net zero in our own businesses but more significantly through our advice. We sit on its steering committee.

Pensions for Purpose – a collaboration of pension funds, fund managers, investment consultants and social enterprises, whose aim is to promote understanding of impact investment-related issues. We sit on its advisory group.

Taskforce on Social Factors – a group fostered by government departments working to assist pension funds to think through the challenge of the ‘S’ in ESG and how to respond effectively. We’re the sole investment consultant on the steering committee and an active participant in the working group on making the case for social issues and setting out the relevant roles within the investment chain.

Pensions and Lifetime Savings Association (PLSA)

the International Corporate Governance Network (ICGN)

UN-supported Principles for Responsible Investment (PRI)

At the end of 2021, at the invitation of the Impact Investing Institute, we took part in a roundtable to discuss issues of fiduciary duty. We brought a practitioner perspective to a discussion predominantly between lawyers, academics and industry bodies. Early in 2022 we followed up on our comments in writing with a short paper outlining the limits set by fiduciary duty on pension scheme trustees choosing to invest in green gilts – according to most legal advice. Noting that this appears to run contrary to the policy intent in creating green gilts, and the net-zero ambitions of both the UK government and many pension schemes, we also articulated ways to address these limits. After some minor changes to the document based on input from other members of the roundtable, we understand that the Institute has used our paper in a range of lobbying efforts.

OUTCOME: The public policy discussion about green gilts continues, and we continue to engage with it.

Our biggest value-add – to our clients, our stakeholders and the wider communities we come from and serve – remains our progressive yet pragmatic approach to sustainable investing. We’re data- and goal-driven problem-solvers in a world where neither data nor goals are standardised. This is challenging, but being well-informed, disciplined and forward-thinking in setting objectives and strategy means fewer revisions later.

Focus on joining the dots for clients through our refreshed sustainable investment training. What’s happening in the science? Does protecting biodiversity and land fit into net-zero targets, and if so, how? What are scope 3, 4 and 5 emissions, and are they important to your portfolio’s climate risk and opportunities?;

Update our tools and metrics to reflect our best thinking on climate and more, which includes updated scenario analysis, more emphasis on sustainability risks and forward-looking metrics and access to modelling around biodiversity strategies and investments. We’ll start to advise clients on nature-positive net-zero investments; and

Facilitate asset owners in reporting and in holding fund managers to account for effective delivery of engagement and voting. We’ll do this by continuing to shine a spotlight on the most significant lever for investor action across all asset classes – effective stewardship and engagement. Stewardship is applicable across all asset classes, and in 2023, we’ll be rolling out Redington’s Enhanced Stewardship Platform (ESP) to clients. This will help them to understand and make sense of what’s being done of their behalf (report), consider whether that’s good enough and identify any areas of weakness (assess), and challenge and press fund managers to deliver more (engage).

This year, as we continue to build out the seven-person, cross-functional Sustainable Investment team at Redington, we do so to honour our commitment to aligning our default client advice with net zero, helping our clients manage their money for success – for the benefit of people and planet.